(Yes, but not as much as you might think)

Introduction

The individual mandate’s financial penalties are probably sufficient to induce high insurance participation rates. However, enforcement of the penalties has not been strict enough to achieve the mandate’s full policy aims.

The individual mandate has been called one leg of the Patient Protection and Affordable Care Act (ACA) “three-legged stool” (with guaranteed issue and subsidies being the other two legs).1 During the crafting of healthcare reform, culminating in the passage of the ACA in 2010, insurers and other market experts contended that the mandate was absolutely necessary for a functional individual guaranteed issue market. With the passage of the Tax Cuts and Jobs Act of 2017, which included a repeal of the individual mandate, there are renewed concerns related to the stability of the individual market. (Technically, the mandate was not repealed, but rather the penalty was set to $0 for 2019 and future years. Throughout this paper, we will refer to this action as repeal.)

While we believe the individual mandate’s financial penalties at face value are high enough to induce high insurance participation rates, the enforcement of these penalties has not been strict enough to fully achieve the mandate’s policy aims. However, available premium assistance in the insurance marketplaces may provide sufficient financial incentives to prevent a collapse of marketplace enrollment rates resulting from the mandate’s repeal. In this paper, we examine available empirical data to arrive at this conclusion.

Additionally, available premium assistance may provide sufficient financial incentives for marketplace enrollment to remain high enough to not result in a significant deterioration of the risk pool in the absence of the mandate.

Uncertainty associated with the mandate’s repeal

The Congressional Budget Office (CBO) believes the mandate repeal will have a material impact on enrollment and premium rates in the non-group market.2,3 Specifically, the CBO estimates that, as a result of the mandate’s repeal:

- Enrollment in the non-group health insurance market, including the marketplace, will decrease by 3 million in 2019 (17 million baseline) and by 5 million in 2025 (18 million baseline).4,5

- Non-group premium rates in the next 10 years will be as much as 10% higher than if the mandate continued.6

More CBO projections

The mandate is most often associated with the ACA and its guaranteed issue provisions and rating reforms. However, the CBO also estimates 5 million fewer people under age 65 will elect to enroll in Medicaid coverage in 2026 (from a baseline of 70 million). The CBO cites four factors that may have resulted in higher Medicaid enrollment under the mandate:

1. A portion of the Medicaid population is subject to the mandate (those filing taxes).

2. Individuals who are exempt from the mandate may believe they are not exempt and enroll in coverage.

3. Some people who have applied for coverage in the marketplaces because of the mandate have turned out to be Medicaid-eligible.

4. Some people will enroll due to peer pressure from others who have enrolled because of the mandate.

On the other hand, while the CBO’s report has provided point estimates for the impact on non-group enrollment and premium rates from repealing the individual mandate, the CBO also devotes several paragraphs to discussing why the actual effects may differ from the above values. In other words, there is considerable uncertainty when it comes to the actual impacts of the mandate repeal. This uncertainty is driven by several factors. First, and maybe the most significant, is the fact that the impact of a mandate (and by extension, its repeal) fundamentally deals with human behavior, which is notoriously hard to predict. Second, even if human behavior were well-understood, the impact would vary considerably state by state based on various factors, including overall premium rates and affordability, state median income, and a state’s Medicaid eligibility levels (particularly its decision on Medicaid expansion). And finally, as we shall see in the following sections, the evidence for mandate effectiveness is mixed.

State market reforms prior to the ACA

Prior to the ACA, non-group insurance rating rules varied significantly across the country.7 The vast majority of states permitted medical underwriting, while a small number required a form of community rating (which prevents insurers from varying premiums by health status). In the 1990s, several states attempted to reform their non-group markets by adopting guaranteed issue (GI) and community rating (CR) rules without a coverage mandate. Research done by Milliman actuaries found that the states implementing GI and CR without a mandate experienced market deterioration as measured by enrollment, premium rates, and available insurance options.8

However, these historical examples admittedly are not the ideal comparisons for how the ACA individual market might function without a mandate. While the states implementing these reforms in the 1990s did not have individual mandates, they also did not have various other measures intended to decrease unfavorable selection and increase enrollment, which the ACA does have. These measures include open enrollment periods and financial assistance to consumers to purchase coverage in the form of premium subsidies.9 The ACA premium subsidies in particular are thought to be a critical part of market stability, even though they do not apply to everyone buying coverage in the individual market.10

