January 31, 2016, marked the end of the third open enrollment period in the insurance marketplaces. The U.S. Department of Health and Human Services (HHS) reported that 12.7 million1 Americans purchased coverage in the insurance marketplaces during the 2016 open enrollment period, an increase of approximately 1 million individuals from the 2015 open enrollment period.2Does this signal that the insurance marketplace is functioning well or struggling? Evaluating the health of the insurance marketplace and the broader individual health insurance market, based solely on aggregate open enrollment selection changes in the marketplace, is problematic for several reasons. We examine three key issues and offer some suggestions for insurers and policymakers to consider when assessing the market:

1. Medicaid expansion and the Basic Health Program (BHP). In states that elect to expand Medicaid or implement a BHP, insurance marketplace enrollment may shrink as a result of marketplace enrollees shifting to these insurance programs. There is evidence of this occurring in several states between the 2015 and 2016 open enrollment periods.

First, in states that have not yet expanded Medicaid as of January 2016,3 the population with household income between 100% of the federal poverty level (FPL) and 138% FPL is eligible for premium assistance in the insurance marketplaces. Since the calendar year 2015 open enrollment period, four states (Alaska, Indiana, Montana, and Pennsylvania4) have elected to expand Medicaid under the Patient Protection and Affordable Care Act (ACA), which removes the population with income between 100% FPL and 138% FPL from the insurance marketplace.5 As shown by the table in Figure 1, this resulted in a decrease in plan selections for individuals with income between 100% FPL and 150% FPL in these four states. It is important to keep these changes in mind when reviewing the growth or decline in overall marketplace enrollments in these states.

In the 19 non-expansion states using the federal insurance marketplace, almost 3 million plan selections were made by individuals with household income between 100% FPL and 150% FPL, with nearly 1.5 million in Texas and Florida alone.

Figure 1: 100%-150% FPL Plan Selection Changes

| State | 2015 | 2016 | Decrease |

| Alaska | 5,800 | 4,300 | (1,500) |

| Indiana | 64,500 | 36,800 | (27,700) |

| Montana | 17,800 | 11,800 | (6,000) |

| Pennsylvania | 131,500 | 84,000 | (47,500) |

| Subtotal | 219,600 | 136,900 | (82,700) |

| Note: Data from HHS open enrollment reports. Selections limited to 100% to 138% FPL are not available. | |||

Given the likelihood that many of these 3 million individuals would otherwise be eligible for the Medicaid program, future state decision-making may significantly alter the growth of the marketplace in states electing to expand Medicaid. For example, Louisiana, which had nearly 46% of its open enrollment selections made by individuals with income between 100% FPL and 150% FPL, has announced it will implement Medicaid expansion on July 1, 2016.6

Similarly, states implementing the Basic Health Program7 (currently New York and Minnesota) have moved the population with income between 138% FPL and 200% FPL outside the insurance marketplace. Between these two states, 400,000 individuals have signed up for the BHP in 2016.8 The January 1, 2016, implementation of the BHP in New York resulted in total marketplace selections decreasing from over 400,000 in 2015 to under 275,000 in 2016.9

Insurers assessing market growth opportunities in the marketplace should take these potential changes in public program eligibility into account when evaluating the long-term growth potential of the marketplace.

2. Premium increases and market bifurcation. The ACA permits individuals with annual household incomes between 100% FPL (approximately $12,000 for a single household) and 400% FPL (approximately $48,000 for a single household), who do not qualify for other forms of minimum essential coverage, to receive premium assistance through the insurance marketplace. This is conditioned on the premium of the subsidy benchmark plan costing more than a certain percentage of an individual’s household income. To the extent the subsidy benchmark plan costs less than the maximum amount the individual must pay under the ACA, the value of premium assistance is $0. This results in the value of premium assistance reaching $0 well below 400% FPL for younger individuals in many states.

For example, in 2016, the Kaiser Premium Subsidy Calculator10 indicates that the average national subsidy benchmark premium for a 25-year-old is $235 per month ($2,818 per year). For a single individual with income of approximately $32,400 (275% FPL), the ACA requires the individual to pay up to 8.92% of income for the benchmark plan ($2,886 per year). Because the premium cost is less than the maximum amount required under the ACA at this income level, no premium assistance is available for individuals age 25 who are at or above this income level.

