Keenan and Milliman have prepared this report in collaboration, in order to help assist in the development of improved workers' compensation management practices.

Executive summary

Definitions

- Total incurred: The loss that has been paid plus case reserves

- Case reserve: Amounts set on individual claims by case adjusters for future payments

- Exposure: Measure of potential liability; risk

- Frequency: Number of claims per workforce unit, usually stated either in terms of payroll dollars or number of employees

- Indemnity (lost-time) claim: A claims that has incurred an indemnity payment2

- Losses: The total of indemnity, medical, and allocated loss adjustment expense (ALAE) amounts

- Severity: Average loss per claim

- Pure premium: Losses per $100 of payroll

- Paid: Loss amounts that have already been paid

- Ultimate estimate: Estimate of total cost of claims after all payments are made

The issues that hospitals and other facilities are facing today are more complex and continuously changing. The risks of providing medical care and the costs of protecting against those risks alone, including the protection of your employees from injury or illness in the delivery of that care, require hospitals to look closely at questions related to taking fully insured, partially self-funded or self-insured positions. As these facilities are well aware, workers' compensation laws in California make the choice increasingly complex—and important.

Keenan HealthCare and Milliman are pleased to present the results of our first annual California Hospital Workers' Compensation and Payroll Benchmarking Survey. Our hope with this survey and report is to provide industry-wide benchmarks in terms of the fundamentals from which informed decisions related to workers' compensation and maintaining appropriate risk can be made: claim frequency and severity, medical and indemnity costs, the allocated loss adjustment expense (ALAE), and the impact of specific factors such as age, occupation, and more.

In the course of our work on this survey, we gathered data from over 18 hospital systems and/or individual facilities within California (over 35 facilities altogether). In aggregate they provided data on over 3,000 annual claims. Additionally, to facilitate analyzing data on a consistent basis among all participants, we relied on payroll and utilization information obtained from the California Office of Statewide Health Planning and Development (OSHPD) website.

As a result, we identified some general trends in the hospital sector which include:

- Overall losses per $100 of payroll are largely the same in 2013 as they were in 2004; however, we identified two noteworthy trends: 1) Severity of claims is on the rise, increasing by approximately 9.5% annually from 2004 to 2013, and 2) Claim frequency has been declining.

- Losses as a function of payroll appear to have bottomed out in 2008.

- Reforms in 2003 reduced losses as a function of payroll by approximately 40%.

- The projected 2014 loss cost per $100 of payroll (as found in OSHPD reports1) comes to $2.65. Eleven of the 18 systems or facilities included in this study appear within +/- 25% of this projection. Two facilities are greater than 25% of this projection and five are less than 25% of this projection.

This report is divided into sections with charts providing results on an overall basis as well as in specific areas. The first section looks at some of the broad trends as well as others identified in the overall survey results. In the next section, we present numerous charts illustrating trends in specific areas of interest, including payroll and utilization, age, occupation, litigation status, cumulative trauma (CT), and future medical (FM).

Keenan and Milliman are committed to providing the annual California Hospital Workers' Compensation and Payroll Benchmarking Survey and Report. In this first annual report, we have endeavored to provide meaningful data comparisons to assist California hospital management in measuring their hospitals’ results against California peers. We believe these key indicators will be valuable in developing plans for improving your results.

The next survey will begin early fall 2014. Our expectations include a much broader participation by California hospitals in 2014.

Your feedback is important to assure this report meets your needs and expectations. This being the first annual report we enlist your support to make this a tool all hospitals will utilize in measuring results and planning improvements. Please email your comments, thoughts and ideas to:

Bill Poland, Marketing Director-Property & Casualty at [email protected]

Ron Srajer, VP, Keenan HealthCare at [email protected]

Richard Lord, FCAS MAAA, Principal, Milliman at [email protected]

Stephen Koca, FCAS MAAA, Principal, Milliman at [email protected]

We are eager for your feedback.

RESPECTFULLY,

Keenan HealthCare and Milliman

Overall results

The big picture for workers' compensation in California today is not necessarily the right one. The overall results of our survey disclosed two interesting hidden trends, which together paint a picture that is a little different from what it first appears. The exhibits in this section, Figures 1 through 6, provide a review of workers' compensation loss trends for California hospitals over the past decade. They are based on benchmark participant claim experience, Milliman analysis of that claim experience, and payroll or FTE information for benchmark participants as reported to OSHPD.

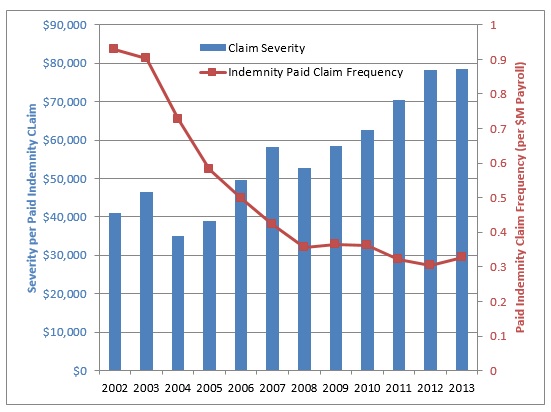

The first trend of note is that severity per paid indemnity claim—i.e., indemnity, medical, and allocated loss adjustment expense (ALAE) combined—showed an increase of approximately 9.5% annually in the period from 2004 through 2013. This may be seen in Figure 1. Note how the drop off in claim severity that occurred in 2003 (represented by the blue bars in Figure 1) actually did little to halt the trend of increasing severity. The drop off was the result of the enactment of reform laws, which provided only short-term measures to halt that trend. The effect was a one-time downward shift in severity with otherwise no effect on the year-to-year upward trend.

At the same time, however, the indemnity claim frequency (represented by the red line in Figure 1) was declining dramatically. This continued until about 2007, when it seemed to find a floor. The net effect of these two trends combined has been that overall losses per $100 of payroll were largely the same in 2013 as they were in 2004.

In reality, while it appears there has been little change there has actually been quite a bit of upward change in severity and downward change in frequency of claims.

