Just over one-third (37%) of super funds’ pension products employ derivatives to protect retirees against market downturns, according to a new Milliman research report.

It represents an opportunity given funds must meet the demands of retiring Baby Boomers who are living longer but face historic low returns from defensive assets. In many cases, risk averse retirees need to take on more investment risk but cannot bear volatility or market crashes as they drawdown on a lifetime of savings.

The majority of super funds are already using derivatives across a wide range of areas including hedging, dynamic asset allocation, physical security exposure replacement and fund manager transitions.

However, a number of funds still raised concerns about costs and the effectiveness of using derivatives for risk management and tail risk hedging, according to the Milliman survey.

The situation is likely to change as those funds in the industry that seek to be in the business of retirement and not just accumulation recognise the unique goals and needs of older Australians.

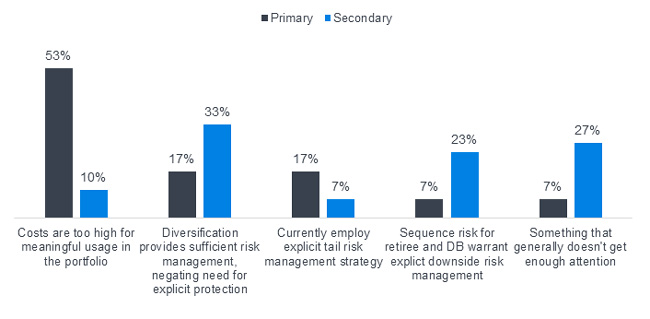

Figure 1: General views towards downside risk management and tail risk hedging

Source: Milliman Derivative Usage in Australian Superannuation Fund report 2017

Managing costs

More than half (53%) of super funds surveyed said that the cost of using derivatives for downside risk management and tail risk hedging was too high, according to the Milliman survey.

Fees can have a compounding impact on long-term returns. However, the real question is whether they provide a greater benefit than their cost. This can only be judged through the prism of members’ goals, which is shaped by super’s underlying purpose.

Australia’s $2.3 trillion pot of super savings has been built with an accumulation mindset– increasing contributions and chasing the highest possible investment returns–but that is changing.

Super’s purpose is vastly different and has only just been enshrined in law: to provide income in retirement to substitute or supplement the Age Pension. That is not a simple goal given the Age Pension is effectively a government-guaranteed lifetime annuity indexed to inflation.

It means older Australians cannot use super for its intended purpose if their savings are exposed to excessive volatility and the risk of market crashes. They are particularly loss averse–and so are more likely to switch investments at the wrong time–while exposed to sequence risk.

Sequence risk describes the significant impact of negative returns that strike just before or just after a retiree starts making withdrawals. They don’t have the time to recover unlike younger investors, who are still making contributions and can benefit from buying cheaper assets.

Meanwhile, many older investors will have to take on more market risk to fund decades in retirement at a time when the global financial crisis has left cash and fixed income returns at anaemic levels.

Over the year ended September 30, 2017, super funds’ diversified fixed interest options returned 1.41%, underperformed cash, which delivered 1.68%, according to SuperRatings.

While downside protection always has a cost, futures-based dynamic risk management overlays avoid the higher cost of implied volatility embedded within option pricing. Further, with the ability to create custom synthetic option strategies over lower-risk diversified portfolios (as opposed to purchasing high-cost equity options), funds are learning downside protection may be cheaper than traditional option purchase protection strategies.

Milliman’s overlay services can reproduce a custom put option payoff for a given portfolio. The expected cost of any option is directly associated with the expected volatility or risk of the underlying portfolio. With the ability to create a custom option on a diversified portfolio, which has lower risk than just the equity component, funds can gain a defensive mechanism for the entire portfolio with significantly lower drag than using physical option purchases on equity options (avoiding arguably the most expensive way to protect downside risk).

Many option-based strategies attempt to manage those costs by either lowering protection or increasing complexity and execution risk.

