Australia’s newly revamped consumer price index (CPI) may provide a more accurate picture of what the average household spends its money on, but it’s no closer to solving the problems faced by retirees.

The Australian Bureau of Statistics (ABS), which recently reweighted the CPI’s basket of goods for the first time in more than six years, suggests inflation has been even weaker than previously thought.

However, that basket of goods still differs radically from the average retiree, whose cost of living steeply declines though retirement, according to the Milliman Retirement and Expectations Spending Profiles (ESP) service.

The revised ABS measure of CPI suggests that the average household’s expenses have been rising slower than expected.

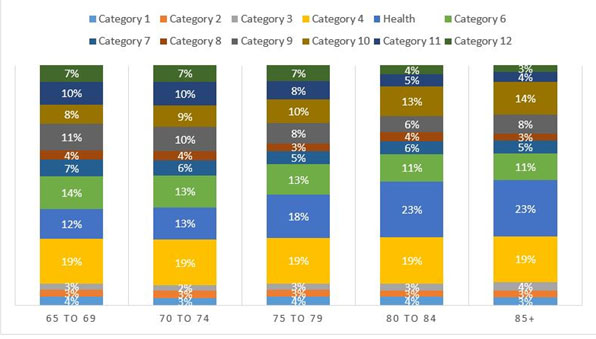

While RBA then lowered its outlook for underlying inflation (which remains below its target of 2% to 3%) in its November 2017 Statement on Monetary Policy, the Milliman Retirement ESP tells us that retirees’ actual expenditure falls by about 8% between ages 65-69 and 70-74.

This is a major disconnect given more than half of balanced pension funds (59%) rank their performance against CPI, according to researcher SuperRatings.

How retirees’ basket of goods differs from CPI

The new CPI weightings show rising rental costs driving up the average household expenditure on housing, which rose from 13.2% to 14.8%. The ABS also estimated housing expenditure for self-funded retiree households (12.1%) and pensioner and beneficiary households (23.4%).

However, the vast majority of retirees own their own home and, according to real-world expenditure data captured by the Milliman Retirement ESP, spend just 7% of expenditure on housing. This is likely to rise as the east coast affordability crisis is already driving down home ownership levels, which will increasingly affect older Australians over time.

The revised CPI weightings also show health costs rising from 5.2% to 5.4%.

Real-world expenditure data captured through the Milliman Retirement ESP shows it much higher–about 12% of total expenditure for retirees aged 65-69. It also increases dramatically as retirees age even as their total expenditure inclusive of all categories falls.

This is still significantly higher expenditure on health than the ABS estimates for pensioner and beneficiary households (6.8%) and self-funded retiree households (10.3%, with more spent on dental and elective hospital procedures).

The new CPI weightings also show the largest increases (in dollar terms) in areas where retirees spent little: child care (127% increase), international holiday travel and accommodation (60% increase) and education (56% increase).

Figure 1: Composition of spending - couple

Source: Milliman Retirement Expectations and Spending Profiles Q2 2017. See full report for a full breakdown and labels of each spending component.

The benefits of real-world data compared to surveys

The ABS’s core CPI measure is a conglomerate of many different households and cannot reflect the specific behaviour of retirees. Its accuracy (and that of its self-funded retiree and pensioner and beneficiary households) is also limited by methodology.

The CPI item weightings are largely derived from the ABS’ Household Expenditure Survey (HES), which is conducted every five or six years (the 2017 CPI adjustment was based on surveys conducted in 2015-16).

This introduces a significant time lag. Surveys are also notorious for producing errors given the inability of people to accurately remember where they spend their money. The CPI measure also makes no allowance for the way households regularly adjust their spending depending on changes in preferences, income and relative prices.

The Milliman Retirement ESP differs significantly. It is based on the bank transaction data of more than 300,000 retirees and cross-referenced against other data sets such as property (CoreLogic) and retail spending (Woolworths).

There is no room for misremembering–it reveals retirees’ actual real expenditure each quarter. The quarterly data is current, which also reveals early expenditure and lifestyle trends that retirees themselves may not be aware of.

As the prudential regulator pressures super funds to justify their decisions made on behalf of members, it will become crucial to use big data such as the Milliman ESP to truly understand members.

It can help lead product development, refine advice and boost engagement by enriching our understanding of how retirees actually live.

The full Milliman Retirement ESP report is published to subscribers each quarter. Contact Milliman senior consultant Jeff Gebler at [email protected] for more details.

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.