This is the second article in a three-part series. For more, read "Leveraging quality control sampling for your business," (Part I of III) and "A primer on lifetime of loss reserving: Preparing for FASB" (Part III of III).

In an earlier article, ”Leveraging quality control sampling for your business,” we discussed how a lender could leverage existing quality control procedures to monitor trends in defect rates and manage future potential repurchase risk. In this article, we focus on how predictive analytics can be used to identify and correct defects before closing.

By using an approach as described in this article, sellers could significantly reduce their future repurchase exposure.

Data requirements

All lenders selling loans to the government-sponsored enterprises (GSEs), Freddie Mac and Fannie Mae, have the data available to complete this type of loan defect analysis, which uses historical data collected through the self-assessment quality control reporting process. The data should be loan-level and include underwriting characteristics of the loan (e.g., FICO, documentation level, self-employed borrower flags, origination channel, etc.), geographic data, appraisal data, and a flag indicating if the loans reviewed had a defect. Sellers must also have developed or subscribe to a data warehouse that keeps track of quality control review outcomes over time.

Understanding the GSE target review process

Based on public documents and interviews from the GSEs, the targeted sampling process for loan defects and underwriting violations is based on statistical selection criteria and models. The models are developed using historical repurchase data (similar to that described above), and they identify the loan characteristics of files that are more prone to defects. The requests by GSEs for loan files are skewed toward loans that statistically have the highest incidence rates for potential defects and represent the highest potential loss exposure to the GSEs.

Note that many lenders perform some kind of targeted pre-funding sampling. The methodology typically involves reviewing loans with certain key characteristics, such as cash-out refinance, self-employed borrowers, etc. However, it is our experience that the probability of defect depends on “layered risks.” For example, a self-employed borrower with a low FICO score has a higher level of defect risk than one with a high FICO score. It is important to consider the compounding effect of risk factors when ranking loans by defect probability.

Managing your risk

Freddie Mac recommends that sellers establish a quality control review both at pre-funding and post-closing in its "Quality Control Best Practices" document. Sellers can proactively reduce their repurchase risks by incorporating a pre-funding sampling process to identify loans with the highest risk of defects and take corrective actions before loans are sold.

The effectiveness of a pre-funding review process depends on the ability of the lender to identify two critical outcomes:

- The characteristics and types of mortgages that are more likely to have a defect.

- The characteristics and groups of mortgages that are more likely to be reviewed by the GSEs.

Using data collected from internal quality control reviews and historical repurchase requests from the GSEs, lenders can use predictive modelling and “big data” techniques to “score” applications by their repurchase risks prior to closing. Applications above a certain threshold could receive a second underwrite or additional loan quality reviews to check for errors or omissions in the application pre-funding. A recent study performed by Loan Logics on quality control (QC) reviews performed in 2012 and 2013 found that approximately 40% of all post-funding defects could have been identified and potentially corrected through a pre-funding audit. Using targeted sampling to identify high-risk loans has the potential to increase this hit rate.

Example

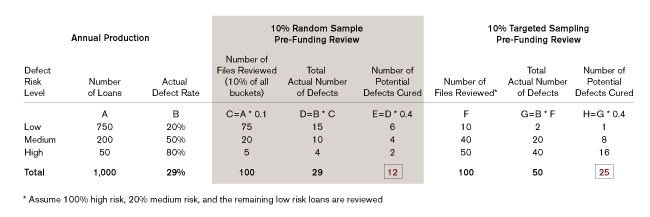

Assume lender “XYZ Mortgage Company” developed a scoring algorithm that segments its production into three levels of defect risk: low, medium, and high. The table in Figure 1 demonstrates how the process described above can reduce XYZ’s repurchase risk on 1,000 loans delivered to the GSEs. We assume 40% of potential defects are cured through a pre-funding quality control review.

Figure 1: Reducing Repurchase Exposure

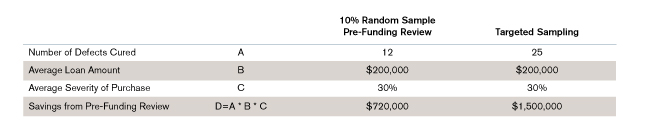

In the above hypothetical example, XYZ would be able to significantly reduce its repurchase exposure by targeting high-risk loans pre-funding. Specifically, a random pre-funding review would correct 12 defects while a targeted approach would correct 25 defects while reviewing the same level of 10% of the loans. Assuming an average loan balance of $200,000 and a severity of 30% for a repurchase, this would result in a reduced repurchase exposure of $780,000 for 1,000 loans originated by XYZ for a savings around $780 per loan (see Figure 2 below).

Figure 2: Savings From Pre-Funding Review

Benchmarking production

In addition to targeted sampling for pre-funding reviews, a defect scoring model can also be utilized by sellers to evaluate and consistently compare the quality of loans being originated by different offices, underwriters, and channels. For example, assume that a seller has developed a network of correspondents for GSE production. The seller will want to monitor the quality of production from correspondents. There are two approaches to this:

- Wait for repurchase requests to come in from the GSEs and compare actual repurchase rates by correspondent.

- Score loan quality on a real-time basis to flag correspondents that are delivering higher-risk loans.

While the first approach will identify high-risk lenders only after losses are incurred, the second approach will identify high-risk lenders during the production process. The advantage of the second approach is the sooner a seller can identify quality problems, the sooner these problems can be addressed and mitigated.