Much of the news and discussion about the Patient Protection and Affordable Care Act (ACA) focused on the commercial individual and group markets. One of the earliest reforms of the ACA for the commercial market was the medical loss ratio (MLR) requirement.1 Effective January 1, 2011, carriers must meet an 85% MLR for large group and an 80% MLR for individual and small group. Three years later, the MLR requirement2 for Medicare Advantage (MA) is now here. Effective January 1, 2014, Sections 422.2410 and 423.2410 Title 42 of the Code of Federal Regulations now require MA carriers and Prescription Drug Plans (PDPs) to meet an 85% MLR or rebate (refund) any excess revenue to the Centers for Medicare and Medicaid Services (CMS). MA carriers and PDPs must file the calendar year (CY) 2014 MLR report and attestations by December 4, 2015.

The purpose of this paper is twofold: to estimate how the MLR requirement might impact MA carriers and PDPs and to identify the key components of the MA/PDP MLR formula and how it compares with the commercial MLR formula.

To accomplish this first objective, we reviewed the CY 2014 financial statements published on the SNL Financial website (at http://www.snl.com). We summarized the Title XVIII Medicare information from the Analysis by Line of Business, on page 7 of the National Association of Insurance Commissioners (NAIC) orange blank, for all health insurance companies to develop estimates of the MA MLR rebate. Note that the financial statements do not report at the CMS contract level (i.e., S or H number); however, for purposes of this paper, we assumed each company represented a contract. If PDP information was not reported in the Title XVIII then it was not included.

The financial statements represent estimates for most actuarial items such as claim reserves, Risk Adjustment Processing System (RAPS) accruals, and Part D settlements with CMS based on information available in the first quarter of 2015. We recognize companies may have included estimated 2014 MLR rebates for MA/PDP, which could lead to double-counting.

In addition, the financial statements do not clearly show certain components of the MLR formula. For example, MA/PDP costs related to improving health care quality expenses or taxes and fees are not reported separately, and the Part D federal reinsurance subsidy is not separately identified. Given these limitations, we made the following simplifying assumptions to estimate the MA MLR rebates:

- Costs related to improving healthcare quality expenses are equal to 1% of earned premium

- Taxes and fees are equal to 1.5% of earned premium

- The Part D federal reinsurance subsidy is equal to 50% of prescription drug claims (this assumption can vary widely depending on the type of population covered)

As expected, the inclusion of quality expenses, taxes and fees, and the Part D federal reinsurance subsidy increases the MLR. Based on these assumptions, we expect the total rebates to be about $750 million for CY 2014, which represents about 0.6% of total MA/PDP premium. Our estimate of the rebates is consistent with the CMS estimate of $802 million to $833 million, published in Table 8 (page 31307) of the Federal Register on May 23, 2013.3

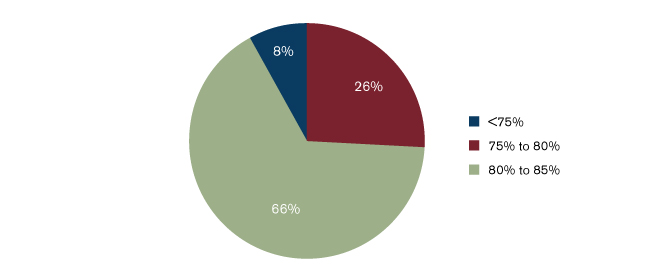

The chart in Figure 1 shows the expected distribution of rebates by MLR. For example, about two-thirds or $500 million of the $750 million in expected rebates would be paid by MA carriers and PDPs with MLRs between 80% and 85%.

Figure 1: Distribution of Expected Rebates by MLR

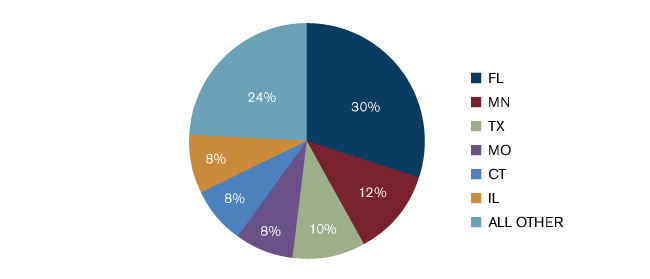

The chart in Figure 2 shows over 75% of the expected rebates will come from six states of domicile.