To the extent a state’s insurance market experiences significant premium increases from one year to the next, this can significantly alter the population that qualifies for premium assistance by increasing the income level where premium assistance reaches $0. In the table in Figure 2, we have summarized the income level where premium assistance ended in 2015 and 2016 for single individuals ages 25 and 40 for federal marketplace states experiencing an increase in the average subsidy benchmark premium of more than 20% from 2015 to 2016.

Figure 2: Income Level Where Premium Assistance Ends

| State |

Subsidy Benchmark Change |

25-Year-Old | 40-Year-Old | ||||||

| 2015 | 2016 | 2015 | 2016 | ||||||

| Oklahoma | 36% | 238% | 275% | 269% | 324% | ||||

| Montana | 35% | 245% | 283% | 277% | 340% | ||||

| Alaska | 32% | 400% | 400% | 400% | 400% | ||||

| South Dakota | 25% | 257% | 286% | 292% | 347% | ||||

| Tennessee | 23% | 242% | 266% | 274% | 304% | ||||

| Oregon | 23% | 237% | 260% | 268% | 295% | ||||

| North Carolina | 23% | 283% | 322% | 340% | 400% | ||||

| Arizona | 21% | 223% | 242% | 250% | 273% | ||||

As Figure 2 indicates, in many states experiencing large premium increases, the population qualifying for premium assistance was expanded to higher income levels. Alaska did not experience this phenomenon because premiums in 2015 were high enough to generate subsidy value up to 400% FPL even for a 25-year-old.

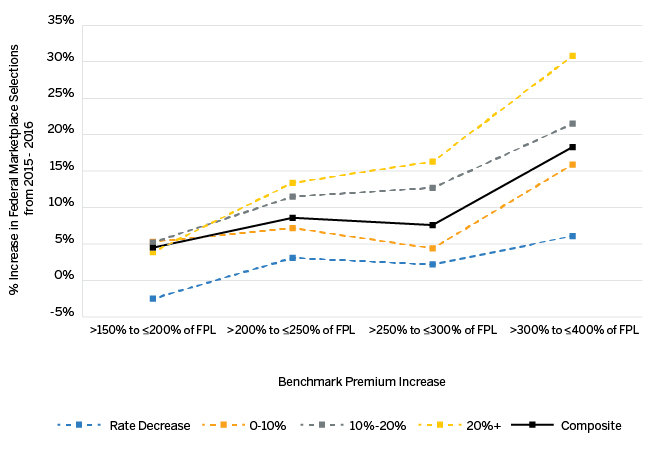

As illustrated in the chart in Figure 3, federal marketplace states with significant benchmark premium increases from 2015 to 2016 had greater increases in marketplace plan selections at higher subsidy-qualifying income levels relative to states with rate decreases or moderate premium increases. Less variance between states was observed in marketplace selection changes at lower income levels, where much of the population was likely eligible for premium assistance in 2015 and 2016. It should also be noted that the population with income between 300% FPL and 400% FPL experienced larger percentage increases in marketplace plan selections from 2015 to 2016 relative to lower-income cohorts regardless of state premium changes, potentially driven by higher individual mandate penalties in 2016.

Figure 3: CY 2015-CY 2016 Percentage Change in Federal Marketplace Plan Selections Segmented by Income Level and Subsidy Benchmark Premium Increase

Although other factors such as the individual mandate may influence future marketplace enrollment growth, some enrollment increases may occur solely as a result of the value of premium assistance rising in the future because of annual premium trend. Premium increases over time may result in a much greater proportion of younger adults becoming eligible for premium assistance in the marketplace. Whether growth in the individual marketplace is a result of greater overall health insurance participation, or simply shifting insurance coverage from off-marketplace to marketplace products, will influence future changes in the health of the individual market’s overall risk pool. For example, if the entire growth in marketplace enrollment from one year to the next was simply a result of individuals shifting from off-exchange to exchange products, the overall morbidity of the individual market risk pool would not improve. Conversely, if the growth was entirely newly insured individuals, it may be an indication of the risk pool becoming healthier. For insurers developing premiums for 2017 and future years, this issue should be strongly considered in the development of morbidity factors used in pricing individual market products.

