The Patient Protection and Affordable Care Act (ACA) implemented a cost-sharing reduction (CSR) program to mitigate out-of-pocket expenses for low-income enrollees. With actual utilization for CSR members deviating significantly in some markets from pricing assumptions in 2014 and 2015, the difference between prospective payments from Centers for Medicare and Medicaid Services (CMS) and actual CSR payments may have a significant impact on financial statements for some carriers. This paper explores four different CSR estimates, focusing on their emergence and impact during the year for financial monitoring and reporting needs. The analysis and simulations show that even under a perfect scenario, where the cumulative year-end CMS prospective payment is equal to the cumulative year-end actual incurred CSR, there will be differences during the year, such that the actual incurred CSR in a given quarter is generally higher in the early quarters and lower in the latter quarters than the CMS prospective payment.

Background

CMS requires any qualified health plan (QHP) offering a silver plan in the individual market to offer alternative silver plans in addition to the standard silver plan. The alternative silver plans have a higher actuarial value (AV) than the standard silver plan, with AVs of 73%, 87%, and 94%. CMS subsidizes these alternatives by providing prospective CSR payments to issuers to account for estimated differences in cost sharing between the standard silver plan and the alternative silver plans. CMS uses the information in an insurer's Unified Rate Review Template (URRT) and its actual enrollment to determine the monthly prospective payment to the issuer.

There is a CSR settlement following the completion of the plan year where the prospective payment is trued up to what the actual difference in cost sharing is between the alternative silver plans and the standard silver plan. Prior to 2017, issuers can choose between two prescribed CSR methodologies to determine what the actual difference is. The two methodologies are the simplified methodology and the standard methodology. CMS prescribes two variations to the simplified methodology: one for plans that meet certain membership threshold requirements, and a further simplified approach for those that don't. It is expected that many plans will not be expected to meet these thresholds and will be required to implement a further simplified methodology if they elect the simplified option. Another Milliman paper1 written by Daniel Perlman and Jason Siegel gives an overview of CSR subsidies and the financial impact to plans based on the methodology selected. As of now, all issuers will be required to use the standard methodology after 2016.

After CMS extended the timeline for CSR settlement for the 2014 plan year and provided issuers an option to reelect the CSR methodology, many plans that previously had elected the simplified methodology (because they did not have the processes in place to fully re-adjudicate claims for CSR members using standard silver plan parameters or weren't able to find a vendor) changed their option to the standard methodology.

Analysis

The standard methodology requires claims to be adjudicated under both the standard silver plan parameters and the actual alternative silver plan parameters. Because this process can be costly to perform every month or every quarter, insurers often use alternative methods to estimate what the actual CSR amount is compared with the CMS prospective payment in order to better understand financials throughout the year. The rest of this paper describes and graphs the development of CSR amounts during the year using four different estimation methods:

- CMS prospective payment

- Actuarial value (AV) estimate

- Further simplified methodology

- "5 Bucket" method

Allowed claims were simulated for approximately 20,000 CSR members to target three different average allowed per member per month (PMPM) levels of $300, $500, and $800. Assuming a uniform distribution of monthly allowed claims during the year, we estimated CSR amounts by month for different plan design parameters determined using the 2016 AV calculator (please refer to the Assumptions and Methodology Section below for a description of the plan designs). The results shown below assume a 50%, 35%, and 15% distribution of the 94%, 87%, and 73% alternative silver plans.

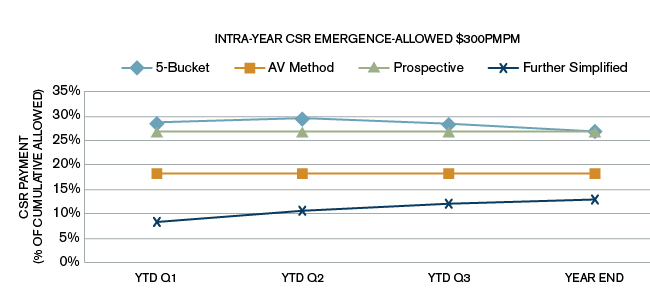

Figures 1, 2, and 3 show the emergence during the year of CSR estimates as a percentage of cumulative allowed claims using the four methods described below. To show the effect for low-cost, medium-cost, and high-cost populations, we simulated the CSR pattern at three different allowed cost levels: $300, $500, and $800 PMPM, for the methods shown above.

