The challenge

A large regional employer had experienced tremendous growth in recent years due to several acquisitions.

The initial challenge post-merger was to develop a successful integration process which would create a new identity and shared vision for the combined organization. One aspect of this process focused on a comprehensive review of all employee benefit programs, including the retirement program. The primary goal of this analysis was to assess the competitiveness of its retirement program as compared to its peers.

The solution

We proposed preparing a “peer group” analysis, which would demonstrate the competitiveness of the retirement program.

Phase 1 – Quantify current retirement program

In phase 1, we focused on quantifying the coverage and benefits provided under the current retirement program.

Defined benefit plan

The employer sponsors a frozen defined benefit (DB) plan, which was the culmination of the merging of several frozen DB plans acquired through the recent acquisitions. Only a small percent of current active employees (12%) were entitled to some benefit under the plan. The plan offered traditional DB features. For example, it offered subsidized early retirement benefits and multiple annuity payment options.

Defined contribution plan

The primary retirement plan was an ongoing 401(k) plan. The plan provided for a 100% employer matching contribution on the first 4% of employee deferrals with a 50% employer matching contribution on the next 2% of employee deferrals. This resulted in a maximum 5% employer matching contribution when employees deferred 6% or more. Our plan analysis showed a 71% participation rate with an average employee deferral rate of 5.3%. The average plan participant was age 42 with a $54,000 account balance.

Combined retirement program

Under the current program, benefits were primarily provided through the defined contribution program. Overall participation was modest (29% of employees elected to forgo deferrals) with the average deferral rate lower than what was required to receive a full matching contribution.

Phase 2 – Understand retirement programs of peers

The employer identified a peer group which included five competitors with similar characteristics (geographic location, size, number of employees, etc.). Analyzing recent IRS Form 5500s and 10-K filings, we were able to determine the retirement programs offered by each of these competitors.

Phase 3 – Develop comparative measurement

A replacement ratio (RR) defines a person’s gross income after retirement, divided by his or her gross pre-retirement income. This is a common measurement used to assess the adequacy of an individual’s retirement income. Historically, a 70% to 80% target RR is cited as the minimum required RR for an individual to maintain his or her standard of living in retirement. The target RR is the sum of the retirement income an individual would receive from employer-provided retirement programs, Social Security, and personal savings.

For purposes of our peer group analysis, the RR measurement offers a method to standardize the variety of retirement programs offered by the employers included in this analysis.

RRs were developed for the employees under their current retirement program. Additionally, we calculated RRs for employees as if they were participants in each of the five retirement programs in the peer group. Assumptions used for this analysis included the following:

- Retirement programs would remain unchanged

- Employees would continue current deferral rates until normal retirement age

- Normal retirement age of 65

- Future compensation increases of 3.0%

- Defined contribution investment returns were based on age-based allocation

| Age | Annual Return |

| 21-29 | 7.00% |

| 30-39 | 6.50% |

| 40-49 | 6.00% |

| 50-59 | 5.50% |

| 60+ | 5.00% |

- Defined contribution account balances were converted to an annuity based on consistent assumptions

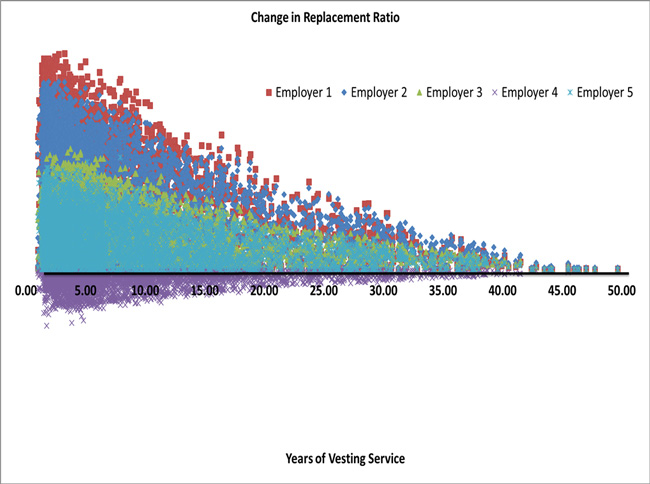

A major challenge was how to display the results of this analysis. We developed the graph below which uses the x-axis as a baseline for the employer’s current retirement program. Participants were sorted based on years of vesting service from the original date of hire. For each participant, we determined the delta between the RR under the current retirement program and the RR under each of the five peer group programs. Plots above the x-axis indicate that the peer group plan provides a larger RR (and thus better benefits) for that participant. Plots furthest above the x-axis indicate that the peer group plan is much better than the current plan for the selected participant. Plots below the x-axis, a negative delta, indicate the current plan provides a better RR than the peer group plan.

The outcome

Most of the plots on the graph are above the x-axis, indicating that the peer group retirement programs generally offer better retirement benefits (four of the five peer group members). In some cases, the difference is substantial. Only peer group member 4 offers a less generous retirement program as indicated by the plots below the x-axis.

Prior to our analysis, the employer believed that its retirement program provided average retirement benefits when compared to its peers. The results of our analysis provided an “apples to apples” comparison of retirement programs and was crucial in demonstrating that the employer’s current retirement program was weak when compared to its peer group. In an effort to retain key talent and keep employees satisfied, the employer also realized that it would need to improve its current retirement program.

After our meeting, the employer decided to engage Milliman for a retirement redesign project to review alternative retirement program designs with the following goals:

- Broad coverage

- Meaningful benefits

- Competitive and cost effective

- Attract and retain talented employees

- Innovative, differentiator