One of the biggest developments in pension accounting in recent years has been the trend toward using the spot rate approach for calculating pension expense. Several alternative pension expense approaches exist, but the spot rate approach is the resounding favorite among plan sponsors who made the switch—we’ll walk through why it is growing in popularity.

The spot rate approach uses individual “spot” interest rates from a corporate bond yield curve rather than a single average discount rate derived from such a yield curve. The distinction may sound obscure, but using the spot rate approach can have a meaningful effect on an employer’s accounting results. For an upward-sloping yield curve, the spot rate approach generally lowers the interest cost and service cost1—and therefore the pension expense—compared with using a single average discount rate. In addition, this approach is more refined and applies the yield curve consistently across all of the calculations required under U.S. GAAP financial accounting.

Milliman’s most recent annual corporate pension funding study2 noted that 37 of the 100 largest corporate defined benefit (DB) pension plans indicated their intention to adopt the spot rate approach in their most recent Form 10-K reports. The study’s authors estimate this change will reduce these companies’ interest cost (IC) about 20%.

Obviously, a 20% reduction in IC can be significant, which effectively sends a message to sponsors of DB plans of all types and sizes: Should you consider this strategy for your pension plans?

A short timeline for approval and acceptance

To help start the discussion, let’s review the recent history of the spot rate approach. AT&T Inc. was the first mover, disclosing the change to the new approach in its Form 10-K in late 2014. In April 2015, the U.S. Securities and Exchange Commission (SEC) began investigating the change from a compliance perspective. By September, SEC officials had concluded that spot rate calculations passed muster, and communicated to representatives of the Big Four accounting firms that the SEC would not object to use of the spot rate approach (given certain facts and circumstances). Before the end of 2015, the American Academy of Actuaries had also weighed in.

It seems remarkable that 37 of the 100 largest corporate pension programs could have moved so quickly to adopt the new approach. But it makes sense when you consider that, according to the Milliman study, IC savings3 could have exceeded $14 billion in 2016 if all 100 of the largest DB plans had switched to the spot rate approach.

Without going too deeply into technical details, let’s look at how the spot rate approach differs from the traditional single-weighted-average approach. This will also demonstrate how the IC savings are generated.

Simplified example

For purposes of illustration, we’re creating a simple pension plan with three people. At retirement, each will receive a $10,000 lump-sum payment. Presently Joe is 60 years old, Joy is 55, and Ben is 50—and we’re assuming each will retire at age 65.

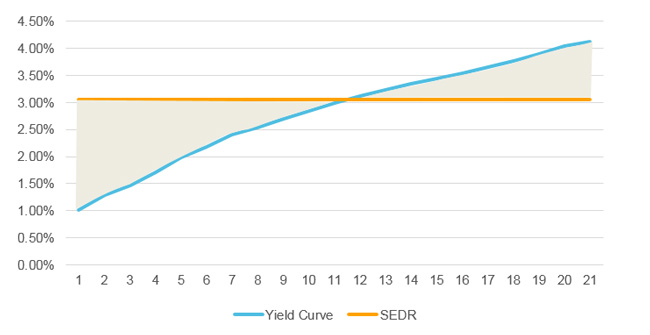

When calculating the liability for financial reporting purposes, the present value of those cash flows must be taken. We’re using the Above Median Citi Pension Discount Curve from April 30, 2016, graphed below (Figure 2). The standard approach solves for a single equivalent discount rate (SEDR) based on the yield curve and the plan’s cash flows. The SEDR—rather than the yield curve—is then used to calculate the projected benefit obligation (PBO), IC, and service cost (SC). In this example, the SEDR is 3.06%.

Figure 1

| FYE 2015 - PBO calculation | ||||

| Time to retirement | PBO payout | YC | PV at YC | PV at SEDR |

| 0 | 0 | 1.01% | 0 | 0 |

| 1 | 0 | 1.29% | 0 | 0 |

| 2 | 0 | 1.47% | 0 | 0 |

| 3 | 0 | 1.72% | 0 | 0 |

| 4 | 0 | 1.98% | 0 | 0 |

| Joe: 5 years | 10,000 | 2.19% | 8,975 | 8,600 |

| 6 | 0 | 2.41% | 0 | 0 |

| 7 | 0 | 2.54% | 0 | 0 |

| 8 | 0 | 2.69% | 0 | 0 |

| 9 | 0 | 2.85% | 0 | 0 |

| Joy: 10 years | 10,000 | 2.99% | 7,448 | 7,395 |

| 11 | 0 | 3.12% | 0 | 0 |

| 12 | 0 | 3.24% | 0 | 0 |

| 13 | 0 | 3.35% | 0 | 0 |

| 14 | 0 | 3.45% | 0 | 0 |

| Ben: 15 years | 10,000 | 3.54% | 5,932 | 6,360 |

| PBO | 22,355 | 22,355 | ||

PBO is the same in both approaches

As you can see in the table in Figure 1, the spot rate approach applies the interest rates for each year when payouts are expected: 2.19% in year 5, 2.99% in year 10, and 3.54% in year 15. The standard approach uses the SEDR of 3.06% to discount each cash flow.