In addition to comparing the four estimates, our intention here is to show how the CSR slope for the prospective payment differs from the 5 Bucket method even when both methods give the same year-end CSR estimate.

The charts in Figures 1 to 3 demonstrate difference in slopes for the 5 Bucket and prospective methods during the year for the same year-end CSR estimate for these two methods for each of the allowed amounts, representing the three different population costs.

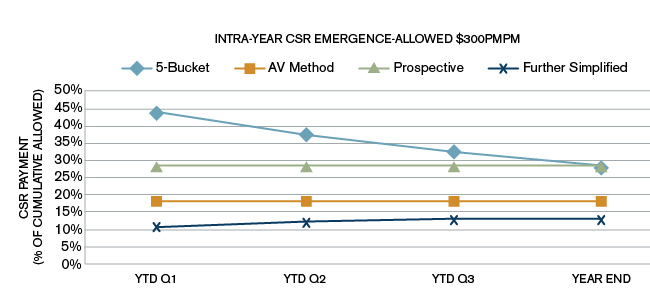

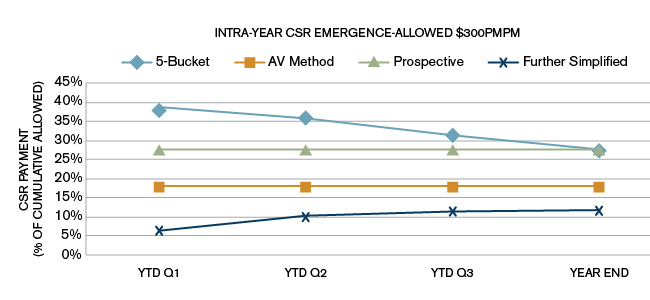

Figure 1: $300

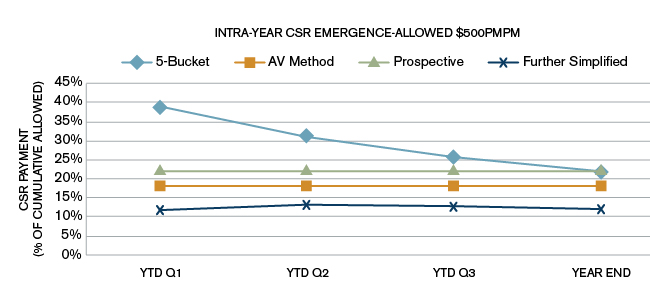

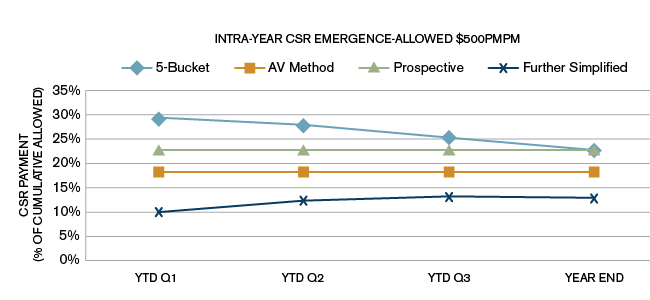

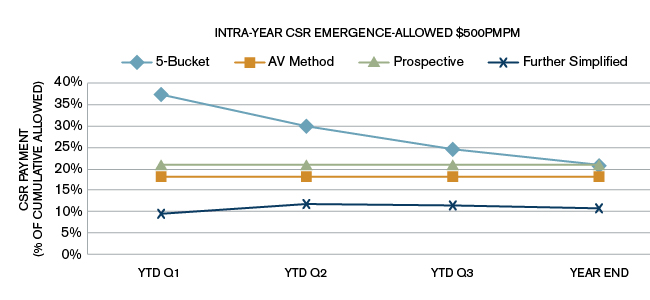

Figure 2: $500

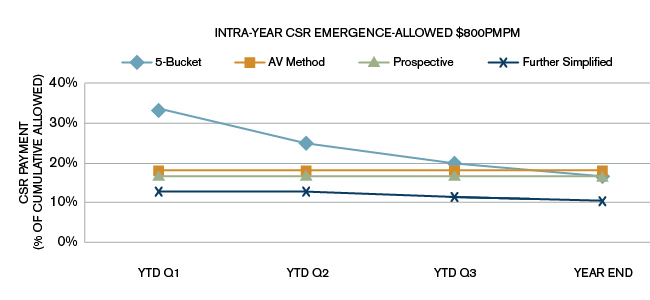

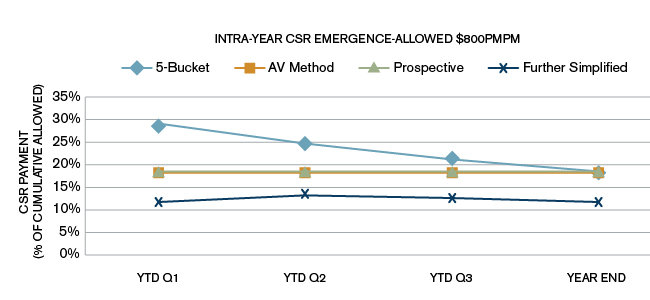

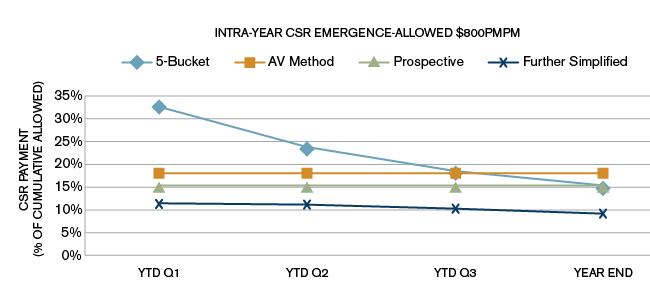

Figure 3: $800

As can be seen from the three charts in Figures 1 to 3, the CSR estimate for the 5 Bucket method as a percentage of average allowed (cumulative) goes down during the year. The AV method and the CMS prospective estimates are flat lines. The CMS prospective payment for these simulations in all charts was targeted to be equal to the same year-end estimate as the 5 Bucket method year-end estimate.

From these charts we see that even if pricing assumptions perfectly match experience to date, the cumulative percentage of allowed amounts under the 5 Bucket method is generally higher than what CMS is reimbursing on a monthly basis. The main drivers of the