On Friday, July 29, the Centers for Medicare and Medicaid Services (CMS) announced another large decrease in the monthly direct subsidy revenue to Employer Group Waiver Plans (EGWPs). Additionally, the Medicare Payment Advisory Commission (MedPAC) recently proposed changes to the Medicare program that could affect EGWP plan costs. Financial dynamics and an evolving regulatory environment continue to influence the value of EGWPs and Retiree Drug Subsidy (RDS) plans in the group retiree pharmacy benefits market. Plan sponsors should periodically evaluate the effect of emerging trends on RDS and EGWP programs to optimize the plan value as the market continues to evolve.

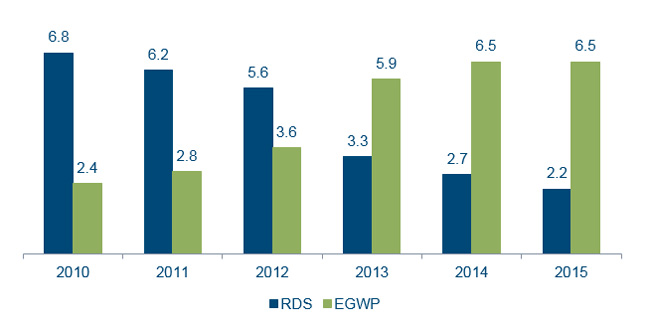

The number of beneficiaries covered by EGWPs has outnumbered those covered by RDS plans since 2013. When Medicare Part D was first introduced in 2006, the typical plan sponsor savings under EGWPs and RDS plans was comparable, but RDS plans were often a more favorable option for taxable plan sponsors due to the tax-favored treatment of the RDS.

Until the passage of the Patient Protection and Affordable Care Act (ACA), plan sponsors could deduct health benefit costs reimbursed by the RDS from their taxable incomes. Starting in 2013, plan sponsors were no longer permitted to deduct health benefit costs reimbursed by the RDS, eliminating the once tax-free status of the RDS. The ACA also introduced the Part D Coverage Gap Discount Program (CGDP) in 2011, under which pharmaceutical manufacturers pay 50% of the cost of eligible brand drugs in the coverage gap phase of the Part D benefit for non-low-income beneficiaries. EGWPs receive these CGDP payments, while RDS plans do not. The elimination of the tax-favored treatment of RDS plans combined with the increase in EGWP savings through the CGDP made EGWPs a more attractive option for many plan sponsors.

These regulatory changes prompted a relatively large shift from RDS plans to EGWPs in 2013 as plan sponsors reevaluated the financial opportunities associated with their group retiree pharmacy benefits. Figure 1 below illustrates this enrollment shift.1

Figure 1: RDS and EGWP Enrollment (millions)

Since 2013, regulatory and market dynamics continue to alter the group retiree pharmacy benefits landscape. These changes include the following, among others:

- reductions to the Part D direct subsidy,

- increasing pharmacy costs from specialty drugs,

- regulatory clarifications regarding the EGWP claim adjudication methodology, and

- recent proposals with the potential to affect EGWP revenue items.

While EGWPs may continue to be more favorable than the RDS for a typical retiree plan in the current environment, this may change for plans as a result of current proposals and future trends. Figure 2 below summarizes key recent and proposed market and regulatory dynamics affecting the relative value of EGWPs and RDS plans since the general shift from RDS plans to EGWPs in 2013.

Figure 2: Trends and Changes Affecting the Group Retiree Pharmacy Benefits Market Since 2013

| Change | Financial Impact on EGWPs | Financial Impact on RDS Plans2 |

| Reductions to the Part D direct subsidy. | Reduces the EGWP risk-adjusted direct subsidy revenue. | No effect. Not applicable to RDS program. |

| Increasing pharmacy costs from specialty drugs. | Mitigated due to 80% federal reinsurance protection for catastrophic claim costs. | Generally reduces the value of RDS plans relative to EGWPs from a plan sponsor’s perspective due to the maximum cost limit on the RDS. |

| Changes to the EGWP claim adjudication methodology. | Generally increases plan liability, while reducing federal reinsurance, compared with prior methodology used by many pharmacy benefit managers (PBMs). | No effect. Not applicable to RDS program. |

| Proposed change to Part D federal reinsurance program. | Would decrease federal reinsurance and increase direct subsidies. | No effect. Not applicable to RDS program. |

| Proposed change to the treatment of Part D CGDP payments. | Would lengthen the time spent in the coverage gap and potentially increase the plan’s overall claim liability under the current Part D benefit. | No effect. Not applicable to RDS program. |

The following sections describe each of these items in more detail, as well as other historical and proposed changes impacting the relative value of EGWPs and RDS plans.