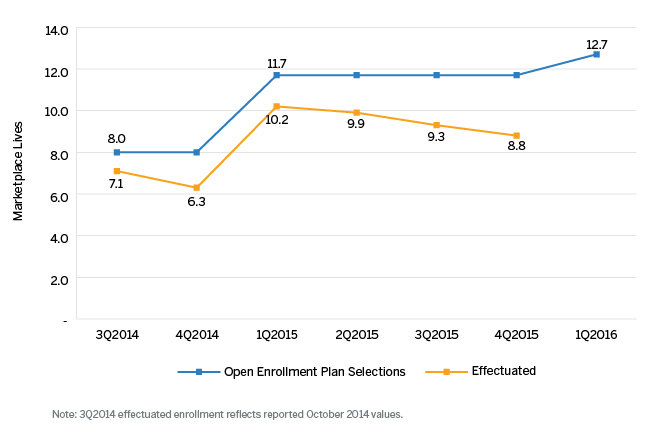

3. Plan selections versus effectuated enrollment. During the first two full years of the insurance marketplace’s operation, HHS has announced significant differences between the number of plan selections during each year’s open enrollment period and the actual number of individuals paying and maintaining coverage (“effectuated enrollment”). The chart in Figure 4 illustrates open enrollment plan selections from 2014 through 2016, as well as quarterly effectuated enrollment. While 2015 open enrollment plan selections increased by 3.7 million relative to 2014, year-end effectuated enrollment only increased by 2.5 million (from 6.3 million to 8.8 million).11 HHS has estimated that 10 million individuals will have effectuated enrollment at the end of 2016.12

Figure 4: Open Enrollment Plan Selections vs. Effectuated Enrollment: Insurance Marketplace National Values

For insurers, the material decreases in marketplace enrollment over the course of the calendar year make financial projections particularly challenging. Insurers should study lapse rate patterns from prior years (such as by income and age cohorts) to better estimate premium and claim expenses for the current calendar year.

Conclusion

While much attention gets paid to open enrollment aggregate selection counts, insurers and policy makers should study the underlying changes in plan selections by age and income to better understand the health of the insurance marketplaces. As the marketplaces enter their 10th quarter of operation, state healthcare policy decisions and premium rate changes may have a significant influence on future enrollment changes within the marketplace for certain demographic cohorts.

1Department of Health & Human Services (March 11, 2016). Health Insurance Marketplaces 2016 Open Enrollment Period: Final Enrollment Report. Retrieved April 13, 2016, from: https://aspe.hhs.gov/sites/default/files/pdf/187866/Finalenrollment2016.pdf.

2Department of Health & Human Services (March 10, 2015). Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report. Retrieved April 13, 2016, from: https://aspe.hhs.gov/sites/default/files/pdf/83656/ib_2015mar_enrollment.pdf.

3See https://www.advisory.com/daily-briefing/resources/primers/medicaidmap for a listing of states that have expanded Medicaid under the ACA.

4In the case of Pennsylvania, it appears a change from an alternative to standard Medicaid expansion program resulted in individuals moving from the marketplace to Medicaid.

5See http://kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/ for a list of states expanding Medicaid under the ACA.

6Litten, K. (January 12, 2016). John Bel Edwards signs Medicaid expansion to make 300,000 eligible for federal program. New Orleans Times-Picayune. Retrieved April 5, 2016, from http://www.nola.com/politics/index.ssf/2016/01/john_bel_edwards_medicaid.html.

7See /-/media/Milliman/importedfiles/uploadedFiles/insight/healthreform/healthcare-reform-basic-health.ashx for an overview of the Basic Health Program.

8Jacob, J.A. (March 22/29, 2016). Open enrollment increased by about 1 million people over last year. Journal of the American Medical Association. Retrieved April 5, 2016, from http://jama.jamanetwork.com/article.aspx?articleid=2504796.

9HHS open enrollment reports for 2015 and 2016.

10The subsidy calculator is available at: http://kff.org/interactive/subsidy-calculator/.

11Centers for Medicare and Medicaid Services (March 11, 2016). December 31, 2015 Effectuated Enrollment Snapshot. Fact Sheet. Retrieved April 5, 2016, from https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-03-11.html.

12HHS.gov (October 15, 2016). 10 million people expected to have Marketplace coverage at end of 2016. Press release. Retrieved April 5, 2016, from http://www.hhs.gov/about/news/2015/10/15/10-million-people-expected-have-marketplace-coverage-end-2016.html.