Using the respective spot rates, from either the yield curve or the SEDR, we obtain the discounted cash flows for each of the three participants. The sum of discounted cash flows for the employee population is the PBO.

As Figure 1 shows, the PBO is identical for the plan as a whole using both approaches.

Figure 2: Yield curve and SEDR

IC is lower using the spot rate approach

The IC using the spot rate approach is lower compared with the standard approach. Let’s take a closer look.

Under the spot rate approach, the IC is the sum of the cash flows that make up the PBO for each participant multiplied by the appropriate spot rate. As Figure 3 shows, with a typical upward-sloping yield curve, the IC is smaller for Joe, who retires in five years; evens out for Joy, at 10 years; and becomes larger after that for younger employees like Ben, who will retire in 15 years.

Figure 3

| Interest Cost Standard Approach | |||

| Liability | SEDR | Interest Cost | |

| Joe | $8,600.00 | 3.06% | $263.16 |

| Joy | $7,395.00 | 3.06% | $226.29 |

| Ben | $6,360.00 | 3.06% | $194.62 |

| Total | $684.07 | ||

| Interest Cost Spot Rate Approach | |||

| Liability | Spot rate | Interest Cost | |

| Joe | $8,975.00 | 2.19% | $196.55 |

| Joy | $7,448.00 | 2.99% | $222.70 |

| Ben | $5,932.00 | 3.54% | $209.99 |

| Total | $629.24 | ||

The total IC is less using the spot rate approach because lower interest rates are applied to the larger liabilities owed to employees closest to retirement. By the time the spot rates are higher than the SEDR, the principal amounts have become relatively small. You can see this in Figure 2 above, where the shaded area below the horizontal SEDR line represents the discounted liabilities that are due in 10 years or less, compared with the shaded area above the line, representing the post-10-year liabilities.

What if the yield curve flattens or inverts?

In this hypothetical example, the spot rate approach reduces pension expense by about 8%. However, recall that in the pension funding study, the IC reduction of programs using the spot rate approach was estimated to be 20%. The shape of the yield curve and the maturity4 of the plan are the key drivers of the magnitude of the IC reduction. Briefly, the steeper the curve or the more mature the plan, the larger the reduction and vice versa. But what happens if the yield curve were flat or inverted (downward sloping)?

If the yield curve were perfectly flat, then both approaches would give the same result. And an inverted yield curve would produce a larger IC than the standard approach. However, these conditions have been historically infrequent. Thus, we believe it’s reasonable to expect the spot rate approach will produce lower IC with occasional, short-lived exceptions.

Service cost is also lower

Another component of pension expense affected by the spot rate approach is the SC. SC is the discounted cost (present value) of the benefits the employees will earn in the next year. Like the calculation of PBO, a higher discount rate results in a smaller SC.

Returning to Figure 2 above, we note that the bulk of the SC liabilities accumulate relatively far out on the yield curve. Thus, the spot rate approach would be applying discount rates that are, on average, higher than the SEDR. As a result, we get a lower SC when we switch from using the SEDR to using spot rates along the yield curve. While the SC is expected to come down, the decrease is generally not going to be as large as the IC decrease. SC might be expected to come down 5% to 7% per an American Academy of Actuaries Issue Brief.

Net gains and losses

We encounter another simple mathematical truth when we calculate the PBO year over year: When the yield curve is upward sloping, the spot rate approach will always result in either smaller gains or larger losses relative to the standard approach.

That’s because, in the year-end gain/loss calculation, the expected liability is projected based on the lower IC, so expected PBO will be lower. No matter what the actual PBO ends up being, because the expected PBO was lower, the resulting liability gain will be smaller (or loss larger). This can lead to larger losses being amortized in later years. Over time, this will offset the reductions in pension expense that are produced by the spot rate approach.

This means the pension expense reductions from the spot rate approach boil down to a question of timing. Eventually, pension expense will increase as smaller gains and larger losses are amortized. Thus, in considering this strategy, it’s always a question of when do you want to recognize pension expense? Generally, because of the time value of money (which gain/loss amortization ignores), companies want to recognize pension expense as slowly as possible.

Spot rate approach deemed incompatible with bond-matching strategies

Unfortunately, plan sponsors who set their SEDRs using a bond-matching strategy and were considering adopting the spot rate approach, received some bad news. On August 2, 2016, SEC staff met with the representatives of the Big Four accounting firms. The SEC staff revealed that the SEC would object to a switch to the spot rate approach made by plan sponsors who use a bond-matching strategy.

