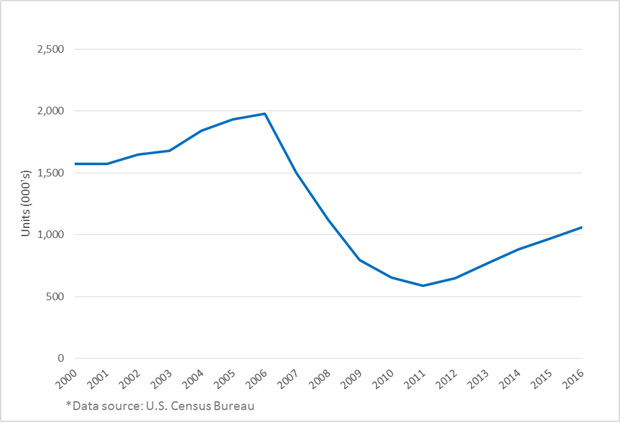

The U.S. Census Bureau and the U.S. Department of Housing and Urban Development recently released their Monthly New Residential Construction report for August 2017. While housing completions are down for the month, completions have continued to rise annually since 2011, and 2017 is on pace to show an increase over 2016. 1

Figure 1: Privately owned housing units completed

Construction defect claims are not typically reported for a number of years, often up to 10, after completion of a home. Given the reporting lag and six straight years of new housing growth, it seems reasonable to expect an increase in construction defect claims in the foreseeable future. With the possibility of an increase in claims, it may be time to think about some of the considerations home builders, contractors, and their insurers may want to contemplate when analyzing construction defect losses. As such, we detail a number of items that should be considered when estimating the total costs of construction defects.

Geography

A simple starting point in analyzing construction defect claims is to separate the data by state, or groups of states. Each state's legal environment can lead to differences in the reporting patterns of claims, frequency of claims that close with payment, and claim severity.

Each state has its own statute of limitations, stating the length of time a claim may be reported after substantial completion of construction. As such, it may be inappropriate to analyze losses in California, where the statute is 10 years, in the same grouping as losses in Washington state, where the statute is only six years. In analyzing claims from the two states together, one may overestimate the number of future claims in Washington state or underestimate the number of future claims in California as a result of the difference in statutes.

One should also consider the maturation of the legal environments among states. California, a state where the "construction defect industry began to take off in the 1980s due to the housing boom and the enforcement of strict liability claims by the courts,"2 has a very mature and stable legal environment for construction defect claims. The claim reporting pattern, percentage of claims that close with payment, and legal expenses may be more predictable in this kind of an environment. When the legal environment changes, as it did in Nevada with the passing of "Chapter 40" statutes, claim reporting may change drastically. Though the environment is now much more stable, Nevada initially saw a large influx of construction defect cases as a result of statute changes. In fact, a 2012 study determined that since 2006, the number of claims per new home in Nevada was 38 times the national average.3 While many had been dismissed as nuisance claims, they often still required legal expenses in order to obtain a dismissal. When there is a sound process for settling a construction defect claim, legal fees may be minimized, or at minimum more stable. In a changing environment, the legal fees may be more variable, or there may be a greater willingness to spend on legal fees in an attempt to set precedents.

Lastly, indemnity costs per claim may be affected by geography-- not only as a result of differences in housing preferences, building materials, or construction costs by region, but also potentially driven by the legal environment. Notice of Repair laws, such as California's SB 800, may reduce the number of nuisance claims and allow contractors to fix work prior to it becoming a bigger issue, thus keeping average indemnity costs down.

Type of insured: Subcontractor versus general contractor or developer

Construction defect losses will arise for both subcontractors performing work and general contractors or developers overseeing the work, so it may be best to analyze these two groups separately. General contractors and developers are likely to be brought into claims first, and may see larger severities as their claims may involve a large number of homes. Subcontractors may not know of claims immediately and may be brought in as an additional insured (discussed below), so the reporting pattern may be dependent upon how quickly general contractors or developers tender claims to the appropriate subcontractors. Further, some subcontractors may have low risk of claims or very low severities. For example, a carpet installer is likely to have much smaller losses than a framer or roofer. When analyzing construction defect losses for subcontractors, it may be beneficial to segregate the insureds even further into tiers of like risk classes.

Additional insured versus named insured

Of particular importance for subcontractors is the difference between named insured and additional insured claims. This is an area where data improvements have been seen in recent years when it comes to tracking information. While it was assumed for many years that additional insured and named insured claims behave differently, historically claims were not consistently set up with an indicator as to whether a claim is the result of additional insured tender or the result of a complaint directly from the plaintiff. While general contractors or developers will certainly have claims filed directly against them, subcontractors are likely to see a significant portion of their claims tendered as "additional insured" claims from the general contractor or developer for which they performed work. Additional insured claims may have noticeably different frequency, severity, and close with pay rates for a few reasons:

- Because not all additional insured endorsements provide general contractors and developers with sufficient coverage, many additional insured claims may get rejected quickly, thus the close with pay ratio may be materially lower than those of named insured claims.

- It is generally accepted that the duty to defend is greater than the duty to indemnify. While subcontractors may be able to close a claim without being responsible for any portion of indemnity, they may not be able to say the same about defense costs as their policies may require them to provide funds for the overall defense of a claim against the general contractor or developer.

- While an additional insured may have a duty to defend the named insured, they are unlikely to have the necessary influence to control the defense strategy or legal costs in large cases.

- The claims against a large developer may be substantially more complex than a claim directly against a subcontractor, adding to the legal fees needed to resolve the claim.

For these reasons, additional insight may be gained by analyzing additional insured claims separately from named insured claims.

Wrap and non-wrap policies

The typical insurance policy for a contractor is a straightforward policy, which covers only the contractor as a named insured. There are also wrap-up policies available that could cover every trade working on a particular project. The underlying reasons for utilizing wrap insurance are often strategic decisions by large developers. Including wrap and non-wrap policies together in an analysis could well lead to inaccurate results because the difference in policy structure is likely to lead to different underlying claims. For example, legal expenses may be higher in programs where each contractor has its own policy. The reason for this is the countersuits that may develop when one contractor blames another for the cause of the construction defect. Under a wrap policy, cross-suits like this are avoided as there is only one insurance policy in play. Wrap policies have also been used often for attached housing units, which can produce larger indemnity claims because they may affect more units than individual tract housing. Wrap policies may also span several years, particularly if a project is put on hold as many were during the global financial crisis of 2007-2010, whereas an individual policy is almost always one year in length.

Attached versus detached housing

As mentioned above, attached housing units may have higher severities because one defect is likely to affect many different units. Take, for example, the potential costs to fix the ongoing defect issues of the Millennium Tower residential high-rise in San Francisco, with more than 200 multimillion-dollar condos. Having sunk 17 inches and tilted 14 inches since its construction in 2008, cost estimates to correct the issue have been estimated in the range of $100 million to $150 million.4 Alternatively, defects in detached housing may very well affect only a single unit, particularly for custom builders or developers building only a handful of homes each year. These differences in claim severities may lead to distorted results if loss data cannot be separated between the two types of housing.

Additionally, with detached housing it may be helpful to consider the size of communities developed. A small general contractor building two or three homes at a time will likely see a frequency and severity that is different from a large homebuilder developing communities with hundreds of homes. Severity may be larger simply because claims for a large developer are likely to include more homes, whereas frequency may be different because building more homes creates more opportunity for a homeowner to notice a defect, and also because plaintiff attorneys may be more willing to focus on the larger communities for the sake of a larger reward. Likewise, a subcontractor working in a subdivision of 200 homes may see much larger claims than a subcontractor working for the developer's building a few homes at a time. While the cost per home may not differ, the cost per claim may well vary substantially if it is possible that a single claim could represent an issue over 20, 30, or 100 homes.

Community/home type

Many large home builders are creating brands or categorizing different types of homes they build: entry-level, move-up, luxury, and active adult (or age 55+ communities). Within the differing types of homes it is possible to see different trends. The move-up, luxury, and active adult homes may feature more expensive materials, and thus higher indemnity severity from the resultant property damage may result. Further, standards and resources for first-time buyers versus age 55+ may be different. First-time buyers or younger buyers may be more willing to make repairs themselves instead of filing claims against a builder. Active adult buyers may be more accustomed to higher standards of living or may be less willing to fix items themselves, so there may be a greater propensity to bring claims against a builder in this category. Additionally, many of the active adult communities feature not only homes but also community and activity centers. These additional exposures may draw claims from homeowner associations (HOAs). If the data is available, particularly for general contractors or large developers, it is a worthwhile exercise to dig into the reporting patterns, frequencies, and severities for each category of home.

Alternative fee arrangements

Construction defect is often considered a cottage industry, where plaintiff attorneys and defense firms can see increased payoffs in a typical hourly billing arrangement by allowing cases to drag on despite the possibility to settle early. In order to combat the issue of increasing legal expenses, insurers can put in place a variety of fixed fee arrangements with the defense firms they utilize. Arrangements range from a flat fee per claim or case handled to a flat fee to handle all of the claims reported for a given book of business. In these instances, using historical data to project the future legal expenses may be misguided. It's important to consider whether or not there are alternative fee arrangements in place that may affect not only the defense fees, but also the indemnity costs. If incentives aren't aligned such that the legal services provided under an alternative fee arrangement are as sufficient as they would have been under an hourly billing arrangement, it is possible that higher indemnity payments could result. However, there are ways to structure these arrangements that motivate attorneys to continue to pursue excellent indemnity results.

It may also be beneficial to take a look at your company's legal expenses and see if an alternative fee arrangement can create a cost savings in the future.

Frequency and severity by report lag

It has been hypothesized that claims reported longer after an accident period or substantial completion of construction have a greater likelihood to close without an indemnity payment, or, if they do have an indemnity payment, close with a smaller indemnity payment than claims reported within the first few years after the accident period. Claim severity may ramp up in the first three to five years after an accident period as homeowners begin to find major defects in their homes. In years seven to 10 after an accident period, the argument is that homeowners have likely discovered the major issues and the claims that begin to get reported are punch-list type items, or nuisance claims, either of which may be dismissed with little to no legal expense.

Evolving litigation

Keeping current with the evolving legal environment is important in long-tail business such as construction defect because the past may not always be an accurate representation of the future. Changes in the legal environment can affect both frequency and severity of claims and should be considered on a case-by-case basis.

Colorado passed House Bill 1279, effective as of September 1, 2017, aimed at making it more difficult for condo owners to bring suits against builders. The new bill creates a requirement that the majority of homeowners in the association consent to a lawsuit prior to an HOA filing suit. Similar legislation, House File 1538, was also passed this year in Minnesota. Thus, past frequency and severity may not be a great indicator of the future environment for attached housing in Colorado or Minnesota. If the legislation is effective, frequency of claims should see a drop, though severity may see an increase as smaller nuisance claims may not be reported.

In both Nevada and Iowa, legislation was passed that altered the statute of limitations. Senate File 413 in Iowa, which became effective September 1, 2017, shortened the state's statute of limitations from 15 years to 10 years. Nevada, which previously had a complex statute that could span up to 10 years, passed Assembly Bill 125 in 2015, which clarified that all construction defect actions must be reported within six years of substantial completion.

Report year versus accident year analysis

While report date is a straightforward concept for construction defect, accident date is more ambiguous but is typically understood to be the date of substantial completion of construction. Actuaries consider it standard practice to analyze construction defect losses by the year in which the claims are reported, but it may also be beneficial to take a look at defect losses on an accident year basis as well because there may be underlying accident year trends that are masked on a report year basis. For example, if a quality control measure was put in place, a reduction in frequency or severity on an accident year basis may be apparent that wouldn't be seen on a report year basis for an extended period. Also, law changes, such as the change in the statute of limitations in Nevada, may be shown in the data on an accident year basis, but may not be as apparent in a report year analysis. These accident year trends may warrant an adjustment to the typical report year analysis that actuaries tend to use.

Use of predictive analytics

The considerations discussed above may lend themselves well to an exercise in predictive analytics. Insurers may use predictive analytics to determine which contractors are most profitable to write or which segmentation of claims is ideal for reserving. Home builders can use analytics to determine the likelihood of claims from employing certain trades or may be able to more accurately allocate the costs of insurance to business units depending on the location of homes, or the types of homes being built, in order to maximize margins going forward.

Conclusion

Construction defect losses shouldn't be analyzed with a one-size-fits-all mentality. The discussion points above are not meant to serve as an exhaustive list, but are intended to provide users with some initial ideas of the different factors that can be considered when analyzing exposure to construction defects. Assuming that growth in home building over the past few years does equate to a rise in construction defect claims down the road, identifying and analyzing various characteristics and changing trends will prepare developers, contractors, and insurers for what may lie ahead.

1U.S. Census Bureau (August 2017). New Residential Sales. Retrieved October 17, 2017, from https://www.census.gov/construction/nrs/index.html.

2Lockhart Park. Discussion of History of Construction Defect Litigation in California. Retrieved October 17, 2017, from https://www.lockhartpark.com/discussion-of-history-of-construction-defect-litigation-in-calif.html.

3Brown, Stephen P. A., & Kennelly, Ryan (February 2013). The Nevada Housing Market: Prospects for Recovery. Retrieved October 17, 2017, from https://www.ralstonreports.com/sites/default/files/UNLV-SNHBA-Report%5B1%5D.pdf.

4Robinson, M. (September 22, 2017). A fix for San Francisco's sinking skyscraper could cost upward of $100 million and no one wants to foot the bill. Business Insider. Retrieved October 17, 2017, from http://www.businessinsider.com/cost-to-fix-leaning-millennium-tower-2017-9.