Figure 1: Claim Severity and Frequency

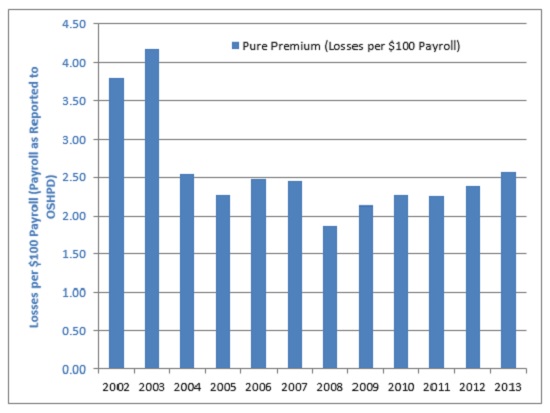

The effects of the 2003 reforms can be observed in Figure 2, where it shows that losses as a function of payroll fell by approximately 40%.

Figure 2: Impact of Reforms on Losses per $100 Payroll

After a dramatic tumble from a high point in 2002, losses as a function of payroll appear to have hit their low point in 2008. After 2008, the frequency decreases have been notably less dramatic, thus with increasing severity we see the resumption of the upward trend in pure premium.

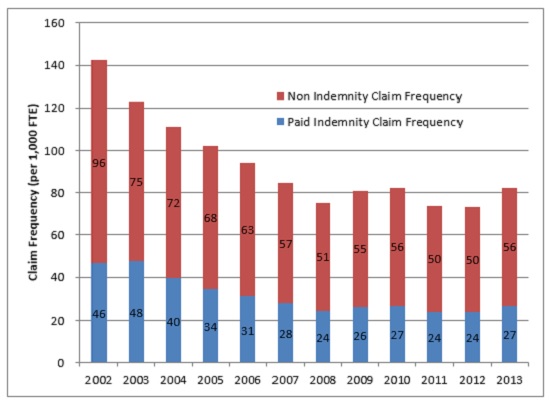

The decline in claim frequency has been seen both in claims that incur an indemnity payment and in medical-only claims. Figure 4 shows the relation between them, with both types of claims seeing significant reductions since 2003.

Figure 4: Combined Indemnity and Non-Indemnity Claim Frequency

Figure 5 illustrates the relative costs of medical-only (non-indemnity) and indemnity claims along with ALAE. The percentage of overall claim costs related to medical has increased over the past 10 years from approximately 50% of total costs to 60%. Meanwhile, the percentage of overall costs related to indemnity benefits has decreased from over 40% of costs in pre-reform years to less than 30% of costs today.

While still the smallest component, ALAE costs have increased as a percentage of overall claim costs and should continue to do so with the change in coding of medical cost containment expenses as ALAE rather than medical.

Figure 5: Percentage of Medical-Only/Indemnity/ALAE Costs by Accident Year

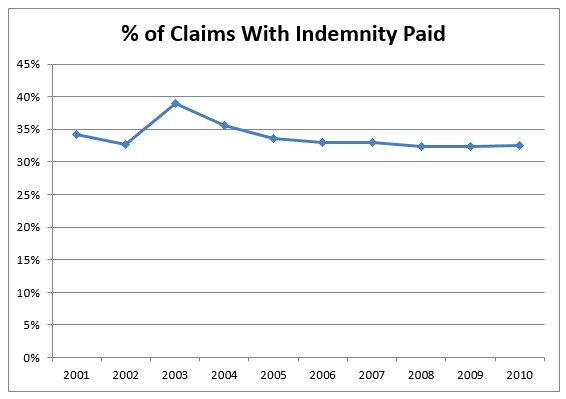

Approximately one-third of all claims reported eventually incur an indemnity payment. The remainder incur only medical and associated expenses and tend to be much less costly. The percentage of claims that incur an indemnity payment decreased soon after the 2003 reforms but has remained steady for the last eight years, as shown in Figure 6.

Figure 6: Percentage of Claims with Indemnity Paid

Specific areas

The exhibits in this section detail survey findings as they relate to trends in the specific areas of payroll, age, occupation, litigation status, cumulative trauma (CT), and future medical.

California hospital profiles

Figures 7 through 16 provide summaries of average wages, patient days, personnel, and medical staff characteristics across California hospitals. This information is based on data reported to OSHPD for all California hospitals.

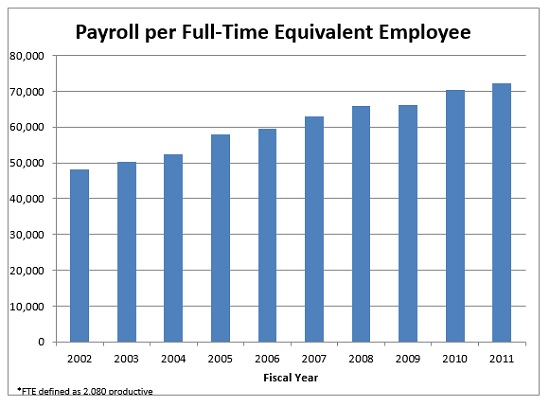

Figure 7 shows the general trend in payroll growth over the years 2002 to 2011. Though it has been slower at some points than others, such as during the years 2008 and 2009, the greater trend has been one of steady growth, nearly 50% over the entire period. Comparatively, average wages in California for all industries combined increased approximately 35% over this period3.

Figure 7: Payroll per Full-Time Equivalent Employee

The number of patient days in California hospitals has been steadily decreasing since 2007, consistent with a national trend of decreases or stagnant levels of inpatient care (combined with increases in outpatient care); however, California hospitals have reduced the number of staffed beds in their facilities by an even greater percentage. Figure 8 shows the combination of these trends, with the result being an increasing number of patient days per staffed bed.