downward slope of the curve for the 5 Bucket method are the significant difference in member cost sharing between the standard plan and the alternative silver plan variation in Bucket 2 (as described below) and the fact that once an insured's claims exceed the standard plan out-of-pocket maximum (Bucket 5), the plan is no longer entitled to additional CSR reimbursements for that insured.

There will be exceptions when an insured's claims are still very low and most of the cost sharing is paid by the insured such that the CMS actual payment will exceed the actual CSR or the 5 Bucket method.

As the average allowed PMPM increases, the 5 Bucket method gives year end estimates lower than the AV method. In Figure 3, the 5 Bucket method provides a higher estimate for CSR at the end of the first three quarters but a lower estimate at the end of the year, once the full years' experience comes through (the light blue line goes below the orange line).

For plans whose actual average allowed PMPM for CSR members is significantly higher than pricing assumptions, the AV method (on the actual allowed experience) will generally overestimate the actual CSR payments the plans are likely to receive at the end of the year.

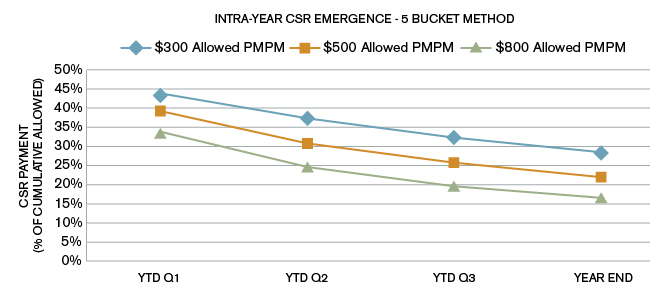

Figure 4 shows the CSR percentage of allowed using the 5 Bucket method for different allowed PMPMs.

Figure 4: 5 Bucket: Percent of Allowed

From this chart we see that the CSR amount as a percent of allowed generally decreases for higher allowed amounts.

