Whether or not Abenomics is successful, it has set the stage for rising interest rates in Japan. It is not a matter of if rates will rise; it is a matter of when and how quickly. Many companies are ill prepared. A handful will do well; some will be hurt. An industry shakeout appears likely.

If Japan’s economy does improve—if inflation hits 2% and nominal growth exceeds that, we will see an increasing real demand for money. Rates will rise; 10-year Japanese Government Bonds (JGB) yields of 3% or 4% would be normal and expected—indeed, they would be low—in a growing economy. If Abenomics fails it will hasten the inevitable—a debt crisis. Contrary to appearances, the domestic and global appetite for JGBs is not unlimited. The banks, insurers, and pension funds now holding government bonds will at some point need to redeem these assets to fund obligations owed to Japan’s aging populace. Facing a diminishing demand for JGBs, Japan will need to monetize its debt; the result will be inflationary. Nominal rates may rise. Japan will not be able to fund its debt at current levels indefinitely.

We face a double-edged sword. If Japan’s economy does well, demand for money will push rates up. If growth is sluggish, falling demand for JGBs will drive borrowing costs higher. In either scenario, current low rates will not persist.

Danger to the life insurance industry

The following is a certainty: if interest rates rise in Japan, policyholder behavior will change. Policyholders will not be passive.

If policyholders can trade low-yielding life insurance policies for bank deposits earning 2%, many will choose to do so. If competing insurers offer attractive rates on innovative life or annuity contracts, money will flow to those companies.

When rates rise by 100 to 200 basis points—hardly a radical scenario—we will see an increase in lapses. If rates rise further, we may see a stampede.

Insurers believe that liability durations are long. They assume that policyholders will remain generally loyal, even in the face of rising rates. Cash flow projections and liability calculations are premised on this assumption. Up to a certain point, it is reasonable. But a spike in interest rates will certainly lead to higher lapses; liability durations may drop precipitously. Liquidation of assets will lead to losses, potentially material ones. There will be knock-on effects as well. As healthy policyholders lapse, persisting books will show impaired mortality and morbidity. It is not an attractive picture, but it is one we cannot ignore. And it is one we can prepare for.

Insurer response to date

While insurers are aware of these risks, only a few have responded proactively. Many seem to believe the following:

- Asset portfolios contain adequate liquidity to support increasing cash surrenders

- Cash outflows can be mitigated through internal replacement programs

- Customers are generally loyal; even in the case of a severe interest rate spike, surrender pressures would increase only moderately

These views are not reassuring. Asset portfolios are liquid enough to support a moderate increase in lapse rates—for example, an increment of 3% to 4% of liabilities—but few companies are prepared to respond to cash demands that equal 10% of liabilities and persist for several years.

In recent years, product design has to some degree envisioned disintermediation risk. A small percentage of liabilities are subject to market value adjustments. Low cash value policies may reduce this risk as well.

Internal replacements could indeed mitigate cash needs, but not without a cost, and strategies require careful consideration. Higher surrenders and increasing competition may emerge quickly; very few companies have attractive replacement products “on the shelf.” Companies need to take action to design product portfolios that will facilitate competition with both banks and the new breed of insurer that will emerge in a rising rate environment.

New product strategies: Need for a proactive response

Insurers cannot wait for the crisis. They must innovate now. The first line of defense is an assessment of product strategies.

Insurers must be ready with products that will respond to policyholder demands in an environment of rising rates. Such products might include, for example, variable life or variable annuities incorporating equity protection strategies. With this in mind, the Milliman Managed Risk Strategy can greatly facilitate VA/VL design and implementation.

A new generation of par and semi-par products can be developed that offer attractive current rates on lump sum premiums.

Given the very large margins that still exist on mortality and morbidity in Japan, there are strong arguments in favor of a universal life style approach to current and guaranteed rates; insurers would offer more attractive protection premiums while investing reserves in shorter-term assets. This would facilitate a more rapid response to rising rates; policyholders would enjoy lower fees for protection and would share in rising rates. From the insurer perspective, loss of mortality and morbidity margins would be compensated for by a more balanced investment risk profile.

