The Variable Annuity Pension Plan (VAPP) is now the Milliman Sustainable Income PlanTM (SIP).

A variable annuity pension plan (VAPP) provides a new way to balance the major risks associated with retirement plans investment risk, longevity risk, and interest rate risk. In defined contribution (DC) plans, all of these risks are borne by participants. In defined benefit (DB) plans, all of these risks are borne by the employers. A VAPP shares these risks, resulting in predictable annual contributions for the employer, similar to a DC plan, and monthly income for life for participants, similar to a DB plan. Proposed VAPP benefit stabilization features could provide even more security for the participants.

Under a VAPP, the investment risk is borne by the participants but the longevity risk is retained by the plan. Interest rate risk is largely eliminated for both plan sponsor and participant under this design.

VAPP features

A VAPP is a DB plan that stays fully funded by adjusting benefits annually for active employees and retirees, based on the investment return of the plan assets. This means that benefits can go both up and down depending on the markets. As with a DC plan, this passes the investment risk on to the participants. However, unlike a DC plan, the benefits are payable monthly for life and, if elected, for the life of a spouse. This keeps the longevity risk pooled within the plan instead of requiring each participant to guess at his or her life span.

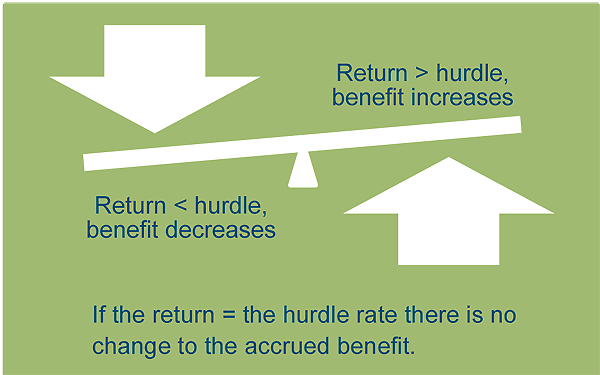

A key feature of the plan is the hurdle rate, which is generally set between 3% and 5%. Benefits go up and down each year by the difference between investment returns and the hurdle rate.

5%. Benefits go up and down each year by the difference between investment returns and the hurdle rate.

As an example, suppose a retiree has a benefit of $1,000 per month in a VAPP with a 4% hurdle rate. If the asset return is 10.2% for the year, the retiree's benefit will adjust to $1,060 per month next year: $1,060 = $1,000 x (1.102 / 1.04).

If, in the example above, the return were -2.2% instead of 10.2%, the participant's benefit would go down to $940. Clearly, the benefits in a VAPP could produce a bit of a bumpy ride for retirees. However, there are some proposed modifications to VAPPs that would provide benefit stability for participants without increasing contribution volatility for sponsors.

One positive feature of the VAPP is expected inflation protection. Just because the hurdle rate is usually between 3% and 5% doesn t mean that the plan assets need to be invested with that as their target return. In fact, most plans would likely continue investing their assets as they are now, targeting a 6% to 7% rate of return. Over time, returns in excess of the hurdle rate would produce some expected growth in the benefit. This expected growth continues during retirement, which would help the retiree's benefit keep up with inflation.

Why a VAPP and why now?

VAPPs have been around, and legal, since the 1950s. Anecdotal data suggests that benefit volatility in the 1970s caused VAPPs to fall out of favor with participants. Additionally, during the 1980s and 1990s, DB plans were paying for themselves with excellent asset returns and plan sponsors were not as concerned with the ongoing cost of the plans.

The market corrections in the first part of the 2000s and again in 2008, coupled with the enactment of the Pension Protection Act of 2006 (PPA), have caused significant increases in DB plan contribution magnitude and volatility. Sponsors have often turned to DC plans as a way to reduce their risk. However, this has shifted all of the retirement risks to the employees. A recent study by Towers Watson suggests that younger employees have recognized this risk burden and are shifting their preference toward DB plans, perhaps after witnessing the impact of 2008 on the retirement security of their parents generation.

We cannot predict the future. We need plans that are robust and successful in all economies, at all levels of plan maturity, regardless of life expectancy, and in the face of various funding rules and accounting standards. Variable annuity pension plans are one way to address these concerns.

A variable annuity pension plan (VAPP) provides a new way to balance the major risks associated with retirement plans investment risk, longevity risk, and interest rate risk. In defined contribution (DC) plans, all of these risks are borne by participants. In defined benefit (DB) plans, all of these risks are borne by the employers. A VAPP shares these risks, resulting in predictable annual contributions for the employer, similar to a DC plan, and monthly income for life for participants, similar to a DB plan. Proposed VAPP benefit stabilization features could provide even more security for the participants.

Under a VAPP, the investment risk is borne by the participants but the longevity risk is retained by the plan. Interest rate risk is largely eliminated for both plan sponsor and participant under this design.

VAPP features

A VAPP is a DB plan that stays fully funded by adjusting benefits annually for active employees and retirees, based on the investment return of the plan assets. This means that benefits can go both up and down depending on the markets. As with a DC plan, this passes the investment risk on to the participants. However, unlike a DC plan, the benefits are payable monthly for life and, if elected, for the life of a spouse. This keeps the longevity risk pooled within the plan instead of requiring each participant to guess at his or her life span.

A key feature of the plan is the hurdle rate, which is generally set between 3% and

5%. Benefits go up and down each year by the difference between investment returns and the hurdle rate.As an example, suppose a retiree has a benefit of $1,000 per month in a VAPP with a 4% hurdle rate. If the asset return is 10.2% for the year, the retiree's benefit will adjust to $1,060 per month next year: $1,060 = $1,000 x (1.102 / 1.04).

If, in the example above, the return were -2.2% instead of 10.2%, the participant's benefit would go down to $940. Clearly, the benefits in a VAPP could produce a bit of a bumpy ride for retirees. However, there are some proposed modifications to VAPPs that would provide benefit stability for participants without increasing contribution volatility for sponsors.

One positive feature of the VAPP is expected inflation protection. Just because the hurdle rate is usually between 3% and 5% doesn t mean that the plan assets need to be invested with that as their target return. In fact, most plans would likely continue investing their assets as they are now, targeting a 6% to 7% rate of return. Over time, returns in excess of the hurdle rate would produce some expected growth in the benefit. This expected growth continues during retirement, which would help the retiree's benefit keep up with inflation.

Why a VAPP and why now?

VAPPs have been around, and legal, since the 1950s. Anecdotal data suggests that benefit volatility in the 1970s caused VAPPs to fall out of favor with participants. Additionally, during the 1980s and 1990s, DB plans were paying for themselves with excellent asset returns and plan sponsors were not as concerned with the ongoing cost of the plans.

The market corrections in the first part of the 2000s and again in 2008, coupled with the enactment of the Pension Protection Act of 2006 (PPA), have caused significant increases in DB plan contribution magnitude and volatility. Sponsors have often turned to DC plans as a way to reduce their risk. However, this has shifted all of the retirement risks to the employees. A recent study by Towers Watson suggests that younger employees have recognized this risk burden and are shifting their preference toward DB plans, perhaps after witnessing the impact of 2008 on the retirement security of their parents generation.

We cannot predict the future. We need plans that are robust and successful in all economies, at all levels of plan maturity, regardless of life expectancy, and in the face of various funding rules and accounting standards. Variable annuity pension plans are one way to address these concerns.