Reduction to the Part D direct subsidy

The financial positioning of EGWPs compared with RDS plans depends on a number of factors, including the value of the various Part D subsidies, such as the:

- Risk-adjusted direct subsidy,

- Federal reinsurance subsidy, and

- Coverage Gap Discount Program (CGDP) subsidy.

The latter two subsidies are based on the EGWP’s own experience and therefore can be projected and estimated based solely on each EGWP’s experience. This differs from the direct subsidy, where EGWP revenue is based on individual Medicare Part D plan bid submissions and can be more difficult to predict.

The direct subsidy steadily decreased each year since 2011. Key drivers of this decrease include member migration to lower-cost plans, competitive forces driving bid reductions, and increased federal reinsurance subsidies. As the direct subsidy decreases, the financial advantage of EGWPs may decline because it does not impact the RDS. Figure 3 summarizes the change in the national average direct subsidy per member per month (PMPM) in recent years.3

Figure 3: Medicare Part D Direct Subsidy (PMPM)

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

| Direct Subsidy | $53.42 | $48.47 | $43.46 | $37.05 | $30.56 | $25.45 |

| Decrease From Prior Year ($) | $4.95 | $5.01 | $6.41 | $6.49 | $5.11 | |

| Decrease from Prior Year (%) | 9% | 10% | 15% | 18% | 17% |

The direct subsidy is risk-adjusted such that the actual direct subsidy revenue each EGWP receives is based on the relative morbidity of the beneficiaries in each plan as demonstrated by their Centers for Medicare and Medicaid Services (CMS) risk scores. Given this, the impact of the declining direct subsidy will vary by group.

Beneficiaries in group retiree plans are typically healthier than the average Medicare-eligible beneficiary. As a result, we typically observe lower risk scores for EGWPs compared with those for individual Part D plans. The lower-than-average risk score reduces the direct subsidy values in Figure 3 for EGWPs when compared with individual Part D plans.

Each year, CMS may implement changes to its risk score model. These changes may impact risk scores differently for the non-low-income (NLI) and low-income (LI) populations. Because EGWPs predominantly provide coverage to NLI beneficiaries, changes to the CMS risk score model for the NLI population may be particularly impactful on the value of EGWPs and their direct subsidy revenues. The CMS risk score model changes do not affect the RDS.

Increasing specialty trends

Federal reinsurance payments increased dramatically in recent years due to high inflation for brand and specialty products and new high-cost specialty launches, including the highly publicized hepatitis C medications. The CMS federal reinsurance subsidy reimburses EGWPs for 80% of the eligible pharmacy costs, net of direct and indirect remuneration (DIR),4 in the catastrophic phase of the Part D benefit. Figure 4 summarizes the increasing average Part D federal reinsurance subsidy in recent years. While EGWP federal reinsurance is based on plan-specific claims, Figure 4 illustrates the impact of high-cost medications on the federal reinsurance payments underlying individual Medicare Part D bids.

Figure 4: Medicare Part D Federal Reinsurance Subsidy (PMPM)

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

| Federal Reinsurance Subsidy | $37.38 | $42.60 | $51.26 | $59.74 | $69.07 | $78.65 |

| Increase from Prior Year ($) | $5.21 | $8.66 | $8.48 | $9.32 | $9.58 | |

| Increase from Prior Year (%) | 14% | 20% | 17% | 16% | 14% |

As brand and specialty costs continue to escalate, more beneficiaries satisfy the true out-of-pocket (TrOOP) threshold of the Part D benefit and thus enter the catastrophic phase of the Part D benefit. From the plan sponsor’s perspective, the EGWP federal reinsurance protection provides a key advantage relative to plans collecting the RDS. This is because the federal reinsurance payment that EGWPs receive is not subject to a maximum cost limit, while the RDS is limited and therefore does not increase for high-cost claimants once the threshold is met.

Specialty utilization is expected to continue to increase in the coming years, placing greater value on the catastrophic protection provided by EGWPs.

Changes to the EGWP claim adjudication methodology

Clarifications to the EGWP claim adjudication requirements in recent years mitigated some of the financial advantage of EGWPs. In December 2013, CMS issued guidance effective in 2014 on the adjudication of straddle claims near the TrOOP threshold.5 Straddle claims are those claims beginning in the coverage gap that would end in the catastrophic phase after application of the defined standard benefit.

