This article was originally published in October 2014. It was updated in January 2017 to reflect nomenclature change. Thanks go to Jessica Gardner, Scott Preppernau, and Frank Thoen for these updates.

Variable annuity plan (VAP) design is compelling. It provides participants with a lifelong income that offers potential inflation protection while providing employers with contribution and balance sheet stability. A VAP stays well-funded regardless of asset performance or interest rate changes. The biggest drawback is that retirement benefits are volatile, sometimes changing substantially from year to year.

An Internal Revenue Service (IRS) Revenue Ruling in 1953 made it clear that the variable annuity plan (VAP) is an allowable qualified plan design. There are VAPs operating now, but there used to be more. Anecdotal information, based on informal conversations with professionals who worked with these plans, suggests that the plan design declined in part because of participant dissatisfaction with benefit volatility.

Among today’s plan sponsors who are interested in implementing VAPs, retiree benefit volatility remains a major concern. There has been a great deal of activity in the actuarial community in the past couple of years to find viable modifications to the VAP that will increase benefit stability. Final hybrid plan regulations issued September 19, 2014, have provided for automatic approval for a number of these modifications.

Benefit volatility reduction strategies

Conservative asset allocation

Because the benefit volatility in a VAP results from investment volatility, adjusting a plan’s investment mix to be less volatile will create more stable VAP benefits. Consider a plan that has an asset allocation of 70% in large company stocks (S&P 500) and 30% in long-term high-grade corporate bonds. Because stocks have greater volatility than bonds, VAP benefit volatility could be reduced by decreasing the stock allocation and increasing the bond allocation. Increased allocations to bonds would not eliminate benefit declines, but would reduce their expected frequency and severity.

A more conservative asset allocation is expected to produce smaller returns over time. Smaller returns produce fewer assets over the life of the plan, which results in smaller retirement benefits being provided to participants for each dollar of contribution. Additionally, the lower expected returns result in less expected inflation protection.

So while shifting a plan’s asset allocation to more conservative investments would be expected to lead to less volatile VAP benefits, it would also be expected to provide smaller benefits and less inflation protection than could otherwise be provided.

Minimum or floor benefit

What would happen if a VAP provided a floor benefit?

This sounds reassuring when faced with volatile benefits. However, the largest benefit declines during the past 90 years would have been 50% from 1929 to 1933, 33% from 1973 to 1975, 20% from 2000 to 2003, and 25% from 2008 to 2009. If a floor benefit is to provide meaningful protection, it would need to be fairly large compared to the VAP benefit.

A small floor benefit would be too small to provide meaningful benefit security and concerns about retiree benefit volatility would remain. With larger floor benefits, a significant asset decline could leave the floor benefit underfunded, which would increase the cost of the plan, at least in the short term.

Additionally, it is difficult to accurately determine the liability associated with a floor benefit that may or may not get paid. As a result, a meaningful floor benefit introduces potential volatility to a plan sponsor’s contribution and accounting requirements, which is counter to one of the primary objectives of the VAP design.

Level retiree benefits

Because plan sponsors are concerned about benefit volatility for participants in pay status, one potential stabilization method is simply to fix benefits in retirement, making them constant.

In a modified VAP that fixes retiree benefits, the benefits for active participants and terminated vested participants fluctuate over time as in the basic VAP, but when a participant retires, the benefit is fixed at its current level for life. This eliminates retiree benefit volatility but also eliminates potential inflation protection in retirement, one of the key benefits of a VAP.

To minimize funding volatility due to investment returns, retiree benefits would typically be immunized (funded by matching expected payments with bonds) or annuitized, which subjects the plan to interest rate risk. In addition, bonds have lower expected returns than stocks, so over the life of the plan, there would be lower expected benefits paid per dollar of contribution.

Another issue with this strategy is that plan participants will time their retirements with up markets, locking-in higher benefits. This retirement behavior will increase plan costs and make workforce management difficult, as employees will delay retirement during down markets or retire all at once after a market run-up. Participants who cannot or do not time their retirement correctly may retire right after a market downturn, thus locking in losses for life.

Providing level benefits to retirees addresses the primary concern with VAPs. Unfortunately, this strategy introduces plan sponsors to workforce management issues and funding volatility, while participants lose inflation protection and risk locking in investment losses for life if they retire after a market downturn.

