The challenge

A small insurance client in New England has a well-funded defined benefit (DB) plan that is open to new entrants. They also sponsor a defined contribution (DC) plan that has a low employer contribution. They rely on their benefits to attract new employees. The client felt that the program was getting stale and was not “unique” enough to stand out to prospective hires among their competitors. The client requested that Milliman provide a report that offered alternatives to their current program that would be attractive to their current and prospective employees.

The Milliman solution

Milliman’s report presented a number of ideas and covered methods for more equitable sharing of risk between the plan sponsor and plan participant. The options presented could, in most cases, be mixed and matched to achieve the level of updating, efficiency, and volatility control that best suited the client.

In the report, we demonstrated the various risks involved in retirement plans (interest rate, mortality, and investment risks) and where each of those risks resides for both defined benefit plans (all with the plan sponsor) and defined contribution plans (all with the participant).

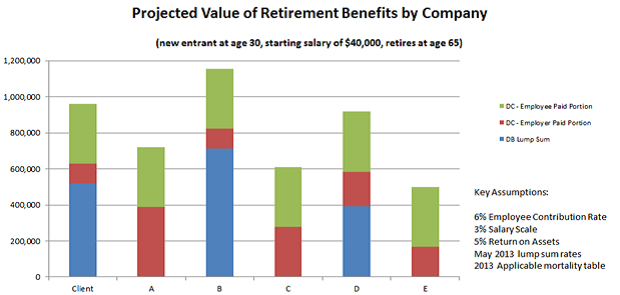

In order to get a feel for the magnitude of change needed in their current plan to stand out from other like employers, our client needed to compare their current benefit program to their competitors’ programs. In this context, the list of competitors was provided by our client and includes those companies in the same geographical area that would compete for the same employees, not necessarily competitors in the same line of business. Comparisons of projected retirement benefits at age 65 were made to five competitors for new entrants of age 30, 40, and 50 in order to give the client an idea of how various employees may accrue benefits over their careers.

Below is a one of the comparison charts provided illustrating their relative rank in benefits provided:

A key takeaway from the comparison of benefits was that those employers providing DB plans to their employees stood head and shoulders above those that do not, resulting in an easy distinction for those potential employees looking for a complete benefits offering.

We focused on changing the perception of the employees’ retirement benefit from being two separate plans (DB and DC) with two separate benefits, to a single retirement benefit with DB (annuity) and DC ($ balance) components that the employees can better understand and customize to their individual needs. Such alternatives included:

1. Allow participants to annuitize DC account balances without the excessive fees and expenses of purchasing an annuity from an insurance company. This can be accomplished by allowing participants to rollover DC account balances into the DB plan. The DB plan would then provide a monthly benefit equal in value to the DC account rolled over. The benefit provided under the DB plan would be covered by the Pension Benefit Guaranty Corporation (PBGC), giving the participant the safety of a guaranteed monthly pension. From the participant’s perspective, the DC plan would essentially have an annuity option available at retirement without any additional cost.

2. Synchronize the vesting schedules under the DB and DC plans. The client currently provides full vesting after 5 years under the DB plan, but only 3 years under the DC plan. By changing the vesting requirement to 3 years for the DB plan, the client could define retirement eligibility under both plans with the same requirement, making the total retirement program appear more seamless at a minimal cost.

3. Allow phased retirement. This plan change provides tangible benefits to both the plan sponsor and the participant. It benefits participants by giving them the opportunity to structure a transition into retirement that works best for them by allowing them to collect their pension while working a reduced number of hours. Plan sponsors reap the advantages of keeping experienced employees who can assist in the transfer of knowledge to the next generation of workers.

4. Modify the plan to be a “Variable Annuity Plan.” Variable annuity plans are a type of DB plan that allows benefits to fluctuate along with changes in the plan’s investment return, thereby resulting in a plan similar to a DC plan with the added benefit of an annuity option and PBGC guarantee.

5. Change the plan from a final average pay plan to a hybrid pension plan. A hybrid plan (such as a cash balance plan) is a DB plan that provides participants with a better understanding of the value of their benefit because it is expressed as a lump sum amount, just like a DC plan would be communicated.

6. Allow partial lump sums. Rather than taking an all or nothing approach under the DB plan, participants have the flexibility to annuitize only a portion of the DB benefit based on the individual participant’s needs and risk tolerance.

None of the clients’ competitors currently utilize any of the alternatives presented, allowing our client to further distance themselves from the other local employers in terms of benefit attractiveness. After presenting the pros and cons of each of the options, we explained the importance of risk mitigation to the client. At this point, we separated the risk management techniques by sources of risk; the first set of options communicated to our client focused on asset-based methods for addressing volatility and the second set of options approached the problem, and solution, from the liability side.

The asset-based solutions hit on such topics as liability driven investment strategies and dynamic asset allocation. The liability focused strategies included analysis of different types of benefit formula changes as well as changes to plan provisions to shift some of the risks away from the plan sponsor.

The outcome

Milliman consultants met with the plan sponsor to discuss the options presented in the report. Based on the report, the plan sponsor decided the plan’s attractiveness would be most effectively improved by changing to a shorter vesting period and allowing for partial lump sum payouts upon retirement. These options will be presented to the board at their upcoming meeting.

As an additional benefit to the client, the study allowed them to see how strong their benefit offerings are and they agreed that an employee communications program would be a great way to promote this among their current employees. Milliman’s communications team will be involved in this important project.

In the final analysis, all of the goals of the plan sponsor have been addressed; they now know how their retirement program ranks with its peers and can modify the plan accordingly utilizing any number of the alternatives presented to them. The client is now aware of a number of volatility control measures that they can employ (both on the asset and the liability side). By bringing together an attractive, more up-to-date benefit plan with better risk sharing between all interested parties, our client has the tools available to maximize the efficiency of not only their benefits dollars, but also the benefits themselves.