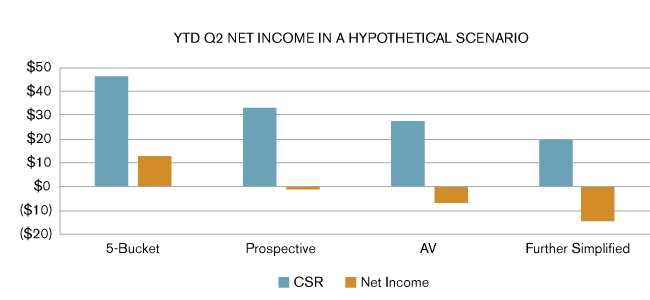

A simple hypothetical example shown in Figure 5 demonstrates the effects on year-to-date (YTD) Q2 net income for a carrier using different methods for CSR. The example assumes a portfolio of gold, silver, and bronze enrolees, with allowed amounts of $550, $500, and $420 respectively at 20%, 30%, and 50% distributions.

CSR percentages used to estimate CSR are from Figure 2 above. (This example assumed the following: premium $425 PMPM; expenses: $205 of premium; incurred claims: $415 PMPM; reinsurance recoveries: 10% of incurred claims.)

Figure 5: Net Income Effect

Methodologies and assumptions

The different methods used to estimate CSR are described below.

CMS prospective payment

The prospective payment PMPM from CMS is a flat PMPM that CMS pays plans based on the allowed amount projections and AVs used in the pricing assumptions. To the extent that allowed amounts used in pricing are significantly higher or lower than actual allowed, the actual payments and receipts will be higher or lower after year-end settlement.

For example, based on the pricing assumptions, CMS may pay a monthly prospective payment of $150 PMPM. If the actual CSR amount for the plan year is $175 PMPM; then a CSR reconciliation amount of $175 - $150 is paid by CMS to the QHP. The reconciliation can result in a payment or receipt, depending on whether the actual CSR amount is higher or lower than the prospective CSR payment.

AV method CSR estimate

The AV method uses Allowed Amount * (Difference of the AVs between CSR AV and Standard AV) as the CSR estimate.

This can also be viewed as:

Allowed * (1 - Standard AV) - Estimated CSR Member Cost Sharing

For example, assuming a $300 PMPM allowed for a 94% alternative silver plan, the CSR estimate under the AV method is calculated as $300 * (94% - 70%) = $72 PMPM.

Further simplified CSR estimate

Under this approach, the standard member cost sharing is estimated as the minimum of:

- Allowed * (1 - Standard AV)

- Standard out-of-pocket maximum (OOPM)

The CSR estimate then would be the difference of the above estimate and the actual member cost sharing under the alternative silver plan. Please refer to the Milliman paper by Siegel and Perlman referenced above for an example.

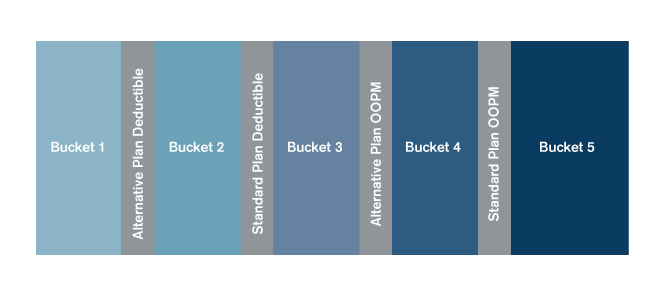

5 Bucket method

The 5 Bucket method estimate gives the true CSR cost for plans with a single coinsurance rate, deductible, and OOPM. While most plans will vary from this simplified plan design, we used the methodology to estimate the actual amount of CSR for this analysis. The following provides a description of the methodology:

Claims for each member are bucketed into five categories as outlined below:

Bucket 1: Allowed claims (A) below alternative plan deductibles (B)

Bucket 2: Allowed claims (A) that exceed alternative plan deductible (B) but are below standard deductible (C)

Bucket 3: Allowed claims (A) that exceed standard deductible (C) but are below alternative plan OOPM (D)

Bucket 4: Allowed claims that exceed alternative plan OOPM (D) but are below standard OOPM (E)

Bucket 5: Allowed claims that exceed standard OOPM (E)

Figure 6: 5 Bucket Method

Under each of these scenarios the CSR estimate can be estimated using the formulae below. For plan designs where all benefits are subject to deductible and have coinsurance, the 5 Bucket method gives estimates consistent with the actual CSR. For all other plan designs, the 5 Bucket method estimate will differ from standard and simplified methodology estimates. F represents the coinsurance rate of the alternative silver plan paid by the issuer. G represents the coinsurance rate of the standard silver plan paid by the issuer.