Shared responsibility payments, mandate exemptions, and insurance coverage changes from 2014 to 2016

The most recent data available11 related to the mandate indicates health insurance coverage rates might respond to an effective mandate. For example, from 2014 to 2015, the mandate was strengthened from the greater of 1% of income or $95 to the greater of 2% of income or $325 (and strengthened further to 2.5% of income or $695 in 2016).12 Examining the Internal Revenue Service (IRS) data for these two periods provides the following observations regarding shared responsibility payments and mandate exemptions:

- In 2015, 6.5 million taxpayers reported $3 billion in individual responsibility payments, which is 1.5 million fewer taxpayers making payments relative to 2014.13

- However, 12.7 million taxpayers claimed an exemption from the individual mandate in 2015,14 an increase of approximately 300,000 from reported values for the 2014 coverage year.15

- Combining these changes suggests a net increase in insured individuals of 1.2 million from 2014 to 2015 (1.5 million fewer individual responsibility payments, less 300,000 additional mandate exemptions). Insurer financial data from 2014 and 2015 is consistent with this observation, with national non-group market average monthly enrollment increasing from 15.0 million to 17.5 million.16

Available statistics on shared responsibility payments and insurance coverage from 2014 to 2015 might suggest a positive correlation between enhanced penalties and insurance coverage gains. However, in complex environments such as health insurance markets, many other factors could be influencing overall insurance coverage rates in addition to the strength of the mandate (e.g., greater awareness of the mandate, consumer education, changes in access to employer-sponsored insurance and public coverage, and premium rates). To that end, the mandate penalty went up again in 2016, but reported enrollment for the national comprehensive individual market in 2016 was flat to slightly down relative to 2015.17 Similarly, based on the National Health Interview Survey (NHIS), the uninsured rate for persons under age 65 was nearly identical from 2015 (10.5%) to 2016 (10.4%).18

Mandate enforcement and exemptions

A mandate to buy health insurance coverage is only effective if the penalty is actually applied in practice to nearly all individuals who do not purchase health insurance. While the ACA’s individual mandate was in place in 2014 and 2015 and carried an increasing penalty, there were a number of limitations related to the penalty being collected by the IRS.

First, the only way the IRS could enforce and collect the penalty was to reduce the amount of a taxpayer’s refund.19,20 Thus if a taxpayer owed an individual responsibility payment but was not in a refund situation, the penalty could be avoided, at least until the next year in which a tax refund was owed.21 This is the case for all tax years from 2014 to 2018.

As discussed previously, the number of individuals receiving an individual mandate exemption was nearly twice the number of persons making a shared responsibility payment in 2015 (6.5 million vs. 12.7 million). Taxpayers could apply for an individual mandate exemption due to a hardship, unaffordable coverage, or several other exemption categories.22 For this paper, we will focus on hardship and affordability exemptions, as well as “silent returns.”

- Hardship exemptions. To qualify for a hardship exemption, a person could select one of more than 10 categories or describe an unlisted hardship.23 One notable example of a hardship category that is broad and subjective is for individuals who had grandfathered health insurance coverage that was canceled and who do not believe marketplace plans are affordable.

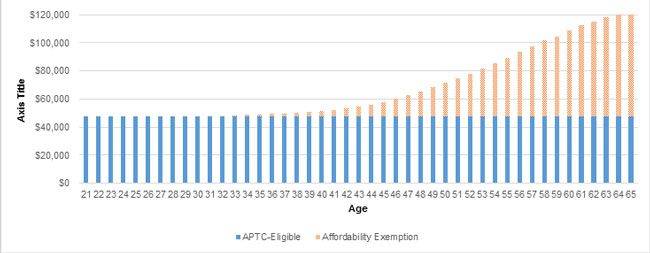

- Affordability exemptions. The individual mandate provision allows for exemptions in cases where households cannot purchase affordable coverage.24 For 2017, affordability is measured by whether self-only minimum essential coverage exceeds 8.16% of household income.25 Affordability is measured using the lowest-cost bronze plan offered in the taxpayer’s geographic area.26 For insurers operating in states where significant premium increases have occurred from 2015 to 2017, it is likely that a greater number of individuals with household incomes above 400% of the federal poverty level (FPL)—that is, not eligible for federal premium assistance—will qualify for the affordability exemption relative to prior years. Because premiums increase with age and the available premium subsidies are capped at a fixed percentage of income, the affordability exemption is most likely to impact older adults. Using the monthly national average bronze premium for a 21-year-old of $272 in 2017,27 the chart in Figure 1 illustrates the income level at which a single person would qualify for an affordability exemption in 2017, as well as Advance Premium Tax Credit (APTC) eligibility up to 400% FPL.

