Loss development factors are a major component in many commonly used actuarial techniques. Workers’ compensation is a long tail line of insurance with losses developing upward for over 30 years. For most companies, the data in their workers’ compensation loss development triangles ends before the ultimate cost of the claims in an accident year is known. In this case, how should a tail factor, developing losses from the last evaluation point to ultimate, be selected?

The selection of the loss development tail factor is extremely important because it affects estimates for all accident years; a minor adjustment to the tail factor can have a significant impact on the unpaid claim liability. Milliman has created and utilized a workers’ compensation database that includes $55 billion of incurred losses to assist in selecting appropriate tail factors. With this significant amount of data, we are able to select tail factors that consider three key variables: retention, location, and industry. We have used our database to build triangles at several different retentions for countrywide losses, state-specific losses, and by industry. The impact of a selected tail factor is significant as the following example highlights.

Let’s suppose a new company was formed in 2010 and now has six years of workers’ compensation data. The company has a $500,000 per occurrence large deductible. The company has significant loss experience and the data in its loss development triangle is considered actuarially credible. However, the 2010 year is only six years old (72 months) and the company has no experience before that point. What tail factor should be selected?

Figure 1: Choosing a tail factor

| Incurred losses (000’s) | |||||||

| Accident Year | Months of maturity | ||||||

| 12 | 24 | 36 | 48 | 60 | 72 | Ultimate | |

| 2010 | 2,829 | 3,961 | 4,418 | 4,668 | 4,816 | 4,906 | ??? |

| 2011 | 2,830 | 3,905 | 4,358 | 4,570 | 4,714 | ??? | |

| 2012 | 2,996 | 4,130 | 4,609 | 4,833 | ??? | ||

| 2013 | 3,134 | 4,355 | 4,826 | ??? | |||

| 2014 | 3,446 | 4,792 | ??? | ||||

| 2015 | 3,690 | ??? | |||||

| Incurred loss development factors | ||||||

| Accident Year | Age-to-age | |||||

| 12-24 | 24-36 | 36-48 | 48-60 | 60-72 | 72-Ult | |

| 2010 | 1.40 | 1.12 | 1.06 | 1.03 | 1.02 | |

| 2011 | 1.38 | 1.12 | 1.05 | 1.03 | ||

| 2012 | 1.38 | 1.12 | 1.05 | |||

| 2013 | 1.39 | 1.11 | ||||

| 2014 | 1.39 | |||||

| Selected | 1.39 | 1.11 | 1.05 | 1.03 | 1.02 | |

| Cumulative | 12-Ult | 24-Ult | 36-Ult | 48-Ult | 60-Ult | 72-Ult |

| Countrywide - unlimited | 1.91 | 1.37 | 1.24 | 1.18 | 1.14 | 1.12 |

| Countrywide – lim. to $500k | 1.79 | 1.29 | 1.16 | 1.10 | 1.07 | 1.05 |

| California - unlimited | 2.13 | 1.53 | 1.38 | 1.31 | 1.28 | 1.25 |

| Illinois - unlimited | 1.77 | 1.27 | 1.15 | 1.09 | 1.06 | 1.04 |

Based on all the data in our database, the countrywide unlimited tail factor from 72 months to ultimate is 1.12. The 72 to ultimate factor is then multiplied by the 60 to 72 month factor (1.02) to get the 60 to ultimate factor of 1.14. This process is continued to estimate the remaining cumulative development factors at 12, 24, 36, and 48 months. An estimate of ultimate losses can be made by applying the appropriate cumulative development factor to each accident year of incurred losses. The resulting incurred but not reported (IBNR) figures are shown in Figure 2.

Figure 2: Tail factor of 1.12

| Accident year | Months of maturity | Incurred losses (000’s) | Incurred LDF | Ultimate losses (000’s) | Indicated IBNR (000’s) |

| 2010 | 72 | 4,906 | 1.12 | 5,495 | 589 |

| 2011 | 60 | 4,714 | 1.14 | 5,385 | 671 |

| 2012 | 48 | 4,833 | 1.18 | 5,687 | 854 |

| 2013 | 36 | 4,826 | 1.24 | 5,963 | 1,137 |

| 2014 | 24 | 4,792 | 1.37 | 6,572 | 1,780 |

| 2015 | 12 | 3,690 | 1.91 | 7,034 | 3,344 |

| Total | 27,761 | 36,135 | 8,374 |

However, the unique characteristics of each company are not captured when utilizing all of the data in our database. Three critical adjustments can be made to the tail factor to more accurately estimate the future development.

