With the 2016 presidential campaigns well under way, a number of key issues that affect the financial markets have begun to make headlines, from terrorism to tax reform. As with any election cycle, these buzzwords and talking points are constantly shifting and changing. One of these topics that has surfaced sporadically is student loan debt. Regardless of whether or not it is at the top of any candidate’s talking points list, student loan debt is a key concern underlying the country’s economic stability.

Trends: Student Loan Debt and Delinquencies

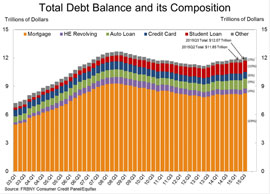

The Federal Reserve Bank of New York recently released its Q3 2015 report on household debt and credit, which allows us to compare the trends in student loan debt and delinquencies since our last article, published in March 2015.19 Figure 1 shows the growth and composition of all categories of outstanding U.S. household debt. As we noticed last year, outstanding student debt is second only to mortgage debt in terms of total debt outstanding.

Figure 1

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax.

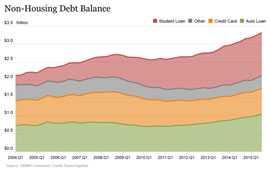

Additionally, since Q1 2012, student loan debt has grown from $0.90 trillion to $1.20 trillion, as shown in Figure 2, an increase of nearly 33% in 13 quarters. While auto debt has grown at a similar rate, mortgage debt, credit card, and other consumer debt have remained stagnant over the same time period.

