Recently passed legislation referred to as MACRA (Medicare Access and CHIP Reauthorization Act of 2015 1) will, among other things, affect the Medicare Supplement industry in calendar year 2020. Specifically, the Part B deductible can’t be covered. Therefore, Plan F will no longer be an option for individuals newly eligible for Medicare starting January 1, 2020.2 However, in-force policyholders will be able to keep their current versions of Plan F and individuals eligible for Medicare prior to January 1, 2020 (i.e., not “newly eligible”), can purchase the current version of Plan F on or after January 1, 2020.

For the Medicare Supplement market, the news is mixed. Overall loss ratio experience (and resulting premium rate pressure) could be more favorable for several years following the implementation of MACRA. However, retention dollars (premium less claims) will most likely be reduced due to MACRA.

Individual carriers are in a position now to plan a course to proactively mitigate risks or exploit opportunities. We recommend analyzing the financial impact of MACRA implementation on your Medicare Supplement product portfolio to provide insight into appropriate next steps. Using a model built from our knowledge of the market, we have simulated the future policy issues of Medicare Supplement Plans F and G and observed some interesting insights.

Medicare Supplement market will split into two distinct markets

What we now consider one market for Medicare Supplement will effectively become two markets starting in 2020. We will call them Newly Eligible (NE) and Non Newly Eligible (NNE). This is terminology from the regulatory language that specifies eligibility to purchase Plan F (or Plan C). The NE market will consist of individuals who reach the age of 65 on January 1, 2020, and later. Over time, this market will have an increasing maximum age and a minimum age of 65.3 The NNE market will consist of individuals who reach the age of 65 before January 1, 2020, and an increasing minimum age but no maximum age.

Overall loss ratio experience should be better for a few years following MACRA implementation

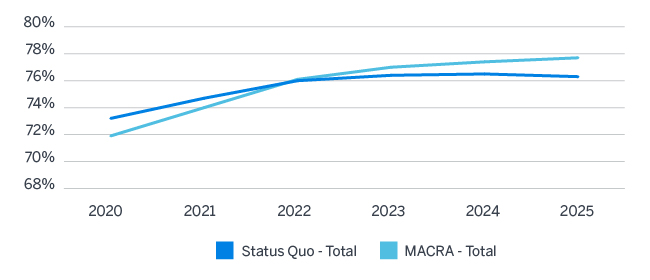

Based on modeling various reasonable scenarios of the Medicare Supplement market, experience on policies issued in 2020 and later should initially exhibit a loss ratio as much as 1.0% - 2.5% lower than would otherwise be the case. The reason is that exposure to the non-medically underwritten higher loss ratio open enrollees will shift from Plan F to Plan G, a lower benefit plan. Therefore, the higher loss ratio business has lower exposure and the overall loss ratio is lower all else being equal. This loss ratio improvement will likely last for a few years and then reverse with portfolio loss ratios realizing a steady increase in future years as Plan G exposure overtakes Plan F. Appendix A illustrates this pattern based on our overall projection of the market with and without the implications of MACRA.

Plan F sales, which will only be available to the NNE market, will consist of a greater portion of healthier underwritten business than under the current environment. Plan F will still be available to NNE individuals under guarantee issue provisions.

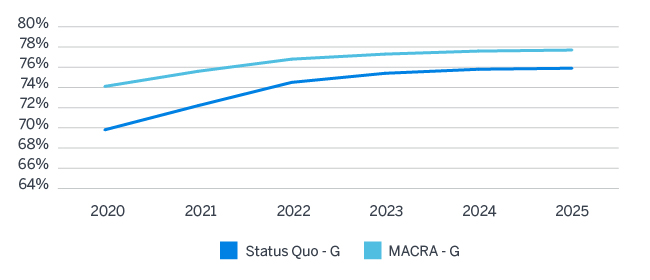

On the other hand, Plan G will likely comprise a greater portion of higher cost/utilization open enrollment and guarantee issue business from the NE market. As the NE market grows and the NNE market shrinks over time, the relative mix of Plan F and Plan G will shift and the market will be more reflective of Plan G experience.

Initially, the favorable underwritten Plan F experience issued at higher rate levels could offset the negative Plan G experience. As time goes by and Plan G becomes an even greater portion of the market, this relatively unfavorable experience will overcome the positive Plan F experience unless corrective action is taken. The aggregate impact may remain positive for numerous years.

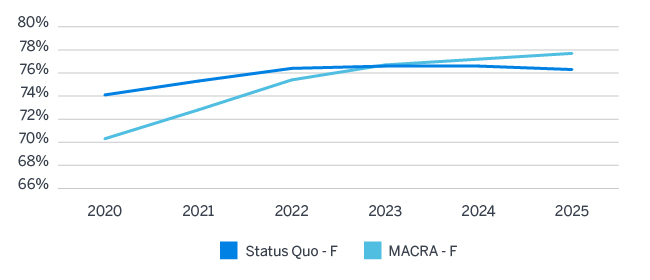

How can MACRA possibly have an overall more favorable impact on experience initially? This scenario occurs if the higher cost/utilization individuals otherwise choosing Plan F under an open enrollment or guarantee issue provision are either forced to or allowed to purchase Plan G at a reduced premium and benefit level. This essentially reduces the exposure for these individuals. Until such time future Plan G sales significantly outpace Plan F sales, these results could continue for several years. However, if there is a complete shift immediately to Plan G regardless of the availability of Plan F, then experience will be worse immediately under MACRA enactment than without MACRA enactment. To demonstrate, Attachment B provides the separate Plan F and Plan G results that make up the total loss ratios for both plans as provided in Appendix A.

In spite of more favorable experience, however, retention dollars are expected to be lower for all years following MACRA implementation

The impact through 2025 could be in excess of $2 billion for only the Plan F/G market. This reflects the profitability on the Part B deductible coverage that goes away.

This is due to a higher proportion of Plan G sales which correspond to both a lower benefit value and a corresponding lower overall premium amount. To the extent administrative expenses reflect a fixed per policy or claim component or corporate overhead component, this will squeeze profit margins and place upward pressure on rate levels, all else being equal.

Specific carrier experience will vary based on particular circumstances

Overall market movement reflects a composite of independent carriers. The experience of a particular carrier will reflect its particular pricing structure and position in the market. This will determine the extent to which market patterns will be replicated or not. There will be carriers on each side of the market pattern. Some will see overall results deteriorate and require additional rate action while others may use this as an opportunity to improve competitiveness.

Key considerations include:

- The volume of pre-MACRA business exposure available to absorb the initial impact at least in the early years

- The relative experience/rating differential of a carrier’s Plan F versus Plan G, including age rate slope

- The relative mix of underwritten, open enrollment, and guarantee issue business before and after MACRA and the relative morbidity level difference among them

- The level of underwriting (i.e., full versus simplified) performed

Company positioning for MACRA starts now

Each carrier will have its own unique circumstances and position in the market along with unique experience levels, sales targets, and rating structure. The time to begin the process of positioning your Medicare Supplement product for 2020 is now. Policy development and rating decisions will need to be finalized well in advance of the end of 2019 for plans sold in 2020.

What steps should carriers take to position themselves in anticipation of future claim shifts?

MACRA will undoubtedly change the demographic mix of different plans in opposite directions. The impact on claim levels can be estimated by modeling future results reflecting current demographics and underlying experience along with the expected impact of MACRA. Model results provide a guide to quantify the need for future rate action and could help answer the following questions:

- Is this an opportunity to scale back on Plan F rating action in anticipation of future shifts and by how much?

- What is the right balance to be able to strengthen Plan G rate levels in anticipation of MACRA while at the same time remain competitive in this new environment?

What market opportunities are available both before and after 2020?

The implementation of MACRA will undoubtedly change the Medicare Supplement landscape. There are multiple potential scenarios to recognize for both existing carriers and potential new entrants. Scenarios to consider and analyze may consist of the following:

- Will Plan G sales increase as new carriers enter the market with a focus on Plan G?

- Or will consumer education and agent/broker influence result in a “run” on Plan F sales to a greater degree than exists even today?

- At what point will the market anticipate the impact of MACRA and narrow the F/G gap in pricing?

Whether a carrier has a large volume of Medicare Supplement exposure or is a new market entrant, MACRA will have an impact. While Plan G will ultimately replace Plan F, there is still a place in the market for Plan F in the near future. A carrier’s ability to properly position these respective plans will require “2020” vision.

Limitations

Projection results reflect a limited set of plausible scenarios. Future results that emerge will differ from projection assumptions. The intent of projecting future experience under various feasible assumptions is to identify the likely pattern and timing of Medicare Supplement experience in 2020 and beyond due to MACRA legislation. Specific carrier experience will vary based on particular circumstances.

Guidelines issued by the American Academy of Actuaries require actuaries to include their professional qualifications in actuarial communications. I, Kenneth L. Clark, am a consulting actuary for Milliman, Inc. and am a member of the American Academy of Actuaries. I meet the qualification standards of the American Academy of Actuaries to render the analysis contained herein.

The opinions expressed in this report are those of the author alone and do not necessarily reflect the opinions of Milliman or other employees of Milliman.

Appendix A

Projected Loss Ratios Plans F and G - 2020 and later issues

Key Assumptions for this scenario

- Issue Status Distribution (UW/OE/GI):

- Plan F: 40%/40%/20%

- Plan G: 50%/50%/0%

- Issue Status Morbidity Relativities (UW/OE/GI): 1.0/1.1/1.3 excluding UW selection

- UW selection factors by duration for UW status

- Year 1 – 75.0%

- Year 2 – 87.5%

- Years 3+ – 100.0%

- Annual sales (before MACRA Impact) as a % of Medicare FFS

- Plan F: 3.0%

- Plan G: 1.1%

- Current market based on MFA Medicare Supplement database consisting of NAIC source data.4

Appendix B

Projected Loss Ratios Plan F - 2020 and later issues

Projected Loss Ratios Plan G - 2020 and later issues

1Public Law 114-10—Apr. 16, 2015; 129 Stat. 87. Congressional Record. Vol. 161 (2015). Retrieved January 21, 2016, from https://www.congress.gov/114/plaws/publ10/PLAW-114publ10.pdf

2The same fate will impact Plan C. However, for purposes of our discussion, we will focus on Plan F.

3For the sake of this discussion we are ignoring under age 65 Medicare enrollees.

4Health Coverage Portal™ by Mark Farrah Associates, Medicare Supplement Insurance Experience Exhibit data as filed in NAIC Annual Statements.