The challenge

A Milliman client was interested in gradually immunizing its liabilities over an extended period of time as the funded status its pension plan improved. The goal was to immunize liabilities on an accounting basis and be able to make investment decisions on a daily basis, based on the daily funded status of its pension plan. This was accomplished with a Milliman tool and in conjunction with a “glide path” investment approach established by our client and its investment consultant.

A “glide path” investment approach moves assets into fixed income in favorable market conditions and as the plan becomes better funded. It maintains a good balance of retaining equity investments and lowering the volatility over time as the funded status improves. With this approach, the liabilities gradually become immunized while allowing the equity portion to seek better returns.

A measure of the funded status was defined and reallocation trigger points were identified and agreed upon in advance. The client viewed the funded status used for public disclosures as a good basis for measuring the financial health of its pension plan. Analysts and investors would typically agree. For accounting purposes, pension plan liabilities are measured on the last day of the fiscal year. This means that the discount rate used to value those liabilities must be measured as of the same day. In today’s market, the change in discount rates from day to day can vary significantly.

Solution

Discount rate indicators are typically only available on a monthly basis. The most popular discount rate reference is the Citigroup yield curve, but again, this is only available at the end of the each month. Our client wanted to make investment reallocations based on live market values of its pension plan, sometimes on a daily basis, and be able to react to market changes when they happen. To assist our client with its objectives, Milliman created a tool that develops daily discount rates and measures pension liabilities on a daily basis.

The Milliman Daily Funded Status model (DFS) is a fully automated model that pulls in market indices, develops a unique yield curve of interest rates, pulls in asset information directly from the trustee, and calculates the liabilities of a pension plan, all on a daily basis. One of the features of the DFS model is the automatically generated emails, texts, and/or website updates with real-time market information regarding the liability and funded status of a pension plan.

The estimated daily discount rate is based on publicly available daily interest rate indicators that track well to pension plan benefit payment patterns. The calculated effective yields are then converted into spot rates. Whether a plan uses a Citigroup yield curve or a custom bond model to develop a yield curve, the DFS can simulate interim yield curves to closely and accurately approximate either basis to determine a discount rate for all business days of the year.

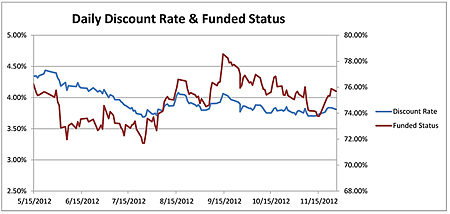

During the summer of 2012, the interest rate environment continued to be volatile. Pension discount rates exhibited a downward trend and sometimes jumped significantly from one week to the next. Below is a chart that shows the volatility of our client’s discount rate from May 15 to November 27, measured on a daily basis. The chart also shows the funded status of its plans (in aggregate) over the same period.

On May 15, the discount rate was 4.35%. The discount rate bounced up for about a week and then trended downward to a low of 3.69% on July 25. The discount rate has oscillated up and down since then while leveling off at 3.84% on November 27.

The outcome

For our client utilizing a “glide path” approach and access to daily information on the status of its pension plans, a good opportunity presented itself before the end of July to reallocate assets. They made a significant asset reallocation of nearly 10% of the plan’s assets (from fixed income to equities) when the funded status and market discount rates were at a low. As a result, our client took advantage of a subsequent uptick in the market. The funded status of the pension plan increased at a faster rate than it would have if our client had had access only to information on a monthly basis.

A “glide path” approach with the DFS model helped our client make investment reallocations at opportune times during the market business cycle. Going forward, they are able to take a more proactive approach to managing the funded status of its pension plan, thus, accomplishing its goals of lowering volatility and immunizing liabilities on any chosen day.