As defined contributions savings plans continue to mature as the primary retirement vehicle for most employees, more discussion/focus is occurring to help former employees protect and grow their accumulated retirement accounts. The Department of Labor (DOL) and Plan Sponsors alike are realizing the growing number of former employee accounts within retirement plans, and they are concerned that former participants might make un-informed decisions which adversely affect their potential retirement accumulation.

Below is an excerpt from the rule proposed by the DOL to modify the definition of a “plan fiduciary” and to add transparency where conflicts of interest exist in the mutual fund marketplace:

The underperformance associated with conflicts of interest—in the mutual funds segment alone—could cost IRA investors more than $210 billion over the next 10 years and nearly $500 billion over the next 20 years. Some studies suggest that the underperformance of broker-sold mutual funds may be even higher than 100 basis points, possibly due to loads that are taken off the top and/or poor timing of broker-sold investments. If the true underperformance of broker-sold funds is 200 basis points, IRA mutual fund holders could suffer from underperformance amounting to $430 billion over 10 years and nearly $1 trillion across the next 20 years. While the estimates based on the mutual fund market are large, the total market impact could be much larger. Insurance products, Exchange Traded Funds (ETFs), individual stocks and bonds, and other products are all sold by agents and brokers with conflicts of interest.1

In short, the DOL comments point to a commonly known issue within the retirement industry, with conflicts of interest affecting the performance/growth of IRA accounts. To further translate, the underperformance is due in large part to excessive fees being charged against former participant’s personal IRA accounts rolled over from qualified plans including 401(k), 403(b) and 457 arrangements.

Below is an excerpt from a U.S. Government Accountability Office (GAO) report to congressional requestors dated March 2013 and titled “401(k) Plan Labor and IRS Could Improve the Rollover Process for Participants”:

Many experts told us that much of the information and assistance participants receive is through the marketing efforts of service providers touting the benefits of IRA rollovers and is not always objective. Plan participants are often subject to biased information and aggressive marketing of IRAs when seeking assistance and information regarding what to do with their 401(k) plan savings when they separate or have separated from employment with a plan sponsor. In many cases, such information and marketing come from plan service providers. As we have reported in the past, the opportunity for service providers to sell participants their own retail investment products and services, such as IRAs, may create an incentive for service providers to steer participants toward the purchase of such products and services even when they may not serve the participants’ best interests.

Common sense pause: Why do financial services aggressively market IRA rollovers? It is profitable for them. Think about it. If the service provider made more money from a participant being invested in a qualified retirement plan, would the provider solicit the participant to take a distribution from that plan and roll it over to an IRA?

The DOL’s proposed rule excerpt above mentions some large numbers regarding the impact that conflicts of interest (i.e., excessive fees) have on the retirement accumulations for IRA owners. It is important to note that regardless of the account type—IRA, 401(k), 403(b), 457—excessive fees will impact a participant’s ability to grow his or her account. This information would probably be more useful if we look at the impact on a micro level.

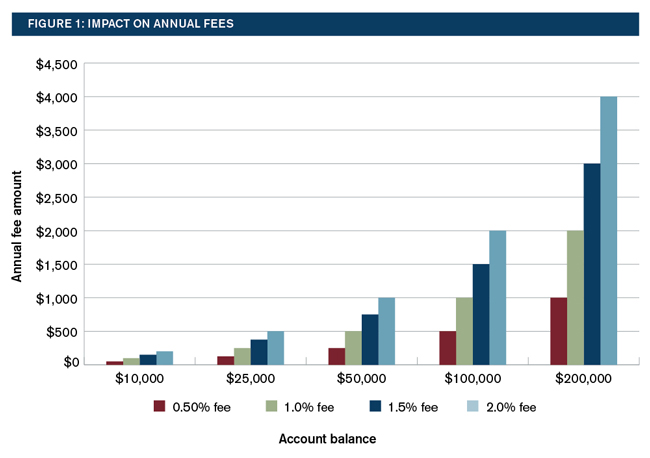

The chart in Figure 1 compares the annual fee charged against account balances ranging from $10,000 to $200,000. These amounts were calculated using fees at 0.5% (50 basis points), 1.0% (100 basis points), 1.5% (150 basis points), and 2.0% (200 basis points). The cost differential is staggering.