Figure 8: Patient Days per Staffed Bed

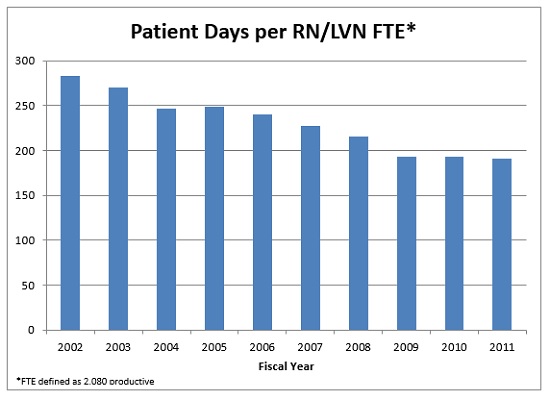

While the number of patient days and staffed beds has decreased, the number of Registered Nurses (RN) and Licensed Vocational Nurses (LVN)’s has increased over the 2002 through 2011 period, indicating that hospitals are focusing efforts on other aspects of care, perhaps associated with care delivery reforms. Figure 9 shows that patient days per hospital nursing staff was generally on a steady downward course for the period of 2002 to 2011.

Figure 9: Patient Days per RN/LVN FTE

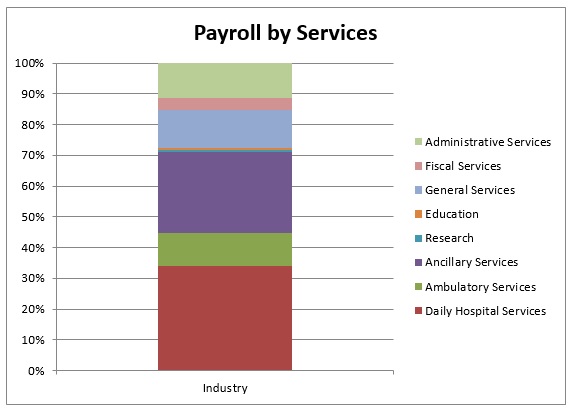

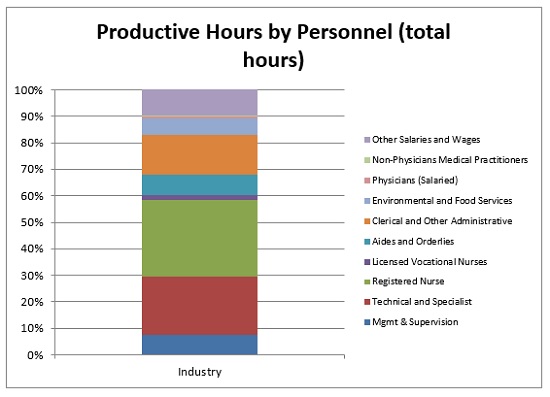

Figures 10 to 13 offer profiles of the patterns of payroll distribution, including by services, by productive hours (totaled up and also called out by both revenue-producing and nonrevenue-producing patient services).

Figure 10: Payroll by Services

Figure 11: Productive Hours by Personnel (total hours)

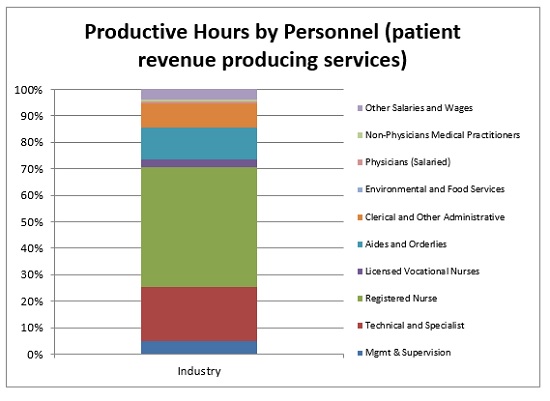

Figure 12: Productive Hours by Personnel (patient revenue-producing services)

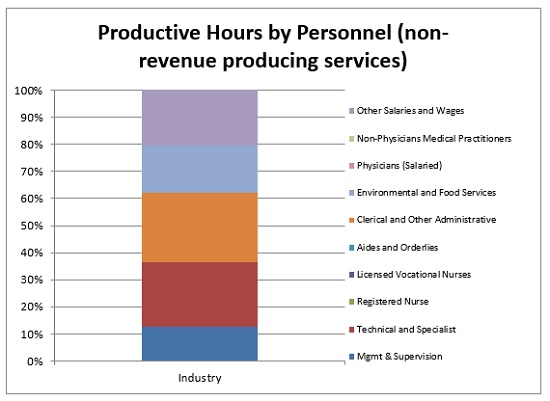

Figure 13: Productive Hours by Personnel (nonrevenue-producing services)

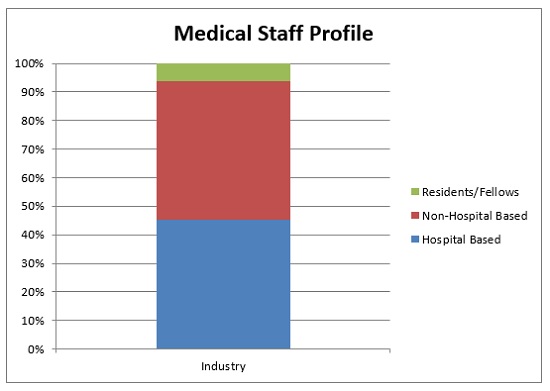

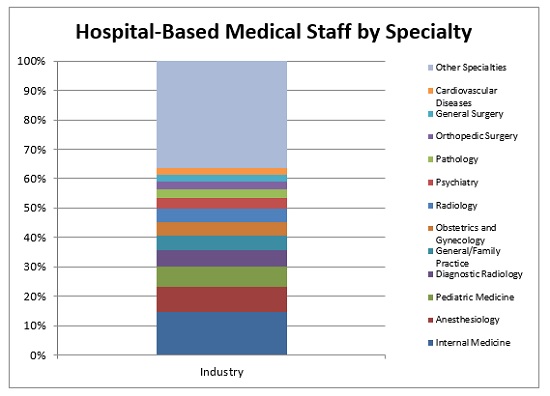

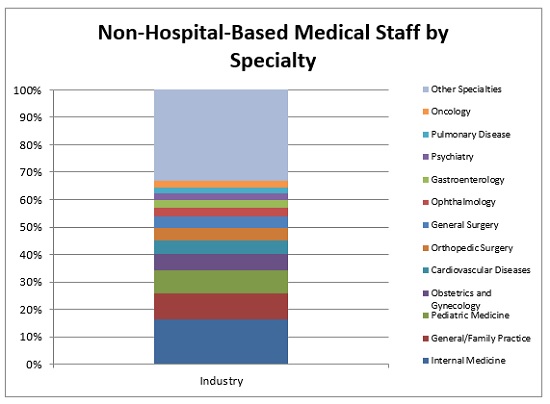

The remaining Figures 14 to 16 in this section show profiles of California hospital medical staff profiles, all totaled up and also broken out by hospital-based and nonhospital-based specialists.