Milliman Sustainable Income Plans™ (SIPs)

Each of the above strategies provides more benefit certainty in retirement than a basic VAP, but comes at the price of reducing or eliminating some of the positive features that make VAPs appealing in the first place. Milliman Sustainable Income Plans™ (SIPs) provide a viable alternative to the strategies above. SIPs offer all the positive features of a basic VAP and virtually eliminate the possibility of retiree benefit declines. SIP design includes a three-part strategy:

1. Build a reserve.

2. Spend the reserve in down markets to prevent benefit decreases.

3. Improving benefits if the reserve is larger than is required to prevent benefit decreases.

The SIP design is allowable under the final hybrid plan regulations.

1. Build a reserve

The central strategy feature of SIPs is creating a “stabilization reserve” (i.e., a funding surplus) that can be used to shore-up benefits following market downturns (preventing benefit decreases). There are several reasonable reserve building strategies.

Contribute reserving margin. The employer could contribute more than the value of annual benefit accruals to build the reserve. This strategy builds reserves consistently and “seeds” the reserve in early years.

Cap benefit increases. SIP benefit increases are capped at a certain maximum increase per year, say 10%. Whenever the plan’s investment return would produce benefit increases greater than 10%, the excess return builds the reserve. This method will not build a reserve on a regular basis, but it will build a reserve at any maturity level and is not likely to require additional employer contributions.

Use a portion of the return directly above the hurdle rate. Instead of building reserves using returns above a cap, reserves could be built with a portion of the return directly above the hurdle rate. For example, if the hurdle rate is 4%, benefit increases would not be earned on the portion of the return between 4% and 5%. Benefit increases would only be provided when asset returns exceed 5%. This method will build a reserve more consistently than capping and works at all levels of plan maturity. However, it decreases the inflation protection provided to participants, as the threshold for an increase in benefits is raised.

2. Spend the reserve in down markets to shore-up benefits

When benefits would otherwise decrease, the reserve is used to prevent or mitigate benefit reductions. The intent is to protect each retiree’s high-water mark (i.e., the highest level of monthly benefit received in retirement) to the greatest extent possible.

For example, if a retiree’s underlying SIP benefit decreases from $1,000 to $900 per month based on the prior year’s return, the stabilization reserve would provide $100 a month to shore up the benefit, maintaining a total benefit of $1,000 per month. The next year, the underlying SIP benefit of $900 per month will be adjusted based on the plan’s investment return. If the underlying benefit exceeds the prior high-water mark of $1,000 per month, the underlying benefit is paid (this becomes the new high-water mark) and no payment is made from the reserve. However, if the underlying benefit is still less than the prior high-water mark, a portion would again be paid from the reserve.

If the reserve runs out, then the underlying SIP benefit is paid. In this case, the benefit paid will remain below the high-water mark until the market recovers or until there are again sufficient reserves in the plan to shore up the benefit. By only shoring up benefits when reserves are available, the plan does not become underfunded.

In practice, a relatively small margin is sufficient to shore up benefits to the retiree’s high-water mark, except in extreme markets. This is because the shore-up is not an ongoing promised benefit, but rather a temporary benefit equal to a fraction of one year’s worth of benefit payments. For most plans, this represents a relatively small portion of the total plan liability.

3. Provide benefit “bumps” if the reserve is larger than is required to prevent benefit decreases

There may be circumstances when the stabilization reserve gets much larger than needed to reasonably protect the high-water mark for all benefits. When this occurs, the benefits of all participants could be increased to spend down the excess reserve. Alternatively, this excess could be used to provide a short-term contribution holiday for the employer. However, under no circumstances should the plan be allowed to get underfunded. For details, see SIPs: Predictable Contributions and Accounting.

SIP example: Retiree benefit examples

As an illustration of how a SIP could work, consider a 2% career average SIP with a 4% hurdle rate. To stabilize benefits a three-part reserve strategy is employed.

1. To build a reserve, returns are capped in years with returns greater than 14.4% (limiting benefit increases to 10% annually).

