This article was originally published in October 2014. It was updated in January 2017 to reflect nomenclature change. Thanks go to Jessica Gardner, Scott Preppernau, and Frank Thoen for these updates.

The retirement crisis

Traditional defined benefit (DB) plans are less plentiful than they once were, and defined contribution (DC) plans have been tested by several major market events in recent years. And yet sustainable, secure retirement income is still a pressing need for many Americans.

DB plans provide retirees with a secure, stable stream of income for life. However, that stability comes at a high price for employers. They face substantial contribution (funding) and balance sheet (accounting) volatility. This has resulted in many DB plan freezes and terminations over the past 40 years. In many cases, DB plans are replaced with DC plans.

DC plans such as the 401(k) work very well for employers, providing predictable contributions, year after year. However, as a sole form of retirement income, they do not provide participants with the same level of security as DB plans. Participants face the risk of outliving their assets because DC plans generally do not provide the guarantee of lifelong income. Additionally, they do not provide as much benefit per dollar of contribution, which is due to lack of professional asset management, individuals’ longevity concerns, and significant leakage.

Milliman Sustainable Income Plans™ (SIPs) have controllable employer costs, like DC plans, and provide participants with lifelong income, like DB plans, while providing inflation protection over time.

Basic VAP design

A variable annuity plan (VAP) is a retirement plan where the benefits adjust each year based on the return of the plan’s assets, resulting in stable plan funding requirements. Although VAPs have been allowed under Internal Revenue Service (IRS) rules for a long time (see Revenue Ruling 185, 1953-2), they are not common. Benefits are typically earned on career average or flat-dollar types of accumulation.

One central feature of a VAP is the “hurdle rate,” which is usually set between 3% and 5%. If the plan’s investment returns equal the hurdle rate, the plan functions exactly like a traditional DB plan. However, when the plan’s investments return more (or less) than the hurdle rate, benefits increase (or decrease) by the difference between the actual return and the hurdle rate. These benefit increases and decreases apply equally to all participants’ benefits, whether active, retired, or terminated vested. This means that, in a basic VAP, retirees will experience decreases in their benefits in some years.

Example

Suppose a company with a VAP that has a hurdle rate of 4% and a 2% career average benefit hires a new participant in 2015 who earns $60,000 in 2015 and gets pay raises of $3,000 per year thereafter.

The 2015 accrual for this participant is $2% x $60,000 / 12 = $100.00 per month. The 2016 accrual for this participant is $2% x $63,000 / 12 = $105.00 per month. This is the same as any other career average plan. Accruals for 2015 through 2019 are shown in the table in Figure 1, which also shows what happens to them in the years after they are earned.

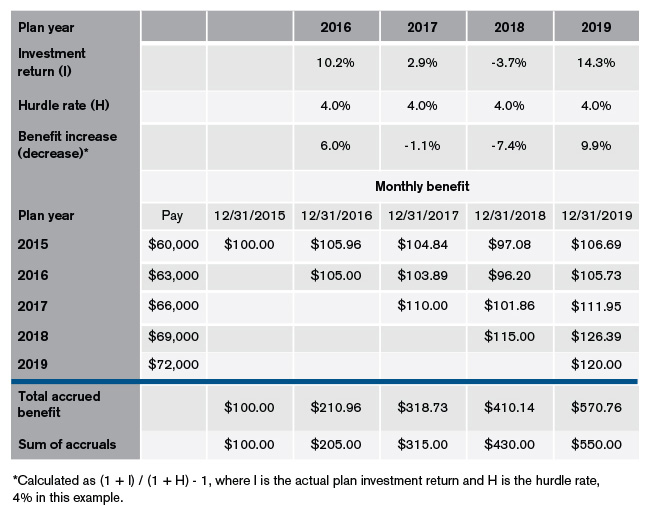

Figure 1: SIP accruals

In 2015, the participant accrues a benefit of $100.00. In 2016, the plan assets returned 10.2%. The VAP defines annual benefit adjustments as (100% + actual return) / (100% + hurdle rate) – 100%, so the 10.2% return results in an increase of 5.96% (110.2% / 104% - 100%) to all previously accrued benefits. As a result, the participant’s $100.00 benefit accrued during 2015 increases to $105.96 as of December 31, 2016. The participant also earned a new benefit accrual of $105.00 during 2016, so at the end of the year the total benefit is $210.96 ($105.96 + $105.00).

In 2017, the plan’s investment return was 2.9%. Although this return is positive, it is less than the hurdle rate of 4% and results in benefits earned prior to 2017 decreasing by 1.1%. The accrual from 2015 adjusts from $105.96 to $104.84, the accrual from 2016 adjusts from $105.00 to $103.89, and a new accrual of $110.00 is earned, for a total accrued benefit of $318.73 as of December 31, 2017.

A year-by-year comparison of the sum of the original accruals to the current value of the total accrued VAP benefit appears at the bottom of Figure 1. As of December 31, 2018, after a poor return year, the VAP benefit is less than the sum of the original accruals. However, by December 31, 2019, the VAP benefit is $570.76 compared to the sum of the accruals of $550.00.