Figure 14: Medical Staff Profile

Figure 15: Hospital-Based Medical Staff by Specialty

Figure 16: Non-Hospital-Based Medical Staff by Specialty

Age

This section offers charts illustrating results of benchmark participant claim experience in terms of age of claimant.

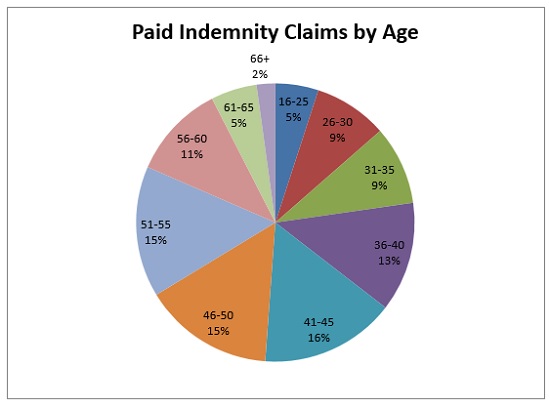

Figure 17 breaks out the entire population considered in this survey by age. Note that the largest segments, ages 36 to 55, account for well over half of the population considered.

Figure 17: Paid Indemnity Claims by Age

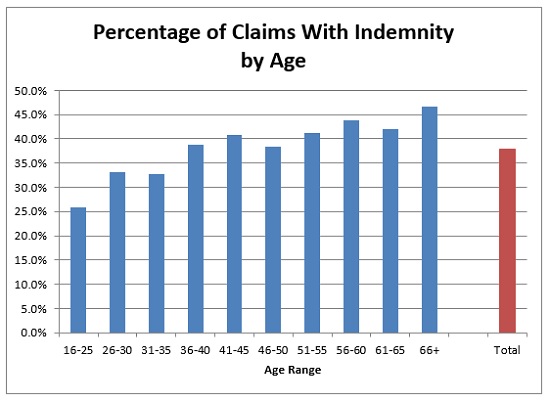

Figure 18 illustrates the likelihood that a claim resulting in an indemnity payment increases with the employee’s age.

Figure 18: Percentage of Claims with Indemnity by Age

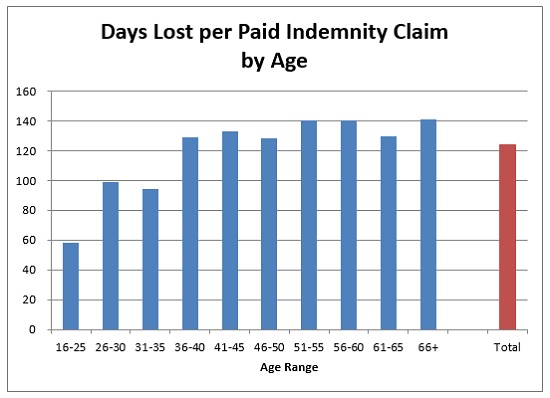

Similarly, the number of days lost when indemnity is paid on a claim also increases with the employee’s age, as shown in Figure 19. Those who are 16 to 25 years old incur less than two months average lost days and those who are 26 to 35 incur slightly more than three months, whereas 36-year-olds and older incur on average between four and five months of days lost.

Figure 19: Days Lost per Paid Indemnity Claim by Age

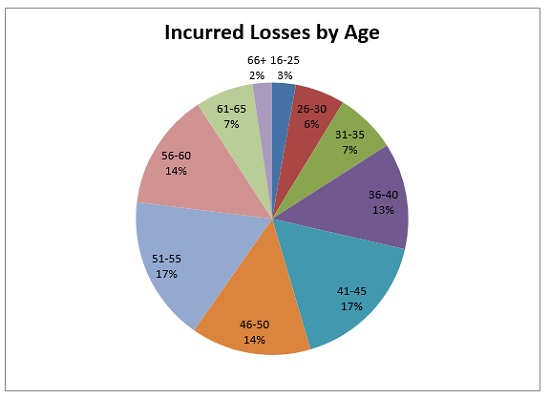

Figure 20 breaks out incurred losses by age. In many ways it shows a pattern very similar to that found in Figure 17 above, which broke out paid indemnity claims by age.

Figure 20: Incurred Losses by Age

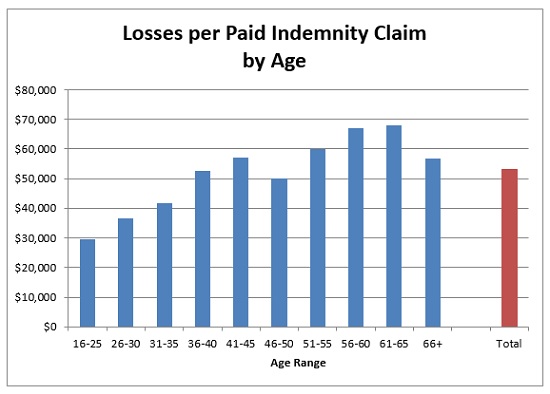

In Figure 21 it can be seen that, as with paid indemnity claims above, the loss severity per paid indemnity claim also increases with age, positively correlated with the average number of days lost per claim.

Figure 21: Losses per Paid Indemnity Claim by Age

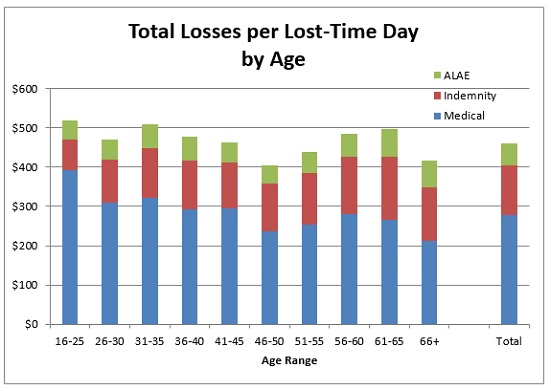

Figure 22 shows how medical losses per lost-time day tend to decrease as workers age (i.e., younger workers spend more in medical care per lost-time day than older workers). When combined with fewer lost-time days on average, this means that younger workers may be receiving more medical care in order to return to work faster.