2. The reserve is spent in down markets to shore up retiree benefits.

3. Whenever the plan’s funded percentage goes over 125%, benefits for all participants are increased so that the plan is 125% funded after the increase. The plan begins the period at 105% funded.

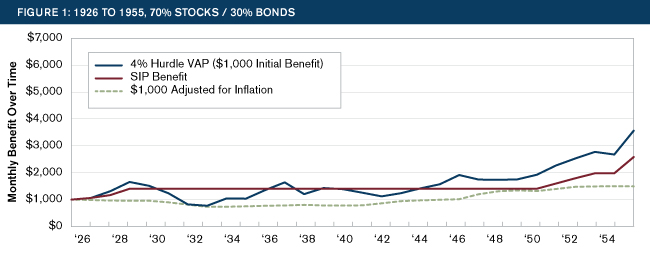

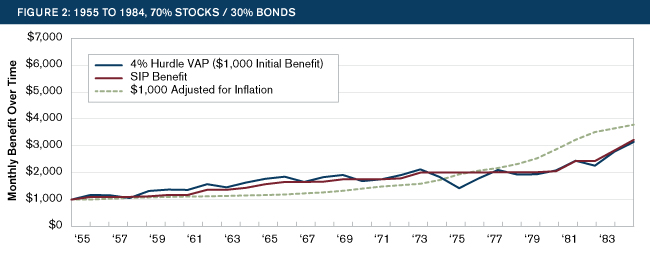

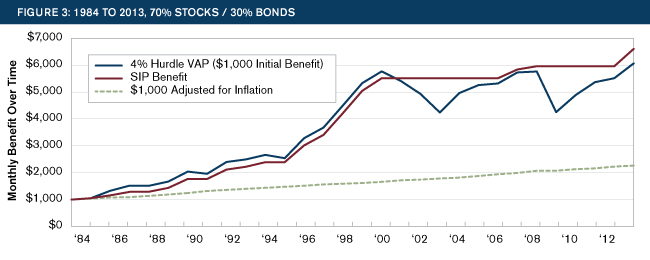

Figures 1 through 3 show how a retiree’s SIP benefit would have changed over different historical periods, 1926 to 1955 (Figure 1), 1955 to 1984 (Figure 2), and 1984 to 2013 (Figure 3). Each period shows a retiree with a starting retirement benefit of $1,000 for a plan invested 70% in large company stocks (S&P 500) and 30% in long-term high-grade corporate bonds. The blue and red lines both show VAP and SIP benefits. The blue line shows a VAP benefit, where benefits move up and down with the plan’s actual investment returns. The red line shows the SIP benefit. The green dotted line shows a $1,000 monthly benefit adjusted for inflation, which is the benefit that would maintain the retiree’s purchasing power over the period.

The general result is that the SIP benefits (red line) typically have smaller increases than the VAP benefits (blue lines), but there are also no benefit decreases in any of the three historical periods tested. This is the trade-off in the SIP. Large benefit increases (those over 10% in this example) are capped so that the high-water mark benefit can be shored up as needed.

Figure 1 shows that, over the 29-year period from 1926 to 1955, the VAP benefit (blue line) consistently provides good inflation protection to retirees, but it comes at a cost. The benefit is very volatile, increasing from $1,000 to over $1,500 by 1929, only to dip below the original $1,000 before providing a bumpy recovery.

By contrast, the red line shows the SIP benefit. The benefit increases are much smaller in the first few years because the annual returns larger than 14.4% did not increase benefits, but instead built the stabilization reserve. The reserve that is built is sufficient to shore up benefits through the entire Great Depression, without a benefit decrease, and the SIP benefit still outpaces inflation over the period, though the benefit increases are not as large as with the VAP. The SIP benefit remains constant from 1928 through 1950, a very long period without any benefit increases. That period also had very low inflation, so the purchasing power of the benefit remains intact.

Figure 2 shows that, over the 29-year period from 1955 to 1984, the VAP benefit (blue line) and the SIP benefit (red line) move together over the period. The VAP benefit increases and decreases while the SIP essentially cuts the tops off of the high return years and fills in the low years, providing a benefit that goes up over time, but does not decrease.

