“ACA risk adjustment management: Going all-out” is the first article in the risk adjustment management series and should be read before the remaining three articles.

Keeping score permeates our society—from baseball standings to sibling rivalries. As a leader within your health plan, are you doing the same? Do you truly have a handle on your score? If not, it could be costing your company competitive positioning, membership, and revenue.

Most corporate initiatives rely upon unbiased and frequent measurement to confirm how closely results are tracking with expectations. Risk adjustment activities should not be different. Risk adjustment management within the Patient Protection and Affordable Care Act (ACA) framework not only focuses on developing and maintaining revenue-generating activities (e.g., coding accuracy and completeness initiatives, prospective member outreach, and data validation and auditing), but also dedicates sufficient time to measuring and reporting results. Without this feedback, decisions in your company will be made in a vacuum and without consciously tying back to overall company goals.

This is one of three topic-specific papers in our series on ACA risk adjustment management.1 Here, we explore a few of the more useful types of analytics your commercial health plan can leverage to monitor the performance of your ACA block and help you better keep (risk) score.

Laying the ground rules

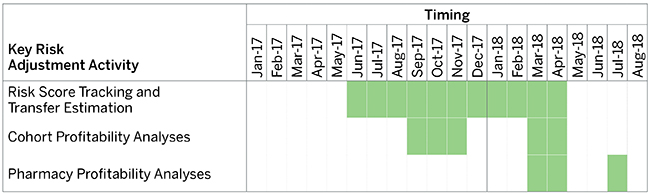

Throughout this series, we have emphasized the importance of timing in all aspects of risk adjustment program management. Risk analytics can begin as early as the middle of the benefit year, overlapping the first half of the following year, with frequent interim refreshes. Figure 1 presents a sample timeline for benefit year 2017 activities.

Figure 1: Sample Risk Analytics Timeline for Benefit Year 2017

We find health plans receive the highest value from focusing on three categories of analytics—monthly risk score tracking and risk transfer estimation, cohort-based profitability analyses, and pharmacy profitability studies. The subsequent sections highlight each of these categories and touch on the following key questions:

- The “What?” The “Why?” The “When?”

- Who owns it? Who else needs to be involved?

- Is there anything else I should think about?

Upon completion, we hope to have instilled a deeper appreciation for tracking and managing risk and to have provided the foundations for introducing these initiatives within your organization.

Risk score tracking and risk transfer estimation

The “What?” The “Why?” The “When?”

Understanding ACA risk scores and transfer payments calculated from the U.S. Department of Health and Human Services Hierarchical Condition Category (HHS-HCC) model is the first of a number of analyses driving strategic decisions. Simply put, all risk adjustment analytics rest on having an accurate and complete picture of the company’s risk position now, at year-end, and in future plan years.2

A comprehensive process will include estimates of risk transfer dollars. All too often, an issuer will shortcut estimation and incorporate prior-year transfer results into forecasts or financial reporting. The inherent volatility in year-over-year risk transfers, especially for smaller health plans, makes this practice unreliable.3

Acquiring an initial view of the risk score in June of the current benefit year strikes a good balance of allowing experience to mature without waiting too long, when a potential adjustment to internal processes or projections becomes difficult (or even impossible). Because the risk scores support a variety of functions, monthly refreshes are recommended. Given the complexity of translating risk scores into transfer payments, most issuers will defer this calculation until later in the year when scores are more complete and after the Centers for Medicare and Medicaid Services (CMS) has released the annual risk adjustment report from the prior benefit year (which often serves as the starting point for estimating statewide average risk scores).4

Who owns it? Who else needs to be involved?

Risk scoring and transfer estimation requires intimate knowledge of the risk adjustment formula and how future CMS updates will affect both the issuer and the market. Therefore, ownership should reside with the lead of firm-wide risk analytics or with actuarial and/or finance areas if no such analytics function exists. Ultimately, though, the chief financial officer (CFO) is responsible for the best estimate risk transfer and gaining buy-in from the executive team on the final amount reported. Many other departments, such as the product lines, pricing, marketing, and customer service, will need to be prepared to react to the internal and external forces stemming from the decisions related to risk analytics.

Is there anything else I should think about?

The main hurdle for robust analytics, surprisingly, is developing the risk scores. CMS maintains a publicly available code set for the HHS-HCC model, dubbed the “Do It Yourself (DIY)" tool.5 This tool requires a SAS license and programming expertise, which likely means involvement from the information technology (IT) department. Given the centralized role of any internal risk-scoring model, the area leading risk analytics must be consulted for tool design and even leveraged for testing.

As mentioned earlier, calculating a transfer payment is complicated, and the greatest struggle is determining a reasonably accurate expectation of marketwide transfer components. Published information from CMS can form the foundation of such expectations—and there are now three full years of transfer metrics available to carriers. Nonetheless, the continued volatility of ACA markets, driven by unknown levels of risk and the constant churn of members within these markets, has made estimating state averages challenging even now.