Figure 22 also indicates that indemnity losses per lost-time day tend to increase as workers age (i.e., younger workers cost less in indemnity loss per lost-time day). This is likely related to lower wages for younger workers.

Figure 22: Total Losses per Lost-Time Day by Age

Occupation

This section offers charts illustrating results of benchmark participant claim experience in terms of occupation.

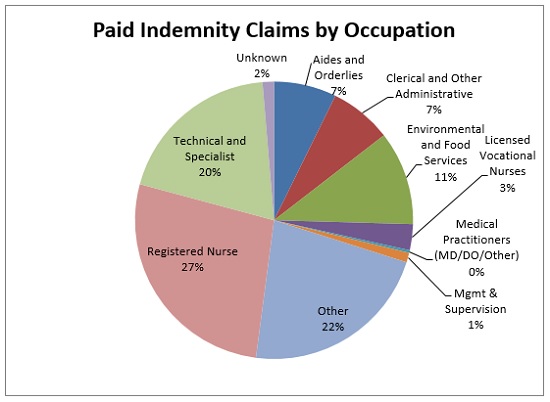

The pie chart in Figure 23 breaks out paid indemnity claims by occupation, showing that medical practitioners and management/supervision claims combined result in only 1% of the overall number of claims that incur an indemnity payment.

Figure 23: Paid Indemnity Claims by Occupation

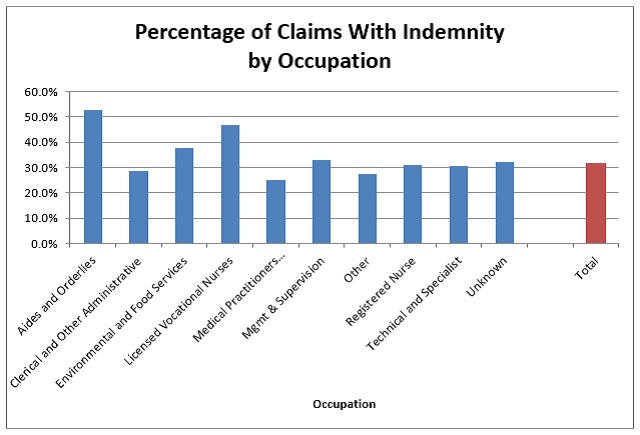

Claims by aides and orderlies claims are the most likely to incur an indemnity payment, as illustrated in Figure 24.

Figure 24: Percentage of Claims With Indemnity by Occupation

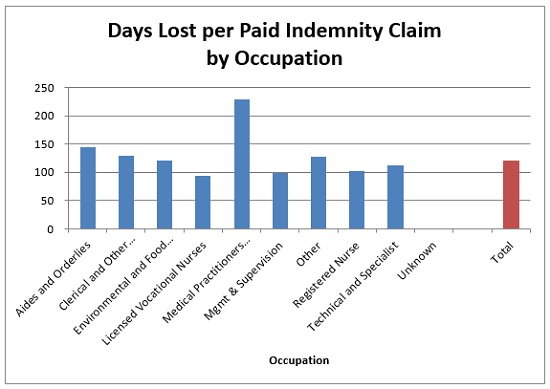

Figure 24 above shows that medical practitioner claims are the least likely to incur an indemnity payment, but Figure 25 shows that when they do they tend to result in by far the most lost-time days—nearly eight months average lost-time days versus four months overall average for all occupations.

Figure 24 above also shows that claims by aides and orderlies are most likely to incur an indemnity payment. According to the results illustrated in Figure 25, aides and orderlies also have the second-highest number of lost-time days.

Figure 25: Days Lost per Paid Indemnity Claim by Occupation

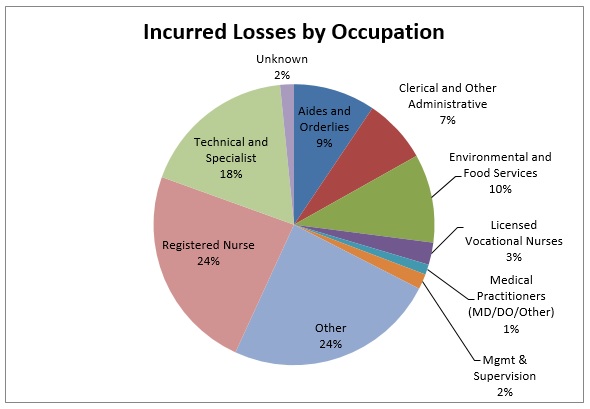

Similar patterns to those we have been looking at are found in incurred losses by occupation, which is broken out in Figure 26. Medical practitioners and management/supervision again account for relatively very small proportions of the total incurred losses.

Figure 26: Incurred Losses by Occupation

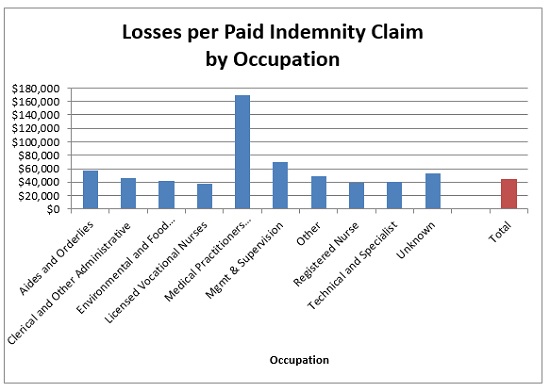

Figure 27 shows that, consistent with the largest number of days lost on average, medical practitioners have the largest severity per indemnity claim—nearly four times the overall average severity.

Aides and orderlies claims are the most likely to incur an indemnity payment (see Figure 24 above), and they also have the second-highest number of lost-time days (see Figure 25 above). As a result, their claims have the third-highest average losses per paid indemnity claim, behind medical practitioners and management/supervision. See Figure 27.