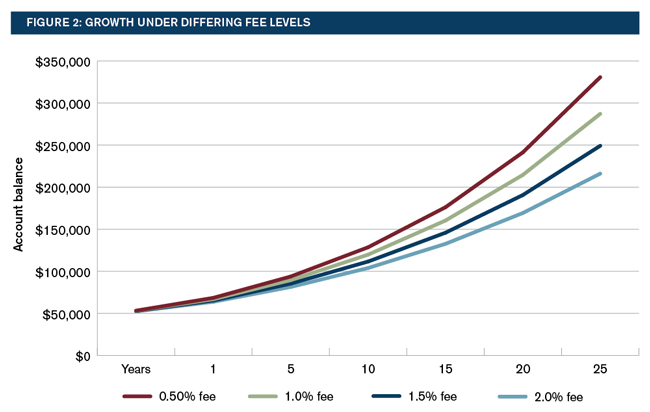

Excessive fees can have a huge impact on the growth of participant accounts over time, significantly reducing what participants are able to accumulate for retirement. The chart in Figure 2 shows the growth of $50,000 over time, assuming a 6% return before fees. Each line represents the growth of the $50,000 account at different fee levels. For example, over 25 years, if a participant paid 2.0% in fees annually, the account would grow to about $217,000. However, if the fees were only 0.5%, the account would grow to $331,000. Excessive fees have a huge impact over time on the growth of an account.

Given the large impact excessive fees can have on former participant IRA rollovers, sponsors are beginning to evaluate potential solutions to address these issues and to assist their former employees. Regardless of employment status, companies and their retirement committees want current and former employees to be able to stay on a path toward a successful retirement. The following is a discussion of what some sponsors are currently doing and a few ideas concerning future changes within the industry that should help protect former employees’ retirement savings.

What are plan sponsors doing to help their former employee participants make better decisions?

Plan design thoughts

Like other transformations within the defined contribution (DC) market, the genesis of these changes is linked to creating a defined contribution plan with some attributes passed down from the “pension plan era.” Participants and sponsors alike are considering changes that shift the plan design discussion from retirement accumulation topics to the "de-accumulation" or payout phase. So what plan design changes are they making?

Partial lump-sum distributions. Many sponsors have modified their plans such that former participants can request a partial lump-sum distribution of their account balances. This enables former participants to satisfy a one-time expense while leaving a portion of their account balances in the plan.

Installments. Years ago, many sponsors simplified their distribution options by removing installments, based on the conclusion that “a participant can set up installments outside the plan (usually an IRA or annuity).” However, now some sponsors have come to realize the issues noted above with outside accounts and some participants are requesting in-plan installments. Some sponsors are again electing to liberalize the distribution options by allowing former participants to elect installment payments from the plan, which gives participants flexibility and allows them to keep their accounts in the plan.

Annuities. Sponsors are reluctant to add this option because they would have to evaluate and select the annuity provider, which is a fiduciary function. Without modification to current law, it's unlikely that many sponsors will add this option.

Education and communication

Guidance on comparing fees. A plan that is run in an unbiased environment is able to provide guidance to participants to help them understand the fees they pay under the current plan provisions and how they might compare those fees to individual retail arrangements. The participant fee disclosure rules introduced a few years ago provide participants with the information they need to access their current plan’s total fees. The plan’s annual notice provides the investment expense ratios from which participants can calculate a weighted expense ratio using their personal account. Plus, using their quarterly statements, a participant can also determine the amount of direct expenses (if any) being deducted from the account. These two key pieces of information yield the total cost of a participant’s account within the qualified plan. If participants can obtain the same information about proposed IRAs or new employers' retirement plans, they should be able to perform an apples-to-apples comparison of the fees. A best practice in the future would be to provide some guidance to former plan participants to assist them in making this comparison so they can then make informed decisions.