Bucket 1: CSR is always $0

Bucket 2: (A - B) * (F)

Bucket 3: (A - C) * (G - F) + (C - B) * (F)

Bucket 4: (A - D) * (1 - G) + (D - C) * (G - F) + (C - B) * (F)

Bucket 5: (E - D)

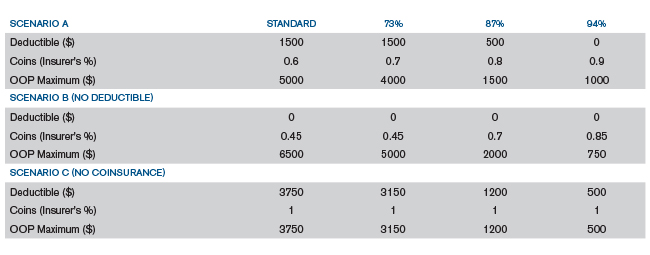

Data and plan design assumptions

Using claim probability distributions from the Milliman Health Cost Guidelines™, we simulated allowed claims for approximately 20,000 members. Three different types of plan design scenarios were considered for each of the CSR silver plans and the standard silver plan. In each of these plan designs, we assumed that allowed costs for preventive services are approximately 5% of total allowed costs and that these services are not subject to deductible and are covered by the plan at 100%. The CMS AV calculator was used to come up with these plan designs.

In preparing this report the plan designs shown in Figure 7 were reviewed.

Figure 7: Plan Designs Reviewed

For each of the plan design scenarios, we assumed 100% in-network utilization of services. Generally, higher out-of-network utilization will result in a greater difference between standard member cost sharing and alternative plan variation cost sharing. The charts used throughout this paper are based on Scenario A in Figure 7. The charts showing CSR amounts as a percent of allowed claims for scenarios B and C are included in the Appendix, where it can be seen that, although the year-end CSR as a percentage of allowed is similar across the three plan design scenarios, there is significant variation in the quarterly estimates.

Conclusions

Based on the charts and the hypothetical example above, it is clear that the methods used to estimate CSR in the absence of actual CSR estimates using the standard methodology (by adjudicating claims through two different plan parameters) can have a significant impact on the quarterly and annual financial statements of insurers.

Under a perfect pricing scenario, the prospective payment from CMS will be the same as incurred CSR at the end of the year. However, there will be differences during the year, such that the actual incurred CSR in a given quarter is generally higher in the early quarters and lower in the latter quarters than the CMS prospective payment.

Limitations

This report has been prepared to discuss certain aspects of the CSR program. The analyses and observations may not be appropriate for, and should not be used for, any other purpose.

The analysis described above was based on a limited set of plan designs. To the extent that an issuer offers standard and alternative plan designs materially different from those included in this analysis, results will differ from those cited above.

While the examples considered above focused on cost-sharing reduction amounts for alternative silver plans, CSR amounts are also paid by QHP plans with limited or no cost sharing.

Differences between our estimates and actual amounts depend on the extent to which future experience conforms to the assumptions made in this analysis. To the extent that there are differences, results will differ from those cited above.

Contact

If you have any questions or comments on this document, please contact your local Milliman consultant, or Aaron Wright or Shyam Kolli, who are actuaries with Milliman. Aaron and Shyam are members of the American Academy of Actuaries and meet the qualification standards of the American Academy of Actuaries to render the actuarial opinion contained herein.

The authors would like to acknowledge the peer review by Scott Katterman, who is a principal and consulting actuary in the Phoenix office of Milliman.

Appendix

Scenario B

Scenario C

1 Perlman, D. & Siegel, J. (November 2014). Cost-Sharing Reduction Subsidies: Financial Impact of the Simplified Methodology. Milliman Healthcare Reform Briefing Paper. Retrieved September 9, 2015, from /-/media/Milliman/importedfiles/uploadedFiles/insight/2014/csr-subsidies.ashx