Figure 1: 2017 APTC Eligibility and Affordability Exemptions: Single Household, Based on National Average Bronze Premium

Based on public data for the 2017 open enrollment period plan selections,28 nearly 65% of insurance marketplace enrollees nationwide are above the age of 35, the age range at which at least some portion of adults could get an affordability exemption. While the numbers in Figure 1 are based on a national average premium, it is likely in many geographic areas that a significant portion of adults over age 50 qualified for an affordability exemption in 2017, and, with large rate increases once again, even more in 2018. For example, an adult age 55 with income between approximately $48,000 and $89,000 would qualify for an affordability exemption in 2017 based on the monthly national average bronze premium. As stated previously, the actual affordability exemption is based on the lowest-cost bronze plan offered in the taxpayer’s geographic area.

- Silent returns. Based on 2015 tax filing returns, 4.3 million nondependent taxpayers submitted returns without reporting having health insurance coverage, claiming an individual mandate exemption, or making a shared responsibility payment.29 This situation, known as a “silent return,” will not be permitted by the IRS for 2017 tax returns.30

Perspective

The sum of individual mandate exemptions (12.7 million) and silent returns (4.3 million) for the 2015 tax filing year (totaling 17.0 million) was nearly equal to the average monthly enrollment in the non-group market in 2015 (17.5 million)

For perspective, the sum of individual mandate exemptions (12.7 million) and silent returns (4.3 million) for the 2015 tax filing year (17.0 million) was nearly equal to the average monthly enrollment in the non-group market in 2015 (17.5 million).31,32 While it is possible that a portion of the population receiving exemptions or filing silent returns is eligible for other forms of insurance (such as employer-sponsored coverage), the absence of these individuals from the individual market risk pool is likely a contributing factor to significant premium rate increases that have been observed in many parts of the country in the last few years.33

Employer coverage changes and incentives associated with purchasing health insurance

While measuring the effect of the individual mandate has focused on the non-group insurance market, isolating its impact is difficult because the institution of the individual mandate coincided with the implementation of the insurance marketplaces and available federal premium assistance. Comparatively, the employer-sponsored insurance market has been stable relative to the non-group market in terms of enrollment, types of coverage offered, and premium subsidy provided (through an employer’s contribution to the sponsored plan). Therefore, by examining insurance participation in employer coverage (the percentage of employees eligible for an employer’s sponsored health plan who elect to purchase coverage) in the current decade, we can assess whether the individual mandate may have had a material effect on insurance participation rates.

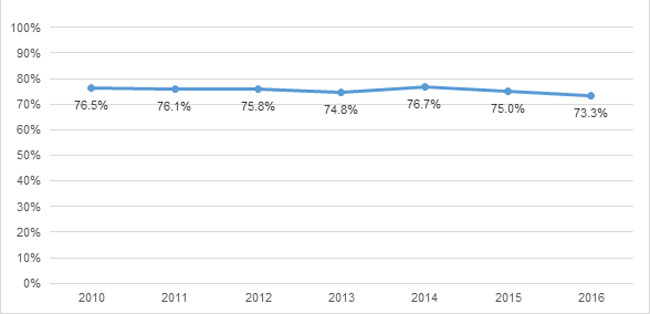

Based on the Medical Expenditure Panel Survey (MEPS) administered by the Agency for Healthcare Research and Quality (AHRQ), the chart in Figure 2 illustrates the percentage of eligible private sector employees enrolling in employer-sponsored insurance from 2010 through 2016.34 Nonparticipation in an employer’s plan may be due to a number of factors, including: availability of coverage through a spouse’s employer, eligibility for public health insurance (Medicaid), unaffordability of coverage, or perceived lack of need for health insurance. Therefore, the participation rate in an employer’s plan should not be used to estimate the percentage of employees that are uninsured.