At retirement, the benefit can be elected in a form that covers the participant’s lifetime only, such as a single life annuity, or the participant’s and spouse’s lifetime, such as a joint and survivor annuity, just like in a traditional defined benefit plan.

The benefit adjustments described in Figure 1 also apply to retiree benefits. As an example, consider a retiree who receives $100 per month beginning December 31, 2015. That person would receive $100 per month during 2016. Because the plan assets returned 10.2% during 2016, the retiree would receive $105.96 per month during 2017. The benefit would continue to adjust just as the active benefit does, but no new accruals would be added.

Though volatile, benefits earned under a VAP are expected to increase over time if the long-term expected return on the plan’s investment portfolio is greater than the hurdle rate. This is expected to provide inflation protection, both while active and in retirement. In addition, the funding requirements of the plan remain stable, even with a market downturn. The contribution requirement each year is the value of benefits accruing for the year, much like a defined contribution plan, without any surprises. Because benefits adjust to reflect the plan’s investment performance, the plan’s assets and liabilities remain in balance at all times. Therefore, VAPs will not have unfunded past benefits that need to be “re-funded.”

Anecdotal information, based on informal conversations with professionals who worked with these plans, suggests that participant dissatisfaction with benefit volatility was one of the reasons for diminished popularity of these plans. Among today’s plan sponsors who are interested in implementing VAPs, retiree benefit volatility remains a major concern. There has been a great deal of activity in the actuarial community in the past couple of years to find viable modifications to the basic VAP that will increase benefit stability without significantly increasing cost or sponsor risk. One such method, the SIP, is described below.

The SIP

There is a benefit stabilization strategy that is able to offer all the features of a basic SIP and practically eliminate benefit declines. A stabilization reserve is built to keep benefits level during down markets. We call it the cap and shore-up method:

Build a stabilization reserve (by capping benefit increases in high return years).

A stabilization reserve could be developed in several ways. Two possibilities are described below:

- Limit SIP benefit increases to a certain maximum increase per year, say 10%. When the plan’s investment return would result in benefit adjustments greater than 10%, benefits would only increase by 10% and the excess return would be used to build a reserve.

- Build the reserve with a portion of the return directly above the hurdle rate. For example, if the hurdle rate is 4%, do not provide benefit increases on the portion of the return between 4% and 5%. Benefits would only increase when returns are greater than 5%.

Spend the reserve in down markets to prevent benefit decreases (shoring-up benefits).

When benefits would otherwise decrease, use a portion of the stabilization reserve to prevent benefit reductions. The intent is to protect each retiree’s high-water mark (i.e., the highest level of monthly benefit received in retirement) to the greatest extent possible.

For example, if a retiree’s underlying SIP benefit decreases from $1,000 to $900 per month, the stabilization reserve would provide $100 a month to shore up the benefit, maintaining a total benefit of $1,000 per month. The retiree has not had his benefit payment decrease.

The next year, the underlying SIP benefit of $900 per month will be adjusted based on the plan’s investment return. If the underlying benefit exceeds the prior high-water mark of $1,000 per month, the underlying benefit is paid (this becomes the new high-water mark) and no payment is made from the reserve. However, if the underlying benefit is still less than the prior high-water mark, a portion would again be paid from the reserve.

In the event that the reserve runs out, then the underlying SIP benefit is paid. In this case, the benefit paid will remain below the high-water mark until the market recovers or until there are again sufficient reserves in the plan to shore up the benefit. By only shoring up benefits when there is reserve available, the plan does not become underfunded.

In practice, a relatively small margin is sufficient to shore up benefits to the retiree’s high-water mark, except in extreme markets. This is because the shore-up is not an ongoing promised benefit, but rather a temporary benefit equal to a fraction of one year’s worth of benefit payments. For most plans, this represents a relatively small portion of the total plan liability.

Improve benefits if the reserve is larger than is required to prevent benefit decreases.

There are circumstances when the stabilization reserve gets much larger than needed to reasonably protect the high-water mark for all benefits. When this is the case, the benefits of all participants could be increased to spend down the excess reserve. Alternatively, this excess could be used to provide a short-term contribution holiday for the employer. However, under no circumstances should the plan be allowed to get underfunded.