Awareness of ability to defer distribution. Following the path of fee transparency and awareness, participants should be made aware of their distribution options when they become former participants. Both the GAO report and the DOL proposed rule discuss the current practices, which are designed to entice participants to roll over their accounts, often without clear or concise information. This additional information might assist participants in making prudent decisions based on their situations. One option that former participants should be notified about is their ability to defer their distributions to a later date and keep their current balances in the plan.

Why would participants choose to defer their distributions and not roll them over to an IRA or their new employer’s qualified plan?

Lower fees. For sponsors of mid- to large-sized plans, generally the total fee incurred by participants ranges from 0.50% to 1.0% per year. The size and complexity of the plan will cause their total fees to vary, but is usually within this range. Plans with a higher utilization of index funds can drop below the .50% in total fees. A best and growing practice within the retirement plan market is for sponsors to provide fee credits to participant accounts; credits from revenue sharing which is a portion of a fund’s overall expense ratio. This practice lowers the total cost of the fund in that the revenue sharing portion is returned to the participants invested in that fund. For more information, see these two articles at:

Monitored investments. Again, most mid- to large-sized plans have an investment committee that works with an outside, independent, registered investment adviser. Together, they ensure that the investment options within a plan meet certain criteria on an ongoing basis. These registered investment advisers are considered fiduciaries to the plan and, therefore, their advice is assumed to be and should be in the best interests of the plan participants.

Online access. With online access, keeping track of one’s assets is easier. Participants shouldn’t feel the need to consolidate their assets for control or tracking purposes. If employees compared the fees and understand the impact fees can have on account growth over time, more plan participants would be inclined to leave their existing accounts in their former employer’s plan at least until retirement age when they actually begin to spend their retirement account.

Why would sponsors want to help former employees?

As defined contribution plans continue to evolve, the retirement plan goals of sponsors shift with the industry. For example, years ago sponsors typically wanted to shed former participants from their qualified plans, reducing the number of participants with a balance, but now, aside from the smaller account balances, sponsors are more accepting of retaining former employee participant balances within their qualified plans. There are a number of reasons supporting this change:

- Law changes have eliminated some of the fiduciary risk associated with nonparticipant-directed accounts.

- Within the mid- to large-sized markets, almost all expenses are paid from the plan assets, which mean the employer cost is not affected if former participants maintain accounts within the plan.

- Many sponsors are proud of the good work performed by their investment committees and independent investment advisers, creating cost-competitive, high-performing retirement plans. They want current and former employees to benefit from this hard work.

- Current employees are driving some of these changes as they begin to approach “former participant” status and they lobby for provision changes that afford them options post-employment.

- Sponsors have a genuine desire to help former participants, many of whom spent years working for the company.

- Within the defined contribution marketplace, as a plan grows (participant counts and/or total plan assets), there is an economies-of-scale effect that reduces fees. Thus, keeping former participants in the plan can produce fee reductions enjoyed by all participants, both active and former. Again, because most plans charge all fees to participants, this economies-of-scale is not biased because all participants share in the reduced fees.

What should sponsors do at this time?

1. Evaluate your current distribution experience with former participants. How many are rolling over their accounts? Do they roll them to new employer plans or to IRAs?

2. Discuss with your recordkeeper and investment adviser possibly liberalizing the distributions options under your plan for former employee participants.

3. Consider communications targeted to former employee participants aimed at giving them guidance about their distribution options—not condoning one option over the other, but at least giving them some general information to help make an informed decision.

4. Sponsors should considering providing participants with guidance to help the former participant compare fees if they are contemplating rolling over their account.

5. If and when the DOL’s proposed changes come to fruition, review the new rules with your adviser/consultant to see if additional changes are necessary.