Retention

Workers’ compensation losses are paid sequentially. This is somewhat unique to workers’ compensation. Other lines of coverage such as general liability, as the result of a verdict or settlement, often pay the last dollar of losses at the same time as the first. In a large workers’ compensation loss, the first $500,000 of losses will be paid significantly before the next $500,000 of losses. In general liability, the first $500,000 of losses will often be paid at exactly the same time as the next $500,000 of losses. The verdict or settlement will be the entirety of the loss.

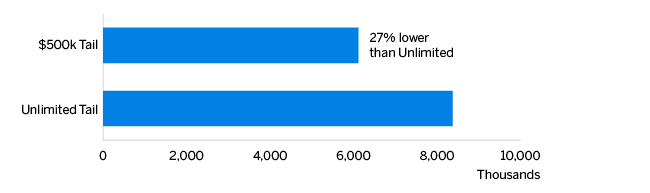

Most actuaries realize that the loss development factors need to be adjusted to account for the retention of a self-insured or large deductible, but the data needed to make these adjustments is not readily available. Our database is large enough to accurately capture the differences in loss development factors depending on the retention. Going back to our example for a countrywide risk, the difference between using an unlimited tail factor and a tail factor adjusted for a $500,000 retention significantly changes the estimated IBNR as shown in Figure 3.

Figure 3: Indicated IBNR

Location

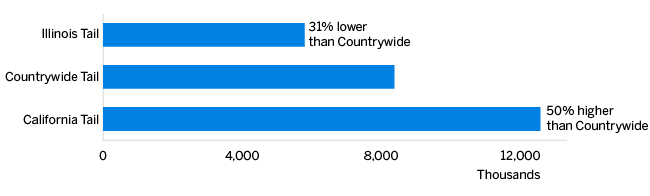

Workers’ compensation laws are state-specific. The loss development patterns for each state are unique and the development patterns between states are very different. The 72-month loss development tail for California, from our database, is 1.25 whereas the 72-month factor for Illinois is 1.04. Applying a countrywide pattern to a California risk would significantly understate the IBNR. Similarly, applying a countrywide pattern to an Illinois risk would significantly overstate the IBNR. The charts in Figure 4 show the potential magnitude of the error.

Figure 4: Indicated IBNR

It is critically important to any actuarial analysis that the loss development factors accurately reflect the geographical composition of the company’s workers’ compensation exposure.

Industry

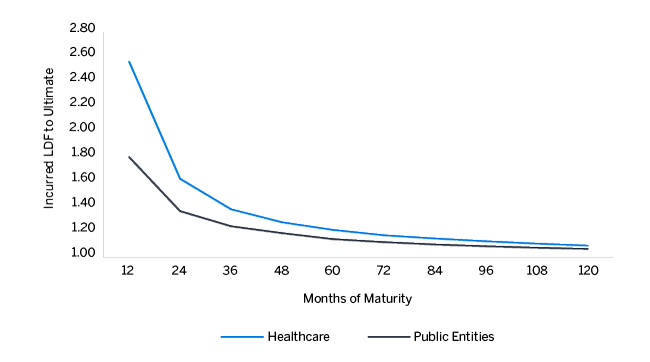

Most actuaries make adjustments for location, but very few make adjustments for the company’s industry. We have been researching loss development by industry for the last six years and have found that there are significant differences in the loss development factors that are due to industry. In the chart in Figure 5, we compare the incurred loss development factors for the healthcare industry and public entities. The difference in the development factors begins at 12 months of maturity and persists throughout the entirety of the development.

Figure 5: Incurred loss development: Healthcare versus public entities

Conclusion

It is critical to the accuracy of an actuarial study that the loss development tail be adjusted to reflect the uniqueness of each company. Most actuaries have been making adjustments for location because of the availability of industry loss development information by state. Our research has concluded that actuaries should also be considering the industry in their analyses. Most importantly, an adjustment for the company’s retention is absolutely necessary to ensure that the IBNR is not overstated. The database we have created allows us to factor in location, industry, and retention, and gives us the ability to select tail factors that incorporate exposure characteristics that prevent understated or overstated IBNR estimates.