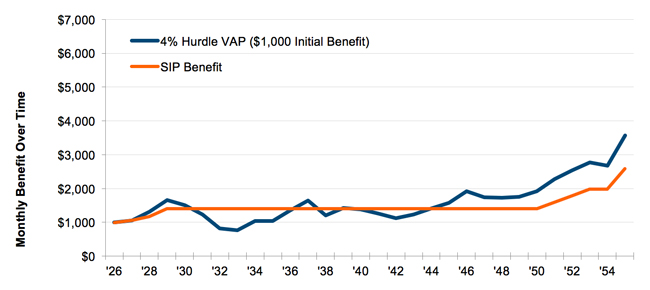

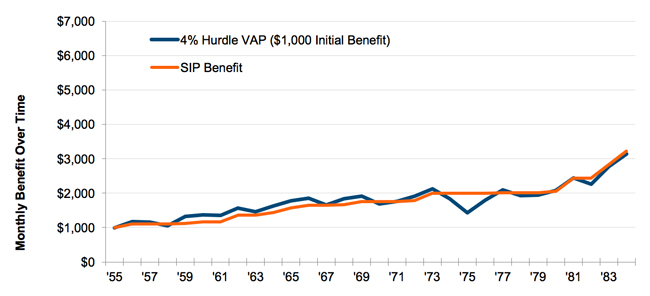

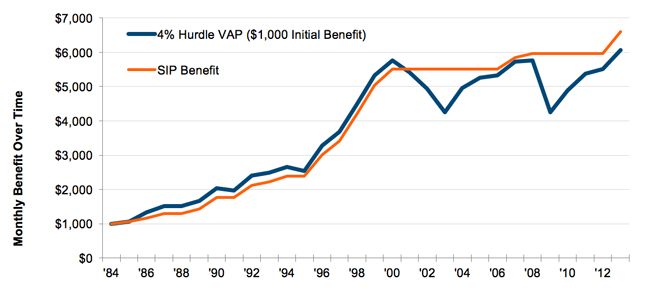

The graphs in Figures 2 to 4 illustrate how a retiree’s basic VAP and SIPbenefit would have changed over different historical periods, 1926 to 1955 (Figure 2), 1955 to 1984 (Figure 3) and 1984 to 2013 (Figure 4). Each period shows a retiree with a starting retirement benefit of $1,000 for a plan with a 4% hurdle rate invested 70% in large company stocks (S&P 500) and 30% in long-term high-grade corporate bonds. The blue line shows a basic VAP benefit, where benefits move up and down with the plan’s actual investment returns. The orange line shows a SIP benefit, where:

- To build a reserve, benefit increases are limited to 10% annually.

- The reserve is spent in down markets to prevent benefit declines for retirees.

- Whenever the plan’s funded percentage goes over 125%, benefits for all participants are increased so that the plan is 125% funded after the increase. For these examples, it is assumed that the plan begins the period at 105% funded.

The general result is that the SIP benefits (orange lines) typically increase less than the basic VAP benefits (blue lines), as returns are capped in high return years. There are also no benefit decreases in any of the three historical periods tested. This is the tradeoff in the SIP. Large benefit increases are delayed so that shoring up can be provided as needed. This retains the funding stability of a basic VAP and provides level benefits.

Figure 2: SIP performance, 1926-1955

Figure 3: SIP performance, 1955-1984

Figure 4: SIP performance, 1984-2013

A SIP with the cap and shore-up method retains all of the great features of a VAP while at the same time practically eliminating the chance that retirees will ever have their benefits decrease. This design is simple, sustainable, and will provide generations of participants with secure retirements.

SIP funding and accounting

For traditional DB plans, Pension Protection Act (PPA) funding rules and accounting standards are volatile. This is because both asset and liability measures are volatile:

- Assets because of reduced or no smoothing coupled with volatile markets

- Liabilities because of calculations performed on current yield curve rates, which change each year

Significant changes in these values can result in periodic underfunding of the plan and large swings in contribution requirements, accounting expense, and balance sheet liability from year to year.

In a SIP, when assets decline so do liabilities and vice versa. Additionally, SIP liabilities are not sensitive to interest rates, meaning that changes in the yield curve do not affect the value of the liabilities. Because the assets and liabilities move together, the contribution and accounting measures remain stable.

Transition to a SIP

There are several options for sponsors looking to transition from their current plans to a SIP.

DB plan sponsors could:

- Freeze the traditional plan and have all future benefits accrue under a SIP

- Close the traditional plan and have new participants accrue benefits under a SIP

- Convert the traditional plan to opening VAPP benefit with future accruals under a SIP

- Depending on the funding level of the traditional DB plan and future investment returns, this may result in a “wear-away” period for some participants.

DC plan sponsors could:

- Direct some or all of the employer contribution to a SIP

- This would allow for continued tax-advantaged savings by participants in the DC plan as personal savings is a key component of retirement income security.

- Allow for DC plan balances to be “rolled over” to an opening SIP benefit

- This may require a distributable event and result in some leakage.

- A determination letter may be required.

These options allow plan sponsors to greatly reduce future funding volatility and still provide secure lifetime income to their employees.

Conclusion

Milliman Sustainable Income Plans™ (SIPs) offer the following strengths:

- Because the benefits adjust to changes in the market, the employer’s annual contributions and accounting statements are stable.

- Because longevity experience is pooled, employees do not risk outliving their retirement assets.

- Professionally managed assets in a balanced investment portfolio have higher expected returns over time.

- Together, longevity pooling and professional asset management maximize the benefit amount provided for each dollar contributed to the plan.

- People do not have to act as their own investment advisors, managing their assets into old age.

- Returns greater than the hurdle rate increase benefits, providing some expected inflation protection over time.

- Stabilization reserves effectively eliminate the possibility of benefit reductions.

SIP benefit design should be seriously considered by plan sponsors that see their DC participants falling short of sufficient retirement savings and by DB sponsors that cannot bear the contribution volatility that has been endemic in the last decade. SIPs provide lifelong income with inflation protection to participants and stable contribution requirements for the employer.