Another hurdle is assessing the impact of annual HHS-HCC model recalibrations by CMS and other revisions from regulatory changes via congressional or executive action. In both 2017 and 2018, published changes to the model6 and unanticipated guidance7 have been significant and have made projecting risk scores much more difficult. To add to this difficulty, CMS has not historically delivered preliminary DIY software until the second half of a given benefit year. Those seeking a head start may need to evaluate the trade-off between making changes to the DIY software themselves and leveraging an external partner to provide a timelier and potentially more cost-effective solution.

Lastly, the DIY tool does not reflect year-end risk scores, and issuers must complete and annualize risk score factors to acquire a full-year picture. Health plans are already conceptually familiar with this process for incurred claims, but risk scores complete and annualize differently and require a different set of factors. The DIY software also does not include conditions residing outside a claim system in External Data Gathering Environment (EDGE) supplemental diagnosis files. This information would need to be incorporated through a separate means.

Cohort-based profitability analyses

The “What?” The “Why?” The “When?”

The traditional view of member profitability (i.e., claims and expenses vs. premium) changed when the ACA introduced risk adjustment transfers. Now, an individual whose claims exceed the premium paid may still be “profitable” if risk adjustment provides appropriate compensation to offset the rate shortfall.

Cohort profitability analysis starts with raw loss ratios for virtually any segment of business (specific demographic groups, member exchange status, metallic tiers, or plan variants) and then removes the estimated impact of cost-sharing reduction (CSR) recoveries8 and risk transfers. This adjusted loss ratio provides a more accurate view of key profitability drivers to any desired level of specificity. It is certainly possible that no meaningful action can be taken to offset the risk of any particular segment, but cohort profitability provides the holistic intelligence necessary to aid strategic conversations.

At a minimum, these analyses should occur near the end of the current benefit year to provide an initial look at plan performance and should then be refreshed a few months later (when runout is sufficient) to inform rate and form filing decisions. However, issuers should assess cohort profitability any time alternative courses of action are under consideration.

Who owns it? Who else needs to be involved?

Cohort profitability is an extension of risk scoring and transfer calculations and, therefore, is likely owned within the same area. The number of stakeholders is also extensive. Sales and marketing will be intimately involved in plan design or portfolio decisions, finance will incorporate results into forecasting and projections, and the executive team will gauge the financial health of certain segments to drive service area definition, exchange participation, and market entry and exit decisions.

Is there anything else I should think about?

By its nature, cohort profitability views segments in isolation, but the decisions that follow cannot do the same. An issuer should recognize that any action could have far-reaching implications. For example, discontinuing a metallic offering, pulling off the exchange, or exiting the ACA completely could have ripple effects within the broader market or could dramatically shift the risk profile of the issuer’s remaining portfolio. Profitability is an important measure of financial health, but is not the only item affecting a company’s direction. Interestingly, cohort analytics may be instrumental in shaping the course of action but are equally important in measuring the short-term and long-term outcomes of those same decisions.

Pharmacy profitability studies

The “What?” The “Why?” The “When?”

Pharmacy analytics are conceptually similar to cohort profitability but carried out at the prescription drug level to understand the correlation between prescription medication usage and financial outcomes. If warranted, an issuer can probe further into drivers of those outcomes—whether from plan cost sharing, benefits, or access to medication.

Recently, CMS increased focus on pharmacy coverage by first publishing issuer-level formulary information for all ACA participants9 and then introducing certain prescription medications into the 2018 HHS-HCC model.10 With more information available in the market and a higher impact on an issuer’s financial position, pharmacy profitability analytics will be a key input into projections moving forward.

Pharmacy analytics best serve strategic planning before premium rate setting and form-filing activities are underway, with timing somewhat dependent on a state’s deadline. However, even after rate submission, there are usually a few months during state and federal review where an issuer can refresh the analysis and incorporate emerging information about risk score markers, formulary regulations, pharmacy contracts, and the coverage decisions of other carriers. These updates may help avoid a surprise adverse deviation in experience and allow for state-approved changes before premium rates for the next benefit year are completely finalized.

Who owns it? Who else needs to be involved?

Pharmacy analytics involve both internal and external parties. An issuer should consider the interactions between the following areas:

- Pharmacy benefits manager (PBM): For those not utilizing in-house resources, a PBM sets the formulary and negotiates rebates with manufacturers on behalf of a health plan. Because many smaller health plans do not contract with PBMs for custom formularies, the results of pharmacy profitability analyses could incentivize these issuers to push for more control in formulary design or for stronger rebate arrangements.

- Pharmacy management operations: For issuers with an in-house pharmacy operation and clinical team, the risk management area should collaborate with these experts for strategy around formulary changes, clinical programs, and therapeutic alternatives that would optimize risk scores.

- Actuarial/finance: These stakeholders will have acute interest in the projected impacts of both PBM contracts and risk transfer estimates to integrate into financial forecasts.

