Key Points

- Diversification is just one risk management tool, not a comprehensive risk management solution.

- Multiple asset classes won’t lower portfolio risk when the same factors drive each asset classes’ investment returns.

- Diversification cannot provide protection against systematic risk, such as a global recession, when all major asset classes tend to fall in unison.

- Derivatives such as futures, which offer significant liquidity and transparency, can be used as a cost-effective second-layer safeguard against volatile markets and potential capital losses.

Risk comes in many forms but investors are acutely aware of two: the impact of capital losses and extreme bouts of volatility.

Both can have a devastating impact on a portfolio.

Capital losses, such as we saw during the global financial crisis, may never be recouped by some unlucky investors. Meanwhile, volatility can prompt investors to withdraw their money at just the wrong time or quickly erode a lifetime’s savings when an investor is drawing down their capital.

The solution offered by the financial services industry typically involves well-intentioned advice to stay invested for the long-term and diversify your portfolio.

While such recommendations have merit, they also ignore several shortcomings of diversification.

When diversification doesn’t work

Diversification has been a central tenant of portfolio construction since the early-1950s when Harry Markowitz developed Modern Portfolio Theory. It tells us that investing is not just about picking the right asset classes, it’s also about selecting the right combination of asset classes.

Most investors understand that by combining a range of asset classes with low correlations – spreading risk around – overall portfolio volatility can also be lowered.

Unfortunately, the practical implementation of this concept leaves much to be desired. Investors have all too often found that when ‘growth’ assets decline, their entire portfolio slumps, and that the correlation between ‘growth’ and ‘defensive’ assets is often greater than they believe.

This is because the investment returns of a range of asset classes are driven by many of the same factors. These can include: economic growth; valuation; inflation; liquidity; credit; political risk; momentum; manager skill; option premium; and demographic shifts.

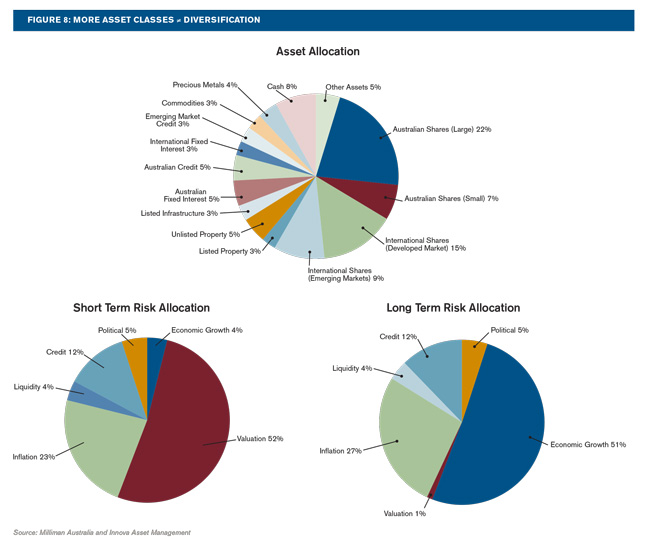

So while investors have added a range of asset classes to their portfolio (such as property, infrastructure, distressed debt, and commodities) their portfolio risk remains similar at the expense of adding greater complexity and management cost.

More Asset Classes Does Not Equal More Diversification

A number of studies have found benefits to this risk factor approach. For example, a 2009 study applied an equal weighting across 11 style and strategy risk premia from 1995 to 2008 to produce similar returns to traditional 60/40 portfolios but with 65 per cent less volatility .1

A failure to evaluate the true underlying risk factors across various asset classes is not the only shortcoming of diversification.

The impact of systematic risk can be even more destructive.

These are risks which cannot be diversified away, such as the impact of war or a global recession. In these circumstances most asset class returns slide in tandem, just as we saw during the global financial crisis of 2007-08.