Figure 2: Percentage of Eligible Employees Enrolling in Employer-Sponsored Insurance (private sector employees)

No change in take-up rates for industries with historically lower-than-average participation rates

Reviewing health insurance participation rates for the retail trade industry, which varied between 62% and 64% in the three years prior to 2014, there is no observed meaningful change in health insurance take-up rates through 2016.

In 2010, 76.5% of eligible employees enrolled in their employers’ health plan coverage. Ignoring random volatility in the survey results, these data points do not suggest any material change in employer-sponsored insurance participation since the implementation of the individual mandate in 2014. This suggests two primary observations:

1. Incentives explicitly offered through employer-sponsored insurance (employer subsidy, tax-exempt treatment of the value of coverage, employee contributions made on a pretax basis) are sufficient to induce high insurance participation.

2. The implementation of the individual mandate in 2014 did not result in incremental gains in employer-sponsored insurance participation above those achieved by explicit incentives such as favorable tax treatment and employer subsidies for health insurance coverage.35

Conclusion

In summary, assessing the impact of the mandate’s repeal on the individual market must be considered within the context of an individual’s current health insurance coverage situation.

The effect of the mandate’s repeal on individuals opting out of health insurance coverage

As the mandate penalty has gone up and net premiums (after premium subsidies) in many cases have gone down, it makes increasing financial sense to enroll in coverage if eligible.36 However, enforcement of the mandate, due to both legislative and regulatory decisions, has not been sufficiently strong to induce high insurance participation rates in the non-group market, lessening the potential for the mandate’s repeal to have a dramatic effect.

- Many potential enrollees could be paying zero for bronze coverage rather than paying a penalty for no coverage.37 An analysis performed by the Kaiser Family Foundation (KFF) estimated 5.8 million subsidy-eligible individuals could purchase a bronze plan for less than the individual mandate penalty.38

- To the extent consumers recognized this and could have been induced to make financially rational decisions, fewer mandate exemptions and stricter enforcement may have resulted in a material percentage of persons currently not enrolled in the individual market opting to purchase coverage in 2018 and future years.

The effect of the mandate’s repeal on individuals currently purchasing health insurance

If federal premium assistance offered through the insurance marketplaces is viewed as a sufficient incentive to purchase insurance by itself, enrollment rates for the premium subsidy-eligible population may not materially change in the absence of the individual mandate.

- It is possible that even during the 2018 open enrollment period (OEP) of November 1 through December 15, 2017, there was a perception among some consumers that the individual mandate would be repealed or not enforced by the Trump administration.39

- However, December 2017 reported national marketplace selections were 11.8 million for the 2018 OEP,40 which was only slightly down from 2017 figures, 12.2 million.41

- Due to the paradoxical effect of marketplace premium rate increases causing lower out-of-pocket premiums for the subsidy-eligible population, the absence of the mandate may have a more limited effect on insurance marketplace enrollment as more generous subsidies lead to low-cost or no-cost plans being the larger motivation to purchase coverage.

The effect of the mandate’s repeal must also be considered for the population purchasing individual market coverage without a subsidy. For this market segment, premium affordability will likely continue to be a significant concern. Because of the individual mandate’s affordability provision, the mandate’s ability to slow enrollment attrition for nonsubsidized consumers may have been limited in many states. Therefore, future premium rate changes may have a larger impact on health insurance participation than the mandate’s repeal.

How to achieve market stability?

In conclusion, while we believe an insurance mandate can be an effective tool in inducing high insurance participation rates, it must be sufficiently enforced to fully achieve its policy aims. Thoughtfully structured and consistently enforced state-based insurance mandates, in combination with existing ACA federal premium assistance and other stability programs (such as state-based reinsurance programs),42 may provide policymakers the best opportunities to improve the individual market risk pool.

1Gruber, J. (August 5, 2010). Health care reform is a "three-legged stool." Center for American Progress. Retrieved February 7, 2018, from https://www.americanprogress.org/issues/healthcare/reports/2010/08/05/8226/health-care-reform-is-a-three-legged-stool/.

2CBO (January 20, 2018). Estimating the Costs of Proposals Affecting Health Insurance Coverage. Retrieved February 7, 2018, from https://www.cbo.gov/system/files/115th-congress-2017-2018/presentation/53448-presentation.pdf.