Figure 2: Distribution of Expected Rebates by State of Domicile

Operating below an 85% MLR for MA/PDP does not guarantee profit; however, it is a leading indicator. The chart in Figure 3 shows the percentage of companies with profitable MA/PDP lines of business by MLR (before the rebate).

Figure 3: Percentage of Profitable Companies by MLR

MLR reporting will be a new requirement for MA carriers and PDPs, and the exact amount (or lack) of rebates will vary by contract and company. Commercial carriers that also offer MA and/or PDP will already be familiar with the general approach; however, they will need to understand the nuances of the MA/PDP formula.

The remainder of this discussion on the MLR rebate will focus on the second objective:

- MLR definition

- Unique components

- Allowed adjustments

- Sanctions

MLR definition

Numerator equals incurred medical and pharmacy claims, including an estimate of unpaid claim reserves and incurred medical incentive pool and bonuses, plusPart D federal reinsurance subsidyplus contingent benefit/lawsuit expenses plusMA rebate for Part B premiumplusMSA enrollee deposit plus fraud reduction expenses plus improving health care quality expenses

Denominator equals earned premium based on final risk scores plusPart D federal reinsurance subsidyplusMSA enrollee depositplusPart D risk corridorminus federal and state taxes and licensing or regulatory fees

Earned premium includes member premiums/CMS premium subsidies, MA risk rate and rebates (cost-sharing buy-downs, mandatory supplemental benefits, Part D premiums, and Part B premiums), and Part D direct subsidy. The Part D federal reinsurance subsidy and risk corridor are based on the final reconciliation with CMS.

The differences from the commercial MLR definition are highlighted in red.

The base MLR is calculated as the numerator divided by the denominator and is further adjusted based on the credibility of the data, which is determined by the number of 2014 member months (discussed in greater detail below). The final MLR is then compared against the MA/PDP target of 85% and a rebate is owed to CMS if the final MLR is less than 85%.

Unique components

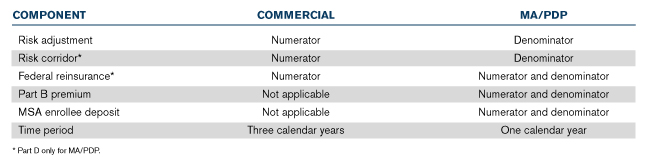

The table Figure 4 shows the components that are unique to both the commercial and MA/PDP MLR formulas.

Figure 4: Major Differences Between the Commercial and MA/PDP MLR Formula

The risk adjustment, risk corridor, and reinsurance are included in both formulas; however, they are treated very differently.

Allowed adjustments

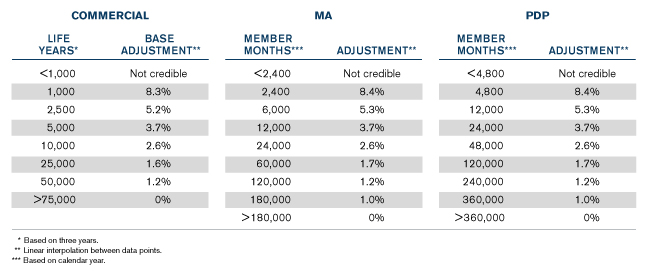

Credibility

As noted above, the base MLR is further adjusted to reflect the credibility of the data. The table in Figure 5 compares the commercial, MA, and PDP credibility thresholds.

Figure 5: Credibility

The MA and PDP full credibility thresholds are much higher for the MLR calculations than the fully credible thresholds for MA (24,000 member months) and PDP (18,000 member months) experience used in developing the bids.

Commercial deductible factor

The commercial MLR formula allows an adjustment for high-deductible plans. The deductible factors adjust the credibility in Figure 5 to reflect that the higher-deductible plans would pay fewer claims and be subject to more volatility. The MA/PDP formula does not include a deductible adjustment factor (i.e., it would always be 1.000).

