There’s a fine line between educating investors and coercing – even strong-arming – them into certain patterns of behaviour. Take lump sums.

A diverse range of organisations including the Association of Superannuation Funds of Australia (ASFA), CPA Australia, the Actuaries Institute, and the Australian Prudential Regulation Authority (APRA) have all raised concerns about the extent of lump sum drawdowns.

Super savings, they say, should be predominately used to generate retirement incomes through existing account-based pensions, annuities or innovative new products.

However, a new Productivity Commission report on Superannuation Policy for Post-Retirement has debunked that stance and raised questions about mandating the way Australians use their retirement savings.

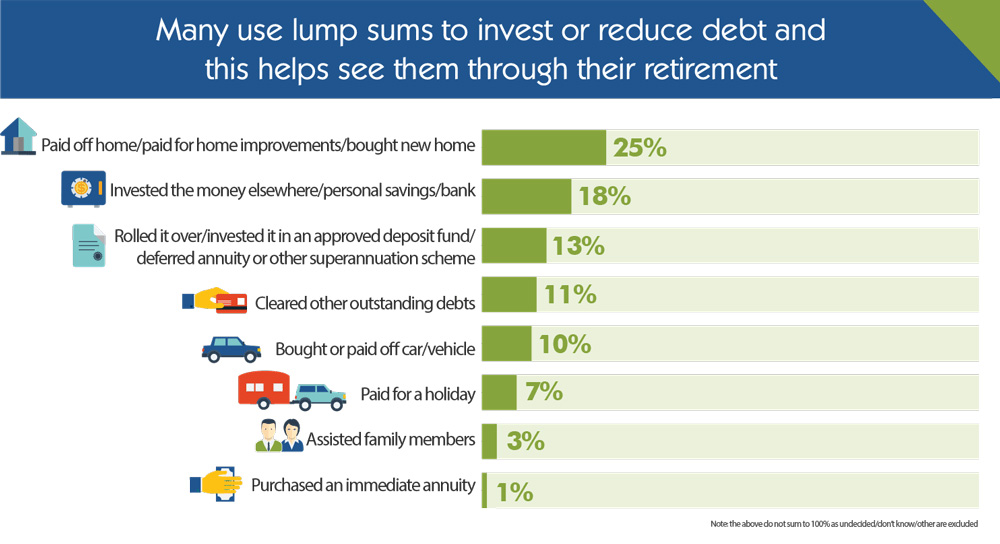

Where the money goes

Source: Productivity Commission

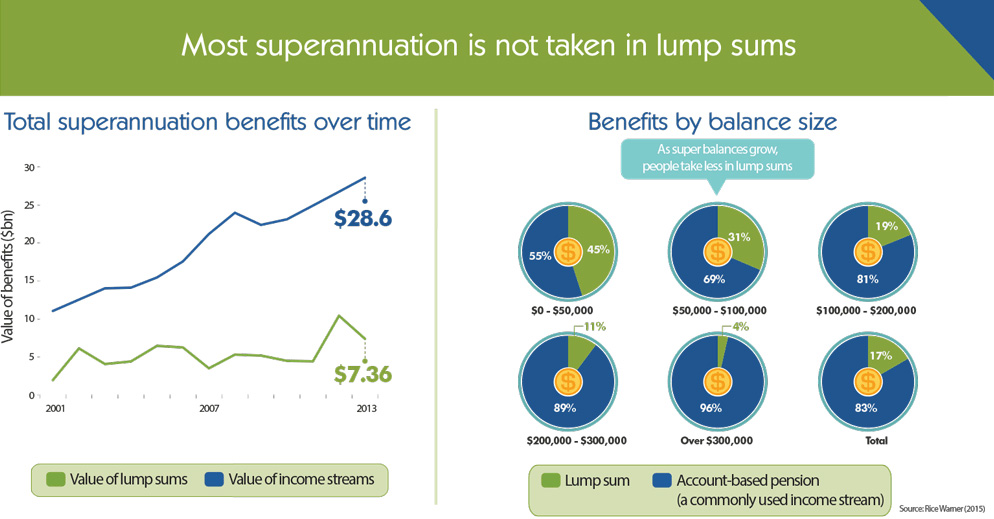

Less than 30 per cent of super assets are taken as lump sums and, when lump sums are taken, they have a relatively small median value of around $20,000, according to Commission estimates based on Australian Bureau of Statistics data from 2011-12.

The recently-launched Colonial First State Income Stream Index found that just 17 per cent of super assets were taken as a lump sum in 2014. The index measured more than 10 million member records representing more than $55 billion in assets.

It is perfectly rational for investors with less super to take a lump sum, which is typically used to repay a mortgage, buy a new home or renovate, or pay off a car or debt. They’re not withdrawing it and blowing it at the casino.

Those who take most of their super as a lump sum rarely have much to begin with – more than 90 per cent of people with up to $10,000 in super take a lump sum at retirement compared to around 30 per cent of people with assets between $100,000 and $200,000.

While last year’s Financial System Inquiry and the 2010 Super System Review both recommended a ‘soft default’ which would widen the take-up of pooled income products, the data cited by the Productivity Commission left it far from convinced.

Good advice: A better solution

Source: Productivity Commission

The Productivity Commission report went so far as to warn that, without careful design, default income products might be ineffective or make some retirees worse off.

“Designing appropriate defaults when there is such diversity necessitates a thorough understanding of people’s superannuation balances, other assets, debts, as well as their personal needs in retirement (which may be affected by their health, marital status and exposure to longevity risk),” the report said.

It sounds a lot like good advice, which also takes into account the interaction of personal retirement savings with the Age Pension, the current low yields on retirement income products, and the capacity of retirees to meet the rising costs of aged care and health issues.

These are components of the four over-arching retirement risks all investors face: longevity, inflation, flexibility (access to capital when needed) and investment volatility. What lifestyle an investor wants in retirement and what it will take to get there are not easy discussions.

It is one thing to measure a clients’ natural tolerance for risk, but how can we shift their capacity for risk when they are not on the path to meet their retirement goals?

It takes personalized, objectives-based advice, rather than a typically blunt focus on risk tolerance. This allows an adviser to take clients with them on the advice journey and, where appropriate, nudge or steer them towards making the right decision.

Whatever course they plot, these retirement decisions should ultimately be made by investors in their own interests, rather than be decisions forced onto them which suit the retirement industry.

This article was first published in Professional Planner.