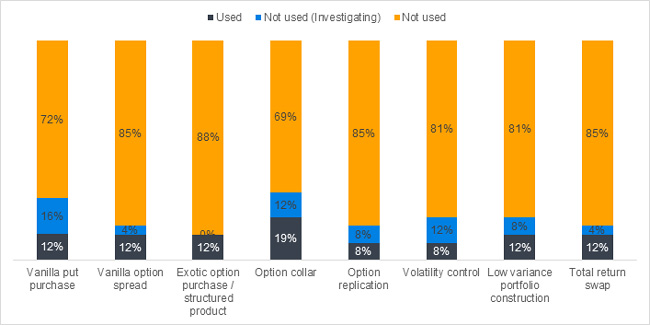

Figure 2: Strategy the fund is currently using or investigating for explicit equity risk management

Source: Milliman Derivative Usage in Australian Superannuation Fund report 2017

The limits of diversification

Diversification is an important risk management technique, but the global financial crisis revealed its limits by wiping more than 21% from super funds in 2008 and 2009.

Australian funds are still highly leveraged to equity market performance, posting the second- highest allocation to shares (51%) among 34 developed countries in 2016, according to an OECD analysis.

The impact of central banks’ quantitative easing programs has also weakened the traditional diversification benefits of bonds, which are producing historic (and in some cases) negative yields.

A rising interest rate environment may bring greater volatility, capital losses and fewer diversification benefits from traditional ‘defensive’ assets.

Yet 17% (primary view) and 33% (secondary view) of survey respondents said diversification was an adequate risk management strategy that replaced the need for explicit portfolio protection, according to the Milliman survey.

The value of risk management strategies is not as apparent when volatility is low and markets steadily rise over an extended period.

The median balanced super fund has posted eight consecutive financial years of positive returns since the global financial crisis. Investment returns in six of those years have been no lower than 8.7% as central banks around the world have flooded markets with liquidity, pumping up asset prices.

However, market cycles continue and funds should carefully consider the needs, goals and behaviour of their entire member base through good and bad times.

For example, Maritime Super’s average active member account balance was $191,000. Almost half (48.9%) of its members were at least 50 years of age at June 2016, according to APRA data.

Market volatility and potential downturns would particularly hurt their members, which is why the fund appointed Milliman to manage a risk management overlay across its entire MySuper option from 1 July 2016.

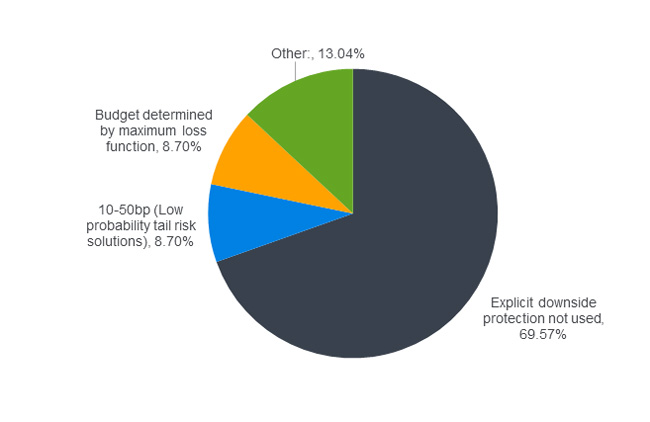

The Milliman research report found that 31% of MySuper funds are currently using explicit downside protection strategies.

Figure 3: Funds’ MySuper budget for explicit risk management strategies (upfront costs and/or expected performance drag per year)

Source: Milliman Derivative Usage in Australian Superannuation Fund report 2017

As funds increasingly weigh up these challenges, we expect their use of derivatives to manage market risk will inevitably increase to meet the specific needs and goals of an ageing population.

For more information about the derivatives survey or Milliman’s services, contact Michael Armitage at [email protected].

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

These results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown. Milliman does not manage the underlying fund.

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.