Background

During 2015, the American Academy of Actuaries issued a white paper discussing the change in accounting procedure AT&T implemented. AT&T changed how they applied their discount rate from using a yield curve to set a rate to using the yield curve to directly calculate their liability and interest cost (alternative 1 below). These calculations are referred to as cost recognition strategies and, while a few alternatives exist, plan sponsors who’ve decided to change approaches are all choosing the same one: the spot rate approach, where the yield curve is used to calculate the projected benefit obligation (PBO), service cost (SC), and interest cost (IC).

- Current strategy. Use a yield curve (or custom bond portfolio) to set a single equivalent discount rate. This discount rate becomes an input for all other calculations. Calculate the PBO as of the beginning of the year and roll it forward to the financial disclosure measurement date. Interest cost is calculated using the same single equivalent discount rate. The same discount rate is used to calculate SC.

- Alternate strategy. Apply a yield curve directly to plan cash flows to discount those cash flows directly to the financial disclosure measurement date. Under this approach, the yield curve is the input. The yield curve is applied separately to calculate the PBO, SC, and IC. The PBO remains unchanged, SC generally decreases, and there are two alternatives for calculating interest cost the Securities and Exchange Commission has said they would not object to:

1) Spot rate approach. Apply the spot rates from the yield curve to the corresponding discounted cash flows. For example, the interest cost associated with the year 15 cash flow would be based on the year 15 spot rate. Result: moderate reduction in interest cost, e.g., could be up to 25% to 40%.

2) Forward rate approach. Apply the forward rates from the spot rate yield curve to the corresponding discounted cash flows. This works just like alternative 2 except the forward rate curve must be calculated from the spot rates. Result: tends to increase interest cost.

The challenge

A client who used a custom bond model to set their discount rate for their ASC 715 financial disclosures wanted to change to using the spot rate approach to recognize their annual pension cost. They have four pension plans ranging from under $20 million in PBO to over $1 billion. Using all the plan cash flows combined, the client selected a single discount rate to apply to all the plans.

Toward the end of 2015, we discussed the alternate approaches with our client. The client was interested in learning more about the alternatives, but was concerned they wouldn’t be able to switch because they used a custom bond model for setting the discount rate. The alternatives require a yield curve, but the bond model does not produce a yield curve.

Our client was concerned they would have to change their discount rate setting methodology from a bond matching approach back to using a yield curve. They adopted bond matching because they argued bond matching was more accurate and consistent with how they would settle the pension obligation (by buying bonds that match as closely as possible to its expected pension payments). Having made this argument, it would be difficult to argue the reverse. In addition, the SEC has since frowned upon this sort of change, confirming the concerns.

Milliman solution

During an initial meeting, we expressed our belief that we could produce a reasonable yield curve from the bonds in the bond portfolio. Following this discussion, we tested our theory. Using the prior year’s bond portfolio and following the Fed’s method for building the Treasury yield curve, we built a yield curve that reproduced the discount rate our client used for financial accounting. This curve allowed our client to implement the spot rate approach.

In short order, we moved from “is this possible?” to “let’s do it.” The primary hurdle between “let’s do it” and final sign off was working with our client’s auditor. The auditors were cautious because this approach was relatively new and a bit different from what AT&T implemented (not necessarily unusual or risky, but new and different). It took several discussions to help the auditors understand the difference between what the SEC frowned upon and the change our client was making.

The crux of the matter was the bond universe. The auditors were concerned we were using the custom bond portfolio to calculate PBO, but a separate yield curve, like the Citi Pension Discount Curve, to calculate the interest cost. Through our discussions, we made it clear that our approach was to build a custom yield curve from the client’s custom bond portfolio and use that yield curve to calculate both PBO and interest cost. Because the yield curve we built was based on the plans’ custom bond portfolio, the resulting PBO (for all plans combined) was unchanged and there was consistency between the PBO and interest cost calculations. Ultimately, the auditors approved the change in approach.

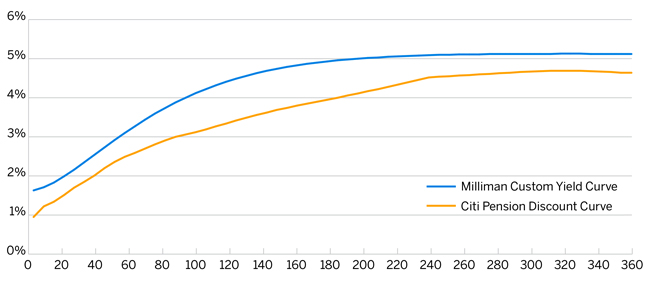

The table below compares the resulting custom yield curve and the Citi Pension Discount Curve.

Figure 1: Spot Rate Yield Curves at December 31, 2015

Outcome

Our client was thrilled with our flexibility, creativity, and responsiveness. They felt the application of the spot rate approach provided a more consistent application of the yield curve across the spectrum of pension accounting calculations. The client liked that there was no impact on the PBO, and though not a driver, the way the various components of pension expense were recognized in their financial statements was viewed favorably.