Figure 27: Losses per Paid Indemnity Claim by Occupation

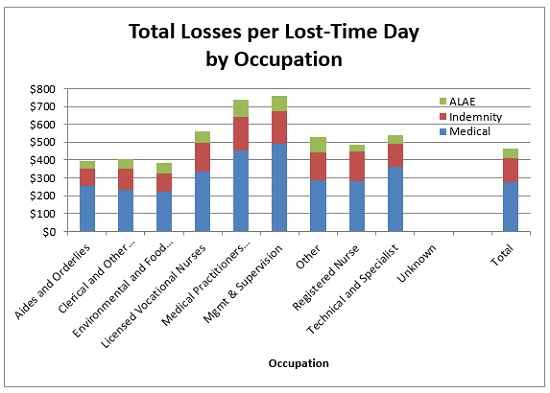

Medical practitioners and management/supervision claims incur by far the most in medical costs and indemnity benefits on a per lost-time day basis, as illustrated in Figure 28. However, these two occupations combined result in only 1% of the overall number of claims that incur an indemnity payment (see Figure 23 above).

Aides and orderlies have one of the lowest average losses per lost-time day, as also shown in Figure 28, so the high severity of their claims is a result of the number of days that are lost.

Figure 28: Total Losses per Lost-Time Day by Occupation

Litigation status

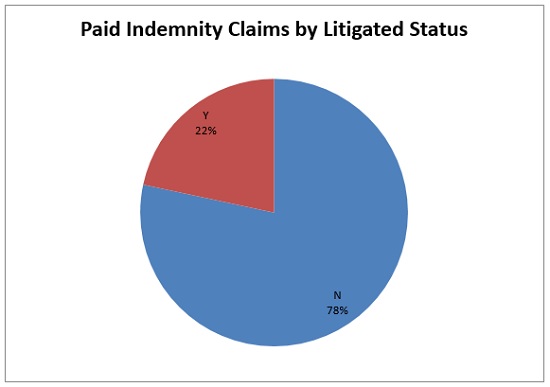

This section offers charts illustrating results of the survey in terms of litigation status. Figure 29 shows that between 20% and 25% of claims with paid indemnity are litigated.

Figure 29: Paid Indemnity Claims by Litigated Status

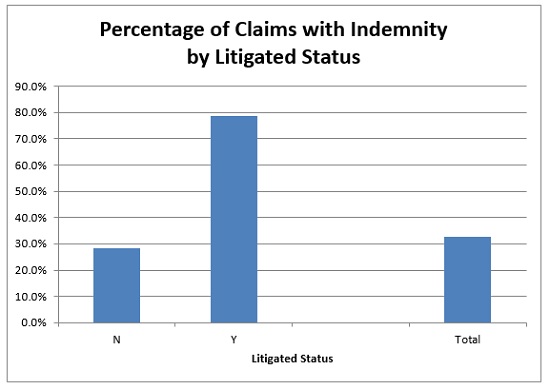

Between 20% and 25% of claims with paid indemnity are litigated, as shown in Figure 29 above. Of claims with litigation, Figure 30 illustrates that nearly 80% ultimately have paid indemnity—this compares with approximately one-third of all claims with paid indemnity.

Figure 30: Percentage of Claims with Indemnity by Litigated Status

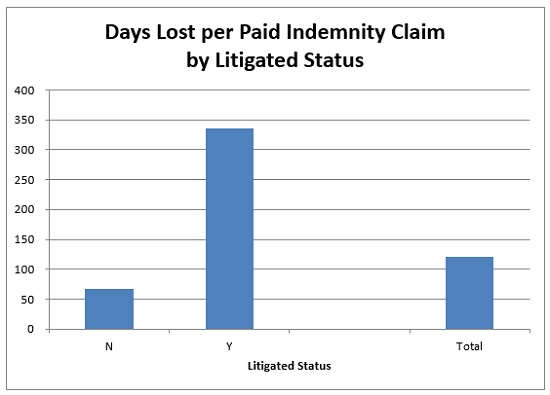

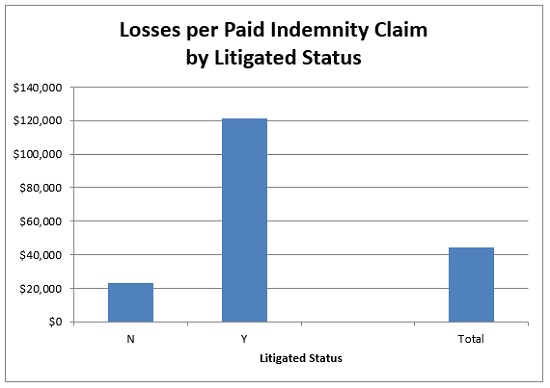

Litigated claims are significantly more costly, with an average severity nearly three times that of the overall claim (see Figure 33 below). This is directly related to the number of lost-time days, which averages about 11 months for a litigated claim versus four months overall average, as shown in Figure 31.

Figure 31: Days Lost per Paid Indemnity Claim by Litigated Status

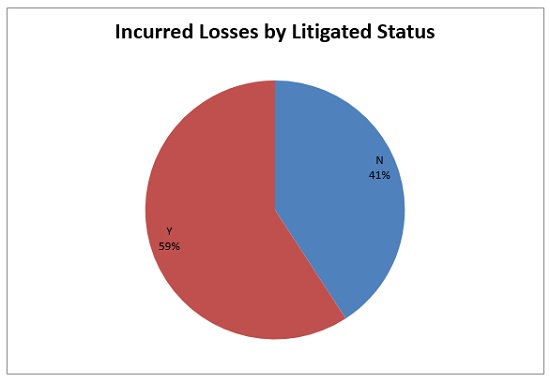

The pie chart in Figure 32 further indicates that litigated claims result in higher average losses, as 59% of total losses are related to the approximately 22% of claims that are litigated.

Figure 32: Incurred Losses by Litigated Status

Again, litigated claims are significantly more costly, with an average severity nearly three times that of the overall claim. See the stark results illustrating this in Figure 33.