3Centers for Medicare and Medicaid Services (CMS) actuaries subsequently issued a report with smaller enrollment impact, available at https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2017.1655.

4CBO (November 2017). Repealing the Individual Health Insurance Mandate: An Updated Estimate, Table 2. Retrieved February 7, 2018, from https://www.cbo.gov/system/files/115th-congress-2017-2018/reports/53300-individualmandate.pdf.

5CBO (September 2017). Federal Subsidies for Health Insurance Coverage for People Under Age 65: 2017 to 2027, Table 1. Retrieved February 7, 2018, from https://www.cbo.gov/system/files/115th-congress-2017-2018/reports/53091-fshic.pdf.

6CBO, November 2017, Repealing, ibid., p. 1.

7See /-/media/Milliman/importedfiles/uploadedFiles/insight/health-published/health-insurance-market-10-31-11.ashx, page 7, for more information.

8Wachenheim, L. & Leida, H. (March 2012). The Impact of Guaranteed Issue and Community Rating Reforms on States' Individual Insurance Markets, p. 2. America's Health Insurance Plans. Retrieved February 7, 2018, from http://www.statecoverage.org/files/Updated-Milliman-Report_GI_and_Comm_Rating_March_2012.pdf.

9Massachusetts’ healthcare reform in the 1990s had an open enrollment period.

10Eibner, C. & Salzman, E. (2014). Premiums and Stability in the Individual Health Insurance Market. RAND Corporation. Retrieved February 7, 2018, from https://www.rand.org/pubs/research_briefs/RB9798.html.

11Detailed IRS data on mandate is not available for 2016 at the time of writing this article.

12Houchens, P.R. (March 2012). Measuring the Strength of the Individual Mandate, p. 6. Milliman Research Report. Retrieved February 7, 2018, from /-/media/Milliman/importedfiles/uploadedFiles/insight/health-published/measuring-strength-individual-mandate.ashx.

13IRS Commissioner John Koskinen (January 9, 2017). Letter to members of Congress regarding 2016 tax filings related to Affordable Care Act provisions. Retrieved February 7, 2018, from https://www.irs.gov/pub/newsroom/commissionerletteracafilingseason.pdf.

14IRS letter to Congress regarding 2016, ibid.

15IRS Commissioner John Koskinen (January 8, 2016). Letter to members of Congress on preliminary results from the 2015 filing season related to Affordable Care Act provisions as of October 2015. Retrieved February 7, 2018, from https://www.irs.gov/pub/newsroom/irs_letter_aca_stats_010816.pdf.

16See /-/media/Milliman/importedfiles/uploadedFiles/insight/2017/2015-commercial-health-insurance.ashx, Figure 6. A portion of the individual market increase may have been driven by other factors, such as the decline in small group coverage.

17Based on preliminary assessment of commercial medical loss ratio filings submitted to CMS.

18National Center for Health Statistics (May 2017). Health Insurance Coverage: Early Release of Estimates From the National Health Interview Survey, 2016, Table 1. Retrieved February 7, 2018, from https://www.cdc.gov/nchs/data/nhis/earlyrelease/insur201705.pdf.

19IRS (December 5, 2017). Questions and Answers on the Individual Shared Responsibility Provision. Retrieved February 7, 2018, from https://www.irs.gov/affordable-care-act/individuals-and-families/questions-and-answers-on-the-individual-shared-responsibility-provision.

20Internal Revenue Code. Chapter 48—Maintenance of Minimum Essential Coverage. Retrieved February 7, 2018, from https://www.gpo.gov/fdsys/pkg/USCODE-2011-title26/pdf/USCODE-2011-title26-subtitleD-chap48-sec5000A.pdf.

21Nor could the IRS apply a lien on the taxpayer for the penalty and pursue any charges, criminal or civil.

22Healthcare.gov. Health Coverage Exemptions, Forms, and How to Apply. Retrieved February 7, 2018, from https://www.healthcare.gov/health-coverage-exemptions/forms-how-to-apply/.

23Healthcare.gov. Hardship Exemptions, Forms, and How to Apply. Retrieved February 7, 2018, from https://www.healthcare.gov/health-coverage-exemptions/hardship-exemptions/.