Revisiting ALM strategies

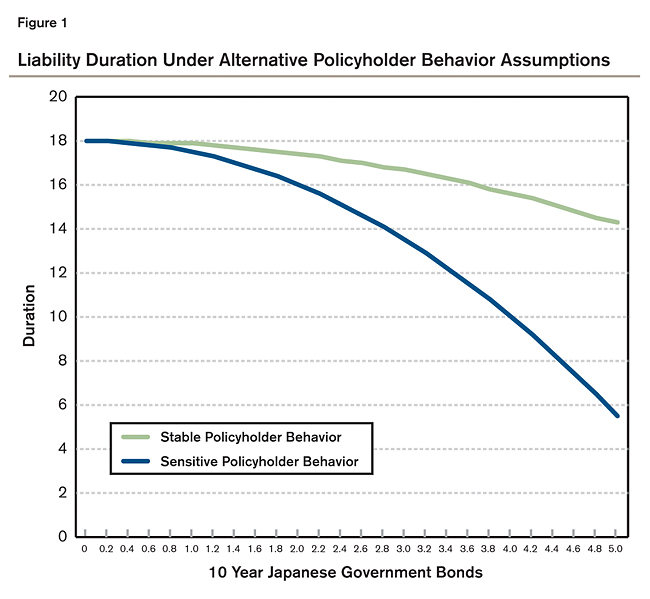

Insurers need to design asset liability management (ALM) strategies that reflect the possibility of materially rising rates. Many companies conclude that liability durations are long because they envision only relatively mild shocks to interest rates and relatively stable policyholder behavior.

Unfortunately, convexity may be larger than is typically anticipated: duration may decline precipitously as interest rates rise. This is illustrated in Figure 1, which compares the liability duration for a block of business under typical assumptions regarding policyholder behavior with the curve that emerges under an assumption of greater dynamic lapse sensitivity.

As long as yields remain below 2%, calculation of duration is relatively straightforward. However, as yields rise well above 2%, the situation is far less certain. If nominal yields were to rise into the 3% to 5% range, it is not unreasonable to anticipate a dramatic decline in duration on many blocks, as illustrated in Figure 1. Such a decline would have serious ramifications for many insurers.

In spite of this, many companies continue to acquire ultra-long JGBs and to pursue strategies aimed at extending asset durations. Such strategies, while improving asset liability matching under relatively stable scenarios, may actually be increasing balance sheet risk when the potential for more severe stresses is reflected.

In order to compensate for such scenarios, companies should explore dynamic hedging and other risk mitigation strategies.

Predictive analytics, policyholder behavior, and the strategic response

While the cost of a blanket hedge of the general account against rising rates may be prohibitively expensive, companies should examine liabilities block by block in order to determine which are at highest risk in a rising rate scenario. This examination can be facilitated by predictive analytics and Bayesian techniques and can support the development of in-force management programs and targeted approaches to hedging.

While companies routinely study lapse experience by duration and product attributes, very few conduct analyses to evaluate the degree to which experience will evolve as external conditions change. Many factors will drive dynamic policyholder behavior and predictive analytics can help uncover these key drivers.

Undoubtedly, behavior will vary by generation, product type, distribution channel, customer demographic, and even agent demographic. Single pay products are likely to exhibit greater lapse sensitivity than recurring pay products. Business sold through bank channels will almost certainly exhibit great sensitivity than business sold through a traditional agency force. Customers with deteriorating health will be less likely to lapse. Business sold by younger agents may exhibit greater sensitivity than that sold by more mature salespeople.

It is essential that companies develop monitoring protocols as a routine component of risk management. With appropriate methods in place, companies will be able to measure risk and respond proactively to it.

A strategic opportunity

An industry shakeout is in the making. The emerging crisis will not be as severe as the one faced in the late 1990s, but it will lead to a realignment in the industry. New players will emerge and some of today’s larger companies will be seriously weakened. There is a danger that the entire life insurance industry will lose market share to Japan’s banks.

But this coming crisis can be viewed as a potential opportunity. Companies that respond now, before the crisis, will emerge larger, stronger, and more profitable. In order to achieve this result, companies will need to assess both their own strengths and weaknesses and the strengths and weaknesses of their competitors. They will need to revise product strategies, approaches to ALM, and overall risk management protocols.

Most of all, they need to act with some sense of urgency. Inaction may have serious consequences.