The final MLR with Credibility equals Base MLR plus (Credibility times Deductible Factor)

Sanctions

In the commercial market, if the MLR is below the target (85% for large group and 80% for individual/small group), a rebate—premium x (target - MLR)—is paid to the policyholder (group or individual) so the policyholder directly benefits from the lower-than-expected MLR.

In the MA/PDP markets, the rebate is paid to CMS so the policyholder (member) does not receive any benefit from the lower than expected MLR. In an effort to ensure MA carriers and PDPs are continually providing value to the policyholder, CMS included sanctions for MA and PDP carriers that do not consistently meet the MLR requirement:

- If an MA carrier or PDP has an MLR that is less than 85% (after credibility adjustment) for three or more consecutive years, then CMS will not permit the enrollment of new enrollees under the contract for the second succeeding contract year.

- If an MA carrier or PDP has an MLR that is less than 85% (after credibility adjustment) for five consecutive years, then CMS terminates the contract as of the second succeeding contract year.

MLR reports will be due in December following the contract year (i.e., 2015 for 2014); however, MA carriers or PDPs that fail to meet the MLR for two consecutive years will be required to submit their MLR reports earlier so that CMS has time to implement the sanctions.

Summary

Clearly identifying and supporting fraud reduction expenses, healthcare quality expenses, and federal and state taxes and licensing or regulatory fees are keys to properly reporting MLRs and minimizing MLR rebates.

The inclusion of the Part D federal reinsurance subsidy in both the numerator and denominator of the MA/PDP MLR formula increases the MLR, as it implicitly assumes a 100% MLR for this portion of the costs. While this helps MA carrier MLRs, it can significantly increase a PDP MLR, especially for those enrolling a significant proportion of high-cost members.

As MA carriers and PDPs begin to estimate any MLR rebate for quarterly and year-end financial statements, they need to be aware of the expected risk scores changes that will occur in late summer following the contract year (i.e., 2015 for 2014), which are due to the final RAPS submissions. MLR rebates reported on the financials should include a best estimate of RAPS accruals.

The CMS sanctions are real and could significantly damage an MA carrier’s or PDP’s reputation and disrupt a financially successful product (i.e., MLR < 85%). MA carriers need to especially consider the MLR when developing bids, as overly conservative risk score projections, trends, impacts of new utilization management programs, or other assumptions could lead to lower-than-expected MLRs. Continual monitoring of assumptions is essential to balancing the MLR and a competitive product.

The 85% MLR selected by CMS is a target and does not guarantee profitability. Companies still need to manage administrative costs including internal/external efforts for properly coding diagnoses and improving CMS star ratings. Both of these initiatives are among the primary drivers of successful MA carriers.

Courtney White, FSA, MAAA, is a principal and consulting actuary with the Atlanta office of Milliman. Contact Courtney at 404-254-6741 or [email protected].

The materials in this document represent the opinion of the author and are not representative of the views of Milliman, Inc.

Limitations

This paper was not intended to be an all-inclusive discussion of either the commercial or MA/PDP MLR formula but was intended to summarize financial results at various MLR levels and highlight the significant differences between the two formulas. It may not be appropriate, and should not be used for other purposes. Companies should consult the appropriate MLR instructions prior to completing the report and attestations.

The rebate amounts reported above are illustrative based on a set of assumptions, which is due to the limited information presented in the financial statements. While we reviewed the information for reasonableness, we have not audited or verified this information. It is certain the actual amounts reported by the companies will vary for a number of reasons.

1Centers for Medicare and Medicaid Services (CMS) Medical Loss Ratio (MLR) Annual Reporting Form Filing Instructions for the 2014 MLR Reporting Year.

2CMS MLR Report for Medicare Advantage Organizations and Prescription Drug Plan Sponsors for the Contract Year (CY) 2014 MLR Reporting Year Filing Instructions (April 8, 2015).

3Federal Register (May 23, 2013). 42 CFR Parts 422 and 423: Medicare Program; Medical Loss Ratio Requirements for the Medicare Advantage and the Medicare Prescription Drug Benefit Programs; Final Rule. Retrieved October 30, 2015, from http://www.gpo.gov/fdsys/pkg/FR-2013-05-23/pdf/2013-12156.pdf.