The superannuation industry has placed an extraordinary emphasis on helping members achieve a “comfortable” retirement given it has so little information about what it actually means.

What we do know is largely composed of averages and assumptions which are ranked against the ASFA Retirement Standard’s portrait of the average Australian.

The standard represented an important step forward when it was launched in 2004, but expectations have since risen dramatically along with the industry’s assets, which now surpass Australia’s annual gross domestic product and the size of the share market.

The personalised nature of each superannuation member’s retirement journey means a one-size-fits-all approach simply cannot deliver the necessary information, products and risk management strategies required to achieve everyone’s desired outcomes.

Or, as the Productivity Commission’s recent report into the industry’s competitiveness and efficiency put it, “Indicators which focus on the ‘median’ or the ‘average’ user will not necessarily reflect what is optimal for all or even most members”.

Funds need to take a more nuanced approach or a lack of member engagement will be the end result.

Starting points: Different funds, different members

An average couple requires about $640,000 at retirement (or $545,000 for a single person) to support a comfortable retirement, according to the ASFA Retirement Standard.

The average Australian household at retirement has slightly more than half this level of super—around $355,000 in 2013-14, according to ASFA. However, this hides a wide disparity in actual retirement experiences. The median household super balance was just $110,000.

At the least, this suggests that the ASFA Retirement Standard is of little practical relevance to a significant number of older Australians and those super funds attempting to improve their retirement experience.

A basic analysis of super fund data, segmented by age, underlines the problem faced by funds.

For example, APRA data reveals that Hostplus members aged 45-64 years had an average balance of approximately $40,000 (the bulk of its approximate 1 million are much younger) at June 30, 2015. No amount of investment outperformance is going to lift these members into the comfortable category defined by the ASFA Retirement Standard.

APRA data also reveals that a number of funds had relatively well-off members (although the data can be partially skewed with defined benefit categories) aged 45-64 years such as equip ($247,000), Commonwealth Bank Group Super ($215,000) and Energy Super ($200,000). Many of their members will have higher expectations about retirement than the standard assumes.

These differences between funds require different strategies to support a comfortable retirement, which should be defined by members rather than be dictated to them.

Assuming less and learning more

The only way to deliver products and services which will deliver better retirement outcomes is to learn more about members.

This is no easy task given there are more than 13 million Australians with (often multiple) super accounts and each has their own individual preferences and circumstances. But it is a crucial first step.

Too many funds assume super is the central hub of retirement–as expressed through the ASFA Retirement Standard–when they have little or no information about members’ wealth outside of super or their personal expectations.

Too many members who can’t meet this standard then receive a devastating message: they’ve paid for a product for decades over a working lifetime only to be told they haven’t earned a comfortable retirement (as defined by the fund rather than the member).

This is a cue for disengagement. Funds with a large proportion of members who can’t meet the current standard should instead take this as a prompt to learn more about them.

It requires better communication with members about their actual needs and better segmentation based on a far wider range of real-world data.

This combination can produce far more accurate estimates of what a comfortable retirement means for individuals and then suggest a pathway to support it.

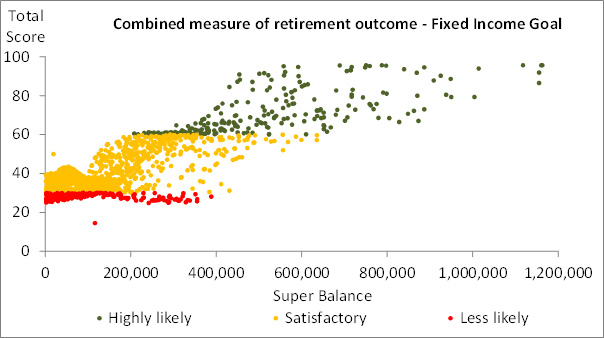

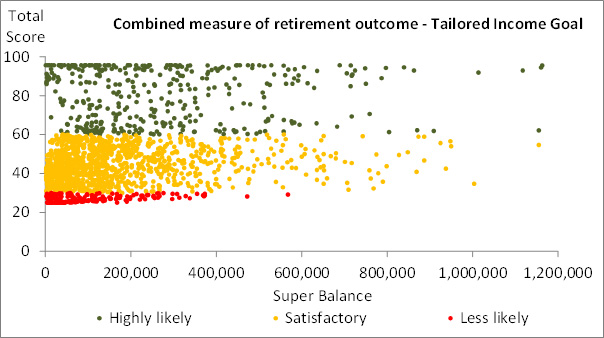

For example, an analysis that includes just one new real-world data set (the ABS Household Expenditure Survey) can radically reshape the type of fixed income goals expressed in the current retirement standards. This is illustrated below where the income goal is defined at a member level incorporating a more realistic expectation of spending requirements using ABS HES data.

Source: Milliman analysis, ABS Household Expenditure Survey, ASFA Retirement Standards.

The opportunity to create better benchmarks is now there for funds thanks to more open data and the rise of low-cost cloud computing that has enabled analysis on a deeper level than ever before.

The super industry exists because Australians are forced to support its products for decades. Finding out what they really need for a comfortable retirement, and helping them achieve it, is the least they deserve in return.

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.