Figure 33: Losses per Paid Indemnity Claim by Litigated Status

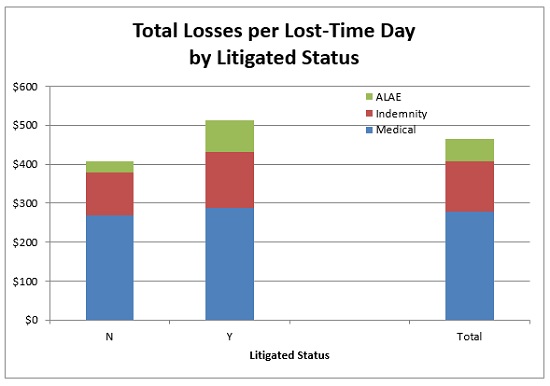

In terms of per lost-time day, litigated claims are also more costly, with more indemnity and significantly more ALAE spent on litigated claims per lost-time day, as shown in Figure 34. However, it's the sheer number of lost-time days on litigated claims that is the main driver of large severity.

Figure 34: Total Losses per Lost-Time Day by Litigated Status

Cumulative trauma (CT)

This section offers charts illustrating results of the survey in terms of cumulative trauma (CT) claims.

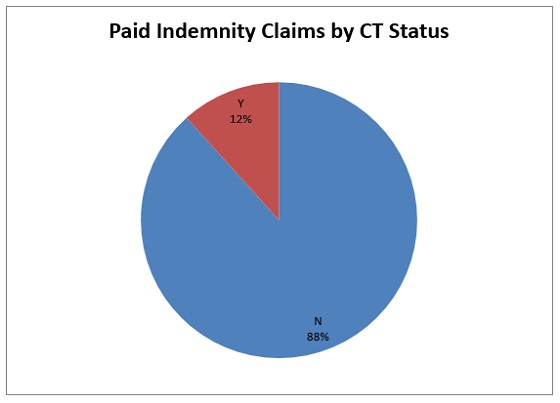

CT claims appear to make up about 10% to 15% of all claims with an indemnity payment, as shown in Figure 35, and this percentage appears to be on the rise, which is consistent with statistics published by the Workers’ Compensation Insurance Rating Bureau of California.

Figure 35: Paid Indemnity Claims by CT Status

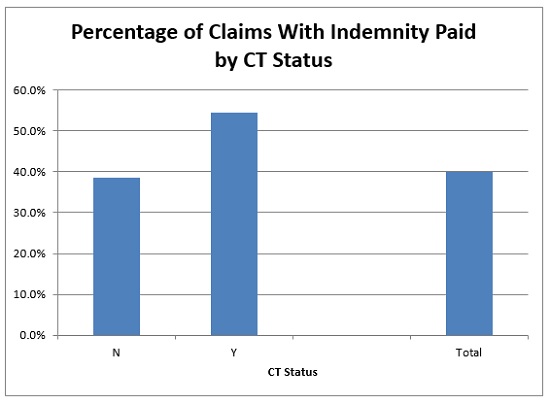

Figure 36 illustrates that claims with CT status are much more likely to result in an indemnity payment than other claims.

Figure 36: Percentage of Claims With Indemnity Paid by CT Status

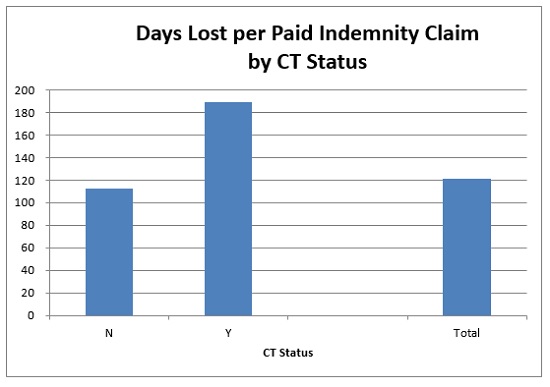

Figure 37 illustrates another impact of CT claims: they incur on average about six months of lost-time days versus three to four months for non-CT claims.

Figure 37: Days Lost per Paid Indemnity Claim by CT Status

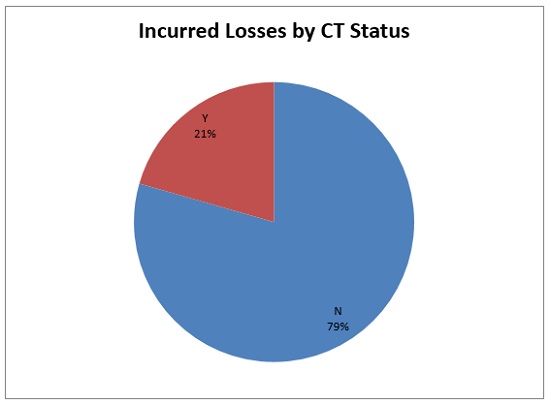

Figure 38 shows again that incurred losses involving CT status represents a relatively small minority, 21%, of the total incurred losses. However, this is compared to only 12% of overall claims involving CT evidencing the much greater severity of CT claims on average.

Figure 38: Incurred Losses by CT Status

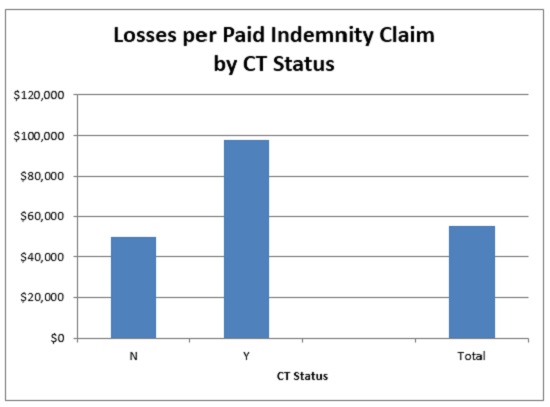

The average cost of a CT claim, however, is about twice that of a non-CT claim, as shown in Figure 39. This additional cost is directly related to the increased lost-time days related to these claims.

Figure 39: Losses per Paid Indemnity Claim by CT Status

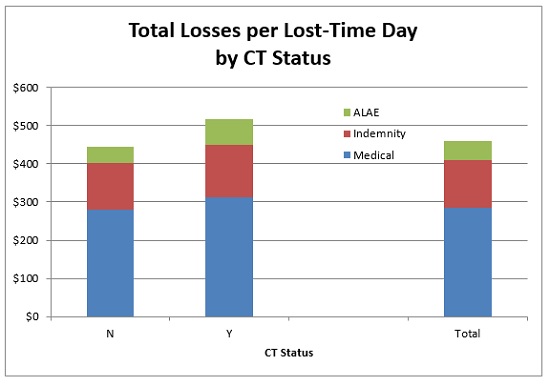

In terms of per lost-time day, CT claims are also more costly. However, it's the sheer number of lost-time days on CT claims that is the main driver of large severity.

Figure 40: Total Losses per Lost-Time Day by CT Status

Future medical (FM)

This section offers charts illustrating results of the survey in terms of future medical (FM) claims.

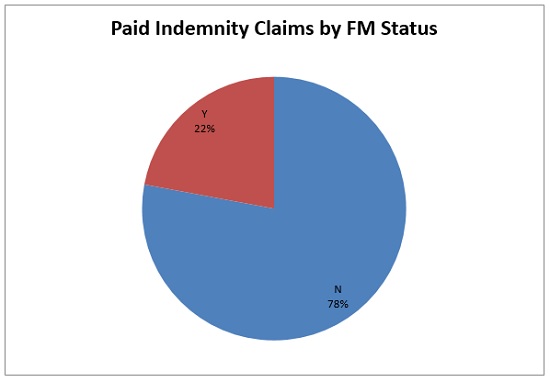

Figure 41 shows that between 20% and 25% of claims with paid indemnity are coded as future medical—that is, indemnity benefits are finished but the claim remains open for continuing medical care.

Figure 41: Paid Indemnity Claims by FM Status

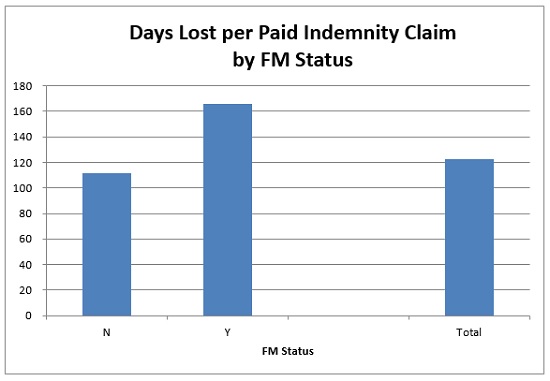

Figure 43 indicates that FM claims on average result in many more weeks of days lost on average.

Figure 43: Days Lost per Paid Indemnity Claim by FM Status

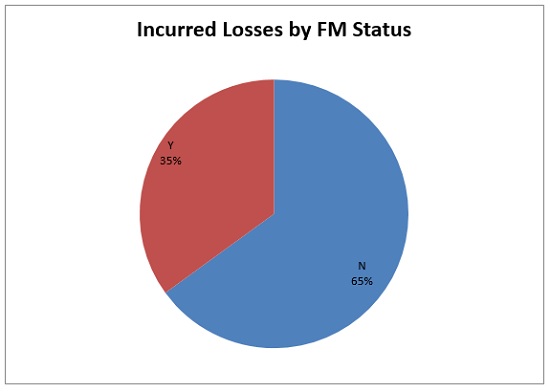

FM claims account for a little more than a third of incurred losses, or 35%, as shown in Figure 44.

Figure 44: Incurred Losses by FM Status

Even though FM claims represent little more than a third of incurred losses, the costs per paid indemnity claims are nearly twice that of the non-FM claims.

Figure 45: Losses per Paid Indemnity Claim by FM Status

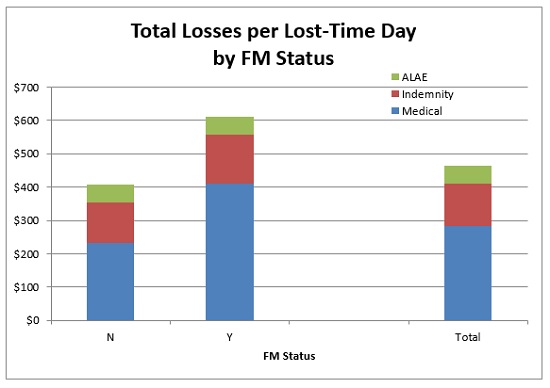

On a per lost-time day basis, as illustrated in Figure 46, the medical losses on FM claims are twice that of non-FM claims, and about equal to the other loss components (indemnity and ALAE) on non-FM claims.

Figure 46: Total Losses per Lost-Time Day by FM Status

Sources

Overall Charts

Figure 1: Milliman estimates from benchmark participant claim experience and payroll as reported to the California Office of Statewide Health Planning and Development (OSHPD).

Figure 2: Milliman estimates from benchmark participant claim experience and payroll as reported to OSHPD.

Figure 3: Milliman estimates from benchmark participant claim experience and payroll or full-time employee (FTE) as reported to OSHPD.

Figure 4: Milliman estimates from benchmark participant claim experience and FTE as reported to OSHPD.

Figure 5: Benchmark participant claim experience.

Figure 6: Benchmark participant claim experience.

Payroll and utilization charts

All data as reported to OSHPD for all California hospitals.

Age, occupation, litigation status, cumulative trauma (CT), and future medical (FM) charts

All data based on benchmark participant claim experience.

Footnotes

1It is important to note that OSHPD payroll only includes payroll under the hospital name; it does not include payroll of clinics, home health, or other associated entities and services. Therefore, loss costs described here and elsewhere in this report will be overstated relative to loss costs that include those payroll sources, and should only be considered valid for benchmarks within the context of this report.

2Please note that the definition of a “lost-time” claim can differ by third-party administrator (TPA) and facility. In order to be more consistent within this analysis, we have used an indemnity claim definition based on whether paid indemnity is greater than zero. This definition is typically more stringent than the definition of a lost-time claim used by most TPAs or facilities and results in fewer claims used in frequency statistics.

3Based on Workers Compensation Insurance Rating Bureau of California (WCIRB) Governing Committee Agenda dated September 11, 2013, Exhibit 5.1.