The CMS-required adjudication approach lengthens the coverage gap, which generally increases the plan liability while reducing federal reinsurance. Under the prior approach employed by several PBMs, the CGDP payment was calculated based on total allowed pharmacy cost. This contrasts with the CMS approach, which calculates the CGDP payment based on the lesser of the total allowed pharmacy cost and the remaining amount needed to reach the TrOOP threshold.

This dynamic delays the point at which beneficiaries satisfy the TrOOP threshold. The effect of the revised straddle claim adjudication logic varies significantly by plan and is a function of the plan’s member cost sharing and the underlying utilization of its beneficiaries. Plan sponsors should consider certain benefit design features to minimize net costs under the straddle claim adjudication logic. This revised adjudication logic does not affect the RDS.

Potential regulatory changes

Emerging trends and potential changes may also impact the relative value of EGWPs and RDS plans. Examples of future regulatory and market dynamics impacting the relative value of EGWPs and RDS plans include:

-

Federal reinsurance payment modifications. MedPAC is closely scrutinizing the Part D federal reinsurance program. In the June 2016 Report to Congress, MedPAC recommended reducing the federal reinsurance subsidy from 80% to 20%.6 This reduction in federal reinsurance program payments would impact the financial position of EGWPs; however, this reduction would likely be accompanied by an offsetting increase in direct subsidy revenue. Because federal reinsurance is based on plan-specific experience and EGWP direct subsidy revenue is based on the individual Medicare Part D market, the net effect of this proposal on EGWPs will depend on the plan sponsor’s population. The net effect will also depend on the extent to which there is a corresponding CMS risk adjustment model recalibration, among other factors.

The current federal reinsurance program provides EGWPs with significant protection from catastrophic claims. Given the maximum cost limit in place on the RDS, this current protection increases the value of an EGWP relative to the RDS plan, all else equal. If the proposed reinsurance modification is implemented, EGWPs will no longer have as large of an advantage in terms of catastrophic claim protection (when compared with RDS plans). While EGWPs will continue to offer plans some federal reinsurance protection under MedPAC’s proposal, the proposed amount will be a material reduction from the current level and EGWPs will need to focus more on their management of high-cost beneficiaries. -

Modification of the treatment of CGDP payments. EGWPs are eligible to receive the 50% manufacturer discount on eligible brand drug costs through the Part D Coverage Gap Discount Program (CGDP) for NLI individuals. The EGWP is structured to allow plans to offer reduced member cost sharing while still maximizing CGDP payments, significantly benefiting EGWPs from a financial perspective.

Although CGDP payments are paid by pharmaceutical manufacturers rather than by members, these significant amounts still accumulate toward the member’s TrOOP. This accelerates the member’s transition to the catastrophic phase of the Part D benefit, where the plan sponsor’s liability is typically lower than it is in the coverage gap phase under the current Part D benefit. Because EGWP benefit designs tend to be richer than individual plans, the CGDP’s role in transitioning members to the catastrophic phase of the benefit makes it an important and meaningful catalyst in reducing EGWP premiums. MedPAC’s June 2016 Report to Congress proposed that the CGDP payments no longer count toward the member’s accumulation of costs toward TrOOP. If enforced, EGWPs may see future cost increases because of reduced federal reinsurance payments as members reach the catastrophic phase of the benefit more slowly, or not at all, under the current Part D benefit. This singular change could significantly alter the relative value of EGWPs and RDS plans from a plan sponsor’s perspective.

MedPAC’s June 2016 Report to Congress proposed additional changes to the Medicare Part D program, including a modification to member cost sharing in the catastrophic phase of the benefit and changes to the formulary restrictions currently in place. The impact of these proposals on EGWP plan liability will vary based on whether these changes are adopted in isolation or in conjunction with one another. Plan sponsors should monitor the effect of these and other future changes on their group retiree pharmacy benefit programs.

Other considerations

Benefit managers should evaluate the impact of recent regulatory and market dynamics on the subsidies generated under the RDS and EGWP approaches. When considering the relative value of each approach, benefit managers should additionally consider the administrative responsibilities associated with EGWPs and RDS plans, as well as other financial drivers impacting EGWPs and RDS plans.

-

Administrative responsibilities: Plans must submit subsidy applications, along with claim data, and demonstrate actuarial equivalence to receive the RDS. RDS plans must also conduct creditable coverage testing and notify enrollees (and CMS) of their creditable coverage status.

EGWPs must meet benefit and formulary coverage requirements to comply with the regulations applying to all Part D plans. Plan costs may be higher under an EGWP arrangement if the plan’s current formulary is more restrictive than required by CMS. EGWP benefit design and administration is highly technical and requires dedicated resources to ensure plans are fully compliant with federal regulations, often resulting in higher administrative costs. - Cash flow timing: As of 2017, CMS will pay a prospective reinsurance payment to calendar-year EGWP Part D plans. This payment will be $26.507 per member per month in 2017, with plans subject to reconciliation based on actual amounts after the end of the plan year, creating a cash flow disadvantage as federal reinsurance becomes a greater component of EGWP revenue. The introduction of a prospective reinsurance payment improves EGWP cash flow timing relative to the current environment.

- Financial reporting: For public sector entities, accounting standards create an additional advantage to offering EGWPs. Both public and private sector entities are required to account for future liabilities due to other post-employment benefits (OPEB). While private sector plan sponsors can reduce the OPEB liability for RDS savings, under the Governmental Accounting Standards Board (GASB) Statements 43 and 45, public sector plan sponsors cannot. However, GASB 43 and 45 regulations allow recognition of all future subsidies for EGWPs. Therefore, a public sector plan sponsor’s unfunded liability may significantly decrease if it switches from an RDS plan to an EGWP arrangement. This perception of value associated with a lower OPEB liability may make EGWPs a more attractive option for public sector entities.

Conclusion

The group retiree pharmacy benefits market continues to evolve over time. Recent and future market and regulatory changes affect the relative financial values of RDS plans and EGWPs. Plan sponsors should monitor the effect of emerging trends and changes on their group retiree pharmacy benefit plans. Periodic evaluation of the RDS and EGWP arrangements could help optimize plan sponsor value in an evolving retiree pharmacy landscape.

Disclosures

This communication has been prepared for the specific purpose of discussing recent changes and opportunities in the group retiree pharmacy benefits market in the United States. This information may not be appropriate, and should not be used, for any other purpose. The opinions expressed are those of the authors and not of Milliman or all Milliman consultants. Milliman does not intend to benefit or create a legal duty to any third-party recipient of its work. This communication must be read in its entirety.

In performing this analysis, we relied on data and other information from CMS. We have not audited or verified this data and other information but reviewed it for general reasonableness. If the underlying data or information is inaccurate or incomplete, the results of our analysis may likewise be inaccurate or incomplete. Milliman does not provide legal advice and recommends readers of this communication consult with their legal advisors regarding legal matters.

Contact

If you have any questions or comments on this document, please contact the authors or your Milliman consultant.

Michelle N. Angeloni, FSA, MAAA

[email protected]

+1 860 687 0168

Tracy A. Margiott, FSA, MAAA

[email protected]

+1 860 687 0169

1Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical insurance Trust Funds (June 22, 2016). 2016 Annual Report, p. 145. Retrieved July 29, 2016, from https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2016.pdf.

2While some changes do not directly impact the financial position of RDS plans, any change that impacts the defined standard Part D benefit may affect RDS creditable coverage testing, which may result in required changes to RDS benefits or pricing.

3CMS.gov (July 29, 2016). Medicare Advantage Rates & Statistics: Annual Release of Part D National Average Bid Amount and other Part C & D Bid Related Information. Retrieved July 29, 2016, via https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/PartDandMABenchmarks2017.pdf.

4DIR includes pharmacy manufacturer rebates and payments from pharmacies to plan sponsors.

5CMS (December 2013). Prescription Drug Event (PDE) reporting examples for benefit year 2014, p. 34. Retrieved July 29, 2016, from http://www.csscoperations.com/internet/cssc3.nsf/files/2014%20PDE%20Reporting%20

Guidance%2012-13-2013.pdf/$FIle/2014%20PDE%20Reporting%20Guidance%2012-13-2013.pdf.

6MedPAC (June 2016) Report to the Congress: Medicare and the Health Care Delivery System. Retrieved July 29, 2016, from http://medpac.gov/docs/default-source/reports/june-2016-report-to-the-congress-medicare-and-the-health-care-delivery-system.pdf?sfvrsn=0.

7CMS (April 4, 2016). Announcement of Calendar Year (CY) 2017 Medicare Advantage Capitation Rates and Medicare Advantage and Part D Payment Policies and Final Call Letter. Retrieved July 29, 2016, from https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/Announcement2017.pdf.