24Houchens, ibid. See page 6 for additional discussion.

25Federal Register (March 8, 2016). HHS Notice of Benefit and Payment Parameters for 2017, p. 12282. Retrieved February 7, 2018, from https://www.gpo.gov/fdsys/pkg/FR-2016-03-08/pdf/2016-04439.pdf. Note that the affordability measure is 8.05% for 2018.

26Healthcare.gov. How to Claim an Exemption Because Marketplace Coverage Is Considered Unaffordable Based on Your Projected Annual Household Income. Retrieved February 7, 2018, from https://www.healthcare.gov/exemptions-tool/#/results/2017/details/marketplace-affordability.

27As published in https://www.irs.gov/pub/irs-drop/rp-17-48.pdf, according to a methodology published in https://www.irs.gov/pub/irs-drop/rp-14-46.pdf, which specifies that this value is for an age 21 non-tobacco user.

28IRS. 26 CFR 601.105: Examination of Returns and Claims for Refund, Credit, or Abatement; Determination of Correct Tax Liability. Retrieved February 7, 2018, from https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Marketplace-Products/Plan_Selection_ZIP.html.

29IRS letter to Congress regarding 2016, ibid.

30IRS (November 21, 2017). Individual Shared Responsibility Provision. Retrieved February 7, 2018, from https://www.irs.gov/affordable-care-act/individuals-and-families/individual-shared-responsibility-provision.

31Houchens, P. et al. (March 2017). 2015 Commercial Health Insurance, Table 6. Milliman Research Report. Retrieved February 7, 2018, from /-/media/Milliman/importedfiles/uploadedFiles/insight/2017/2015-commercial-health-insurance.ashx.

32While silent returns are prohibited for the 2017 tax filing year, marketplace enrollment changes from 2016 to 2017 do not suggest this had a measureable effect on enrollment.

33Other major factors include healthcare inflation, the phase-out of the transitional reinsurance program, and the elimination of cost-sharing reduction payments. See http://www.milliman.com/insight/2015/Ten-potential-drivers-of-ACA-premium-rates-in-2017/ for additional discussion on drivers of ACA premium rates.

34AHRQ. MEPS: MEPSnet Query Tools. Retrieved February 23, 2018, from https://meps.ahrq.gov/mepsweb/data_stats/meps_query.jsp.

35Please see https://www.cbo.gov/budget-options/2013/44903 for further discussion.

36See /-/media/Milliman/importedfiles/uploadedFiles/insight/health-published/measuring-strength-individual-mandate.ashx for an in-depth discussion of this topic.

37Semanskee, A., Claxton, G., & Levitt, L. (November 29, 2017). How Premiums Are Changing in 2018. Kaiser Family Foundation. Retrieved February 7, 2018, from https://www.kff.org/health-reform/issue-brief/how-premiums-are-changing-in-2018/.

38KFF (November 2017). How many of the uninsured can purchase a marketplace plan for less than their shared responsibility penalty? Issue Brief. Retrieved February 23, 2018, from http://files.kff.org/attachment/Issue-Brief-How-Many-of-the-Uninsured-can-Purchase-a-Marketplace-Plan-for-Less-Than-Their-Shared-Responsibility-Penalty.

39KFF (October 18, 2017). Kaiser Health Tracking Poll – October 2017: Expeiences of the Non-Group Marketplace Enrollees, Figure 9. Retrieved February 23, 2018, from https://www.kff.org/health-reform/poll-finding/kaiser-health-tracking-poll-october-2017-experiences-of-the-non-group-marketplace-enrollees/.

40CMS.gov (December 28, 2017). Final Weekly Enrollment Snapshot for 2018 Open Enrollment Period. Retrieved February 7, 2018, from https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2017-Fact-Sheet-items/2017-12-28.html?DLPage=1&DLEntries=10&DLSort=0&DLSortDir=descending.

41National Academy for State Health Policy (February 7, 2018). State Health Insurance Marketplace Enrollment (plan selections) 2017 and 2018. Retrieved February 23, 2018, from https://nashp.org/state-health-insurance-marketplace-enrollment-2017-and-2018/.

42See http://us.milliman.com/insight/2017/Reinsurance-and-high-risk-pools-Past--present--and-future-role-in-the-individual-health-insurance-market/?lng=1048578 for more information.