Figure 3 shows that, over the 29-year period from 1984 to 2013, the VAP benefit (blue line) increases more quickly than the SIP benefit (red line). Over this period there were many years with returns above the cap. Ultimately, the SIP benefits were increased by spending excess reserve in addition to the increases that were due to returns.

There are two very dramatic benefit declines in this period, one after the dot-com bubble in the early 2000s and one after the housing crisis in 2008. The reserves built in the 1990s were more than sufficient to shore up benefits in both of these markets. In fact, the plan spent reserve to increase benefits because it was over 125% funded through most of the period, resulting in benefit increases above the VAP benefit by the end of the period.

SIP strengths

SIPs retain basic VAP strengths. A SIP provides all of the benefits of a basic VAP:

- Well-funded plan

- Funding and accounting stability

- Predictable employer costs

- Expected inflation protection

- “Portable” benefits

- Lifelong income

- Longevity pooling

- Professional asset management

SIPs can virtually eliminate benefit decreases. Through utilization of a benefit stabilization reserve, a SIP can effectively prevent retiree benefits from declining.

SIP weaknesses

SIPs do not increase as fast in rising markets. During rising markets, benefits in a SIP will lag those of a basic VAP.

SIPs cannot guarantee benefits do not decrease in retirement. While the chances of retiree benefit reductions are very unlikely under a SIP, they are not completely eliminated. Retirees could still see their benefits decrease if the stabilization reserve is completely depleted.

Conclusion

SIPs offer all of the sponsor and participant benefits of the basic VAP design while at the same time virtually eliminating the chances that retirees will ever have their benefits decrease. This design is simple, sustainable, and will provide generations of participants with secure retirement.

Appendix 1: Benefit stabilization reserve method: Active SIP benefit example

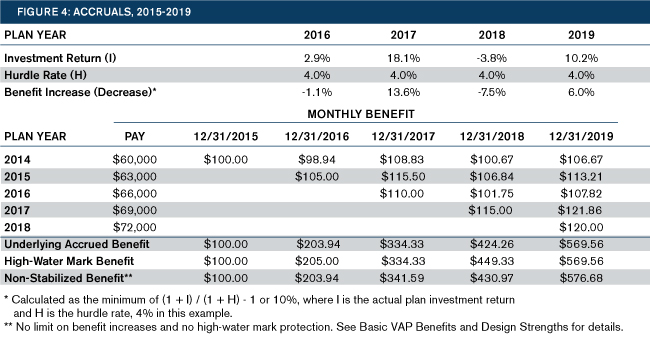

Figure 4 shows the active benefit example from Basic VAP Benefits and Design Strengths modified to provide a SIP benefit using a cap to build reserves. In this example, the company has a SIP with a hurdle rate of 4%, a 2% career average benefit, and a benefit increase cap of 10%. Suppose the company hires a new participant in 2015 who earns $60,000 in 2015 and gets pay raises of $3,000 per year thereafter.

The 2015 accrual for this participant is $2% x $60,000 / 12 = $100.00 per month. The 2016 accrual for this participant is $2% x $63,000 / 12 = $105.00 per month. This is the same as any other career average plan. Accruals for 2015 through 2019 are shown in the table in Figure 4, which also shows what happens to these accruals in the years after they are earned.

As with a VAP, the accrual for each year is adjusted in later years based on the plan’s investment return. There are, however, two key differences from the VAP example. In a SIP, the benefit payable to a participant who retires is the high-water mark benefit (subject to reserve availability). At the end of 2016 and 2018, the high-water mark benefit applies because the underlying benefit has declined below that level. Additionally, to build the reserve, benefit increases are limited to 10% in years where investment returns are greater than 14.4%. In the example above, the benefit increase is limited to 10% at the end of 2017. Without the cap, the benefit increase would have been 13.6%.

The last line of the table in Figure 4 shows what the benefit would have been under a VAP. This benefit is not part of the SIP, but is shown for comparison purposes to illustrate the trade-off between the stabilization features in a SIP design, which protect the benefit from declining, and the VAP design, which provides higher peak benefits. Over time, both designs are expected to pay out the same value of benefits, but the SIP will provide a smoother ride to participants.

For details on how funding and accounting consistency are achieved, please read SIPs: Predictable Contributions and Accounting.

For information on transitioning to a SIP see Transition to a SIP Design.