Retirees are demanding simple products that offer guaranteed income, flexibility, and low fees, according to a Milliman survey of financial institutions across eight Asia-Pacific countries.

Those expectations are creating significant challenges for organisations given many in-demand risk management features, such as capital guarantees, typically come with higher fees or less liquidity.

Firms will need to understand the underlying drivers of retiree needs and more effectively communicate the necessary product feature trade-offs if they are to deliver better retirement outcomes.

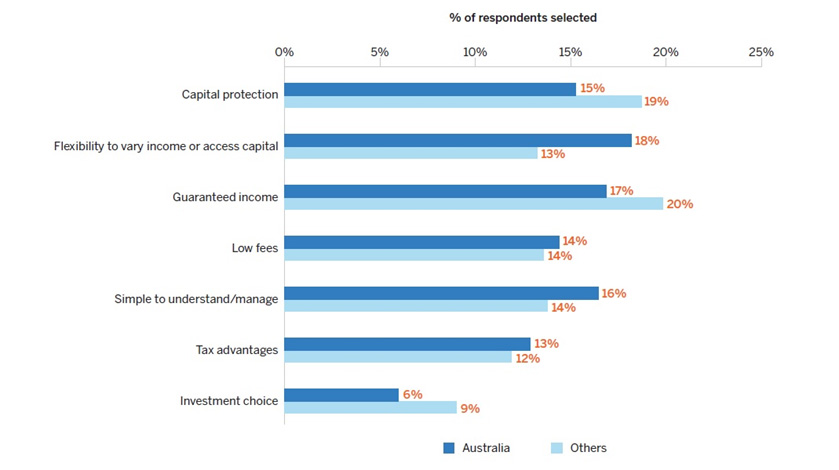

Figure 1: What are the most important features in a retirement income product for the consumer?

The survey, which included more than 100 insurance companies and financial institutions across Asia-Pacific, reveals how firms are responding by creating more tailored regional products.

It marks a change from past approaches that typically led to either:

- Low-fee, flexible products that left investors exposed to 100% market risk.

- High-cost, inflexible products that guaranteed income or capital.

However, firms are now starting to offer a range of products with greater investment certainty but without costly and inflexible full-blown guarantees.

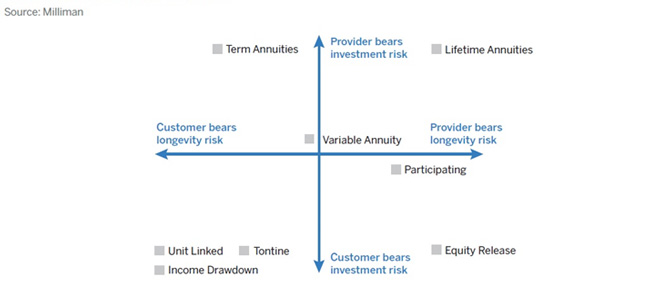

Figure 2: Risk mapping by product

Guaranteed products such as annuities remain popular among institutions across Asia-Pacific according to the survey but adoption by consumers has been limited other than in Singapore (through the government-provided CPF LIFE pension) and Australia, where the annuity market is slowly reviving and the government is reviewing structural impediments.

Historic low interest rates, which are keeping payouts low, stand as another roadblock for annuities and other longevity-focused products, according to the survey.

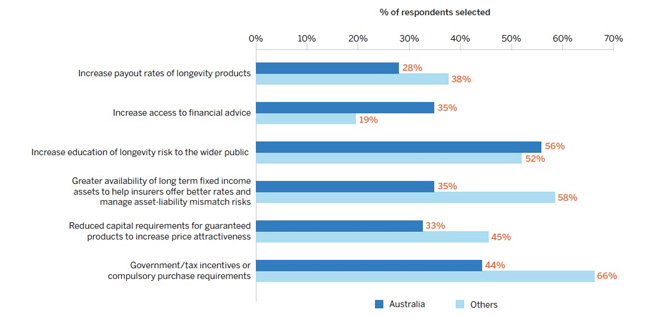

Figure 3: What needs to be done to increase the uptake of longevity products?

But while providers and governments can make longevity-focused products more attractive, there is scope to improve the education of financial planners and consumers about how to implement smarter longevity solutions.

These challenges are consistent across Asia-Pacific because they are fundamentally manifestations of human behaviour.

Longevity solutions tend to struggle to gain traction without a strong incentive model or government support because of factors such as hyperbolic discounting: People are hard-wired to focus on the short-term and struggle to assess the value of distant payouts in the future.

Short-term loss aversion is another behavioural bias that particularly affects retirees—the pain from losing money is far more acute than the pleasure from making money. This has helped underpin the success of products with an element of capital protection or managed market risk compared to long-term annuities and income products.

However, firms are taking on these challenges and beginning to use new technology and approaches to innovate. Large insurance companies, for example, are adopting an agile approach to product testing, building experience rather than attempting to create a perfect product.

The regulatory challenge remains significant with regular changes leading to confusion and a general lack of faith in the stability of the system, according to surveyed companies.

Few countries across Asia-Pacific meet the common financial planning goal of providing 60% to 70% of pre-retirement income in retirement, as the region grapples with rapidly ageing populations. Meanwhile, about half of firms in the Milliman Asia retirement income report said their national retirement income systems currently worked for less than one-third of the population.

However, while this is cause for concern, it also represents an opportunity for private organisations to step in and fill part of the gap.

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

These results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown. Milliman does not manage the underlying fund.

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.