GFC Returns

| 2007 return (%) | 2008 return (%) | |

| Australian Shares | 16.07 | -38.44 |

| International Fixed Interest | 7.03 | 13.41 |

| Cash | 6.77 | 7.60 |

| Australian Fixed Interest | 3.46 | 14.95 |

| Australian Infrastructure | 3.08 | -13.56 |

| International Shares | -2.60 | -24.92 |

| A-REITs | -8.41 | -53.99 |

| Source: Goldman Sachs Asset Management | ||

Correlations between asset classes have become particularly pronounced during times of stress due to the impact of globalisation across industries, markets and economies.

When US and World ex-US stock markets were performing strongly (up more than one standard deviation above their respective full sample mean between January 1970 and February 2008) they showed a low correlation at -17 per cent2.

However, when markets were down (by more than one standard deviation) the correlation between US and World ex-US stock markets was significantly higher at 76 per cent over the same time period.

Average Cross-Correlations (March 1994 – December 2009)

A multi-tiered solution

Effective risk management begins with diversification – but it does not end there. It forms the basis of risk management but only when investors are able to make a true assessment of each asset classes’ underlying risk factors.

But even at this level, investors are still exposed to systematic risk. Many investors simply don’t have the time or the fortitude to ride out such devastating market downturns as the GFC. As we have seen, the Australian sharemarket has still not returned to its pre-GFC high despite the passing of several years3.

A second layer of risk management can smooth out volatility and attempt to protect against severe capital losses by intelligently using derivatives such as futures.

Companies and investors regularly hedge their risks across sectors including equities, FX, interest rates, metals, energy, and commodities in the futures market, which accounts for over $US1 trillion per day in contract value.

Financial futures contracts are simply contractual agreements to buy or sell a financial instrument at a predetermined price in the future and, in the hands of large institutional investors, can form a particularly cost-effective safeguard.

This risk management approach, often implemented as a low-cost overlay, allows investors to maintain their exposure to the bulk of potential returns from traditional ‘growth’ assets while seeking to minimize the risk of excessive volatility and catastrophic market downturns.

While options are significantly more expensive and offer less depth and flexibility than futures, they can be employed as the last piece in the risk management puzzle to safeguard against unlikely events such as ‘gap risk’.

This multi-tiered approach offers significant benefits to traditional risk management approaches which were exposed during the GFC. It gives investors greater certainty at low-cost while allowing them to retain the bulk of returns.

1 Briand R., Nielsen F., Stefek D., 2009, ‘Portfolio of Risk Premia: A New Approach to Diversification’, MSCI Barra Research Insights, January 2009.

2PIMCO: ‘The Myth of Diversification: Risk Factors vs. Asset Classes’. 2010.

3The S&P/ASX 200 peaked at 6828.70 points in November 2007. At December 1, 2015, it closed at 5266.10 points.

Milliman is a global risk management and retirement expert. Its risk management processes are employed across more than $US150 billion in assets and it counts fund managers, insurers, private businesses, government, education and non-profit organisations among its partners.

Issued by Milliman Pty. Ltd. (Milliman AU) (ABN51 093 828 418) (AFSL 340679) Please contact Milliman to obtain more information about the products and services we offer as not all products and services may be suitable for you.

The Milliman Managed Risk Strategy is available only to persons who meet the requirements for a "wholesale client" under the Corporations Act and trustees of superannuation funds with net assets of at least A$10 million (Clients). Clients must have an agreement with Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman) to implement the strategy (Service) against a portfolio of the Client's equity investments (such as listed shares), which enables the Client to use the Service or to offer the Service to members of the Client's superannuation fund.

Milliman makes no recommendation and gives no statement of opinion to Clients, members of Clients' superannuation funds or their respective advisers in relation to use of, or any investments, in the Service. Before considering whether to use the Service, Clients may wish to obtain professional advice (including taxation advice). Investments in, the Service are subject to market and other risks, and no guarantee or assurance is given by Milliman that such investments will not give rise to losses or that performance of the Service will completely reflect inversely the performance of equities markets generally or a Client's portfolio of equity investments. While generally assets which are acquired through use of the Service will be liquid, this may not be the case in all circumstances. Further, during periods of sustained market growth, the return to Clients from the combination of their portfolio of equity investments and assets held in the Service should be less than if the Client did not participate in the Service. Fees and conditions apply to use of the Service.