The specific strategy the SEC expressed concern with was one where a yield curve was constructed from a plan’s hypothetical bond portfolio. According to information reported by those firms, the SEC argued that the spot rates from such a yield curve were not directly observable, and therefore the proposed strategy would not meet the requirement under ASC 715-30-35-8 to use the same interest rates to measure the benefit obligation and interest cost.5

While there may be more to the story, the rationale reported raises some questions. With only the information reported, we seem to run into an unintended contradiction. The corporate bond yield curves used in pension financial accounting calculations are all engineered through “generally accepted yield curve construction techniques,” and, as such, none of the associated spot rates are necessarily observable. This context implies the SEC’s argument could be made against the spot rate approach for all plans using a yield curve to set their SEDR—a conclusion it seems clear the SEC was not trying to reach given prior staff comments.

It’s entirely plausible that the nuances of the SEC’s rationale are missing or were summarized in a way that certain meaning was lost. As such, in time, we may receive additional clarification or new information, but for now plan sponsors using bond matching likely will not receive auditor approval to switch to the spot rate approach.

Plan sponsors with multiple plans that currently use a single SEDR

Figure 1 above shows that the PBO for a single plan is the same whether the spot rate approach or a SEDR is used. What about plan sponsors with multiple plans that use the same SEDR for all plans? In this case, the PBO by plan will vary, but the total PBO for the company, that is, adding up the PBO for all the plans, will be the same. The PBO by plan will vary because we’d be applying the yield curve separately to each plan, producing unique discount rates by plan.

To help see this, consider our three-participant plan. What if those were three separate plans, one per participant. It’s clear that the SEDR would still be 3.06% when the three plans are combined, but individually, under the spot rate approach, each plan would have a unique SEDR equal to the spot rate associated with the time until each participant retired.

On average, the spot rate approach gets us back to the same total PBO on the company’s books, whether we have three separate plans or one combined plan.

Change of approach is a long-term, permanent decision

The accounting argument for switching to the spot rate approach generally is that plan sponsors expect it to provide a more precise estimate of pension expense by applying the yield curve directly in all calculations rather than the SEDR. It meets the standard of fiduciary prudence based on the SEC’s evaluation and commitment not to object to its use—bolstered by its rapid acceptance by nearly 40% of the largest pension funds and their auditors.

In addition to the accounting rationale for the change in approach, the reduction in pension expense, which we’ve presented above, is a clear benefit for an organization’s income statement.

That said, it’s still important to include on any due diligence checklist a detailed discussion with your plan’s auditors. Given the SEC’s statement that it won’t object to the use of the spot rate approach and the many recent precedents, you’re not likely to encounter objections to the basic principle.

However, it’s a good idea to confirm that converting to the spot rate is a change in accounting estimate rather than in method. A change in estimate does not require restating results for prior years as a change in method would.

It’s also important to recognize that the switch to the spot rate approach is likely a one-way street and should be viewed as a permanent feature of accounting for pension plans. The fundamental case for the spot rate approach rests on its improved precision: By using the yield curve and all the information it contains, and applying it consistently in all calculations (PBO, IC, and SC), and for all plans, the results will be more precise than they’d be using a SEDR. Once you’ve presented this argument it would be difficult to reverse course and switch back to the SEDR-based approach.

Should you consider this strategy for your pension plans?6

Because of the spot rate approach’s improved precision, ability to reduce pension expense, and the combination of a lack of SEC objection (at least for plan sponsors using a yield curve approach)7 and general auditor approval, we envision that it could continue to increase in popularity. As such, if you haven’t already done so, you may want to start conversations with your auditors and actuaries to help determine exactly how the new approach would impact your pension expense—and if the shoe fits, outline a transition plan for implementation.

1Because many plans are frozen and do not have a service cost, we focus most of our attention on the interest cost calculations.

2Perry, A.H. et al. (April 7, 2016). Milliman 2016 Corporate Pension Funding Study. Retrieved July 31, 2016, from http://us.milliman.com/insight/2016/2016-Corporate-Pension-Funding-Study/.

3Eventually, as discussed in the net gains and losses section below, these savings will be recognized through gain/loss amortization, so the IC savings is really a deferral of pension expense.

4For simplicity, we’ll use plan maturity as a proxy for the duration of the plan’s cash flows.

5Deloitte, (August 24, 2016). Financial Reporting Alert 16-2. Retrieved August 24, 2016, from http://www.iasplus.com/en-us/publications/us/financial-reporting-alerts/2016/16-2.

6Remember the opening question? “Consider” is the key word. The spot rate approach isn’t necessarily appropriate for all plan sponsors. Each plan sponsor should consider their own circumstances and decide if the spot rate approach is right for them.

7Plan sponsors using a bond-matching approach are not likely to receive approval from their auditor given the most recent SEC staff comments.