Is there anything else I should think about?

The challenge with prescription drug analyses, as with most pharmacy analytics, is acquiring an accurate picture of net drug cost, which includes claim reductions such as rebates. Although issuers may not have this information with 100% certainty, reasonable estimates can still provide a useful picture of where pharmacy spend may be driving adverse financial performance after risk adjustment.

Navigating pharmacy solutions can be challenging. When making formulary decisions, it is critical to ensure actions do not unfairly restrict access to medications or otherwise run afoul of discrimination testing requirements. Issuers may have some control in prescription drug coverage and should explore formulary alternatives or clinical programs with their PBMs to maximize risk scores while still satisfying federal and state regulations.

Always know the score

Understanding risk adjustment starts with a risk score and ends with a wide array of tracking, measurement, and analytics to help drive key decisions. Health plans perform these types of analyses every day and do not think twice about calculating reserves, projecting claims, or regularly breaking down sales figures. However, it has been our experience that many fall short in their efforts to truly know their risk scores and understand what they mean for their business. Given the potential financial impacts, this is not an area to be overlooked.

Knowing your score in ACA risk adjustment requires a very specific level of expertise and familiarity with the right tools. But with the backing and dedication of key decision makers and proper oversight, any issuer can leverage the analytics we presented and use them in concerted efforts to optimize financial outcomes and forge a path that will ensure the company’s long-term success in the ACA marketplace.

1

http://www.milliman.com/insight/2017/ACA-risk-adjustment-management-Going-all-out/

http://www.milliman.com/insight/2017/ACA-risk-adjustment-management-Higher-EDGE-ucation/

http://www.milliman.com/insight/2017/ACA-risk-adjustment-management-Cracking-the-code/

2Focusing purely on risk scores in the current benefit year is not sufficient. Issuers should consider modeling risk scores based on CMS guidance for future benefit years, which can provide valuable insight into how model updates may change risk scores over time.

3Vandagriff, A., Petroske, J., Fink, K., & Krienke, N. (June 15, 2016). Sizing Up ACA Risk Adjustment Volatility: How the Interplay Between Risk Adjustment and Issuer Size Influences Profitability Under the ACA. Milliman White Paper. Retrieved November 6, 2017, from https://www.milliman.com/en/insight/sizing-up-aca-risk-adjustment-volatility-how-the-interplay-between-risk-adjustment-and-is.

4For example, the CMS 2016 risk adjustment summary report released on June 30, 2017, at: https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/Summary-Reinsurance-Payments-Risk-2016.pdf.

5CMS. HHS-Developed Risk Adjustment Model Algorithm "Do It Yourself (DIY)" Software Instructions. Retrieved December 8, 2017, from https://www.cms.gov/CCIIO/Resources/Regulations-and-Guidance/Downloads/DIY-Instructions-2017.pdf.

6Vandagriff, A., Hunter, M., Petroske, J., & Klein, M. (August 2017). The "Rxisk" of Adjustments in 2018 ACA Risk Adjustment. Milliman White Paper. Retrieved November 6, 2017, from /-/media/Milliman/importedfiles/uploadedFiles/insight/2017/rx-2018-aca-risk-adjustment.ashx.

7Although CMS has made no formal proposal, see the notice of August 10, 2017, as an example of potential changes to the risk adjustment program to account for unanticipated shifts in ACA legislation, rules, or guidance, at: https://www.regtap.info/uploads/library/QHP_FAQ_5CR_081117.pdf.

8At the time of publication, the future of CSR subsidy funding is currently uncertain, and any analysis needs to recognize and account for the current funding status of CSR members. Refer to these publications for more details surrounding the issue: "A Bridge Too Far? The Most Likely Fates of ACA CSR Payments and Impacts on the Individual Market" (at /-/media/Milliman/importedfiles/uploadedFiles/insight/2017/aca-csr-payment-likely-fates.ashx) and "The Risk and the Adjustment: Managing ACA Marketplace Selection Risk If Cost-Sharing Reductions Fall Short" (at https://www.milliman.com/en/insight/the-risk-and-the-adjustment-managing-aca-marketplace-selection-risk-if-cost-sharing-reduc).

9CMS (December 16, 2016). 2018 Letter to Issuers in the Federally-facilitated Marketplaces. Center for Consumer Information and Insurance Oversight. Retrieved November 6, 2017, from https://www.cms.gov/CCIIO/Resources/Regulations-and-Guidance/Downloads/Final-2018-Letter-to-Issuers-in-the-Federally-facilitated-Marketplaces.pdf.

10Federal Register (December 22, 2016). Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters for 2018; Amendments to Special Enrollment Periods and the Consumer Operated and Oriented Plan Program. Retrieved November 6, 2017, from https://www.federalregister.gov/documents/2016/12/22/2016-30433/patient-protection-and-affordable-care-act-hhs-notice-of-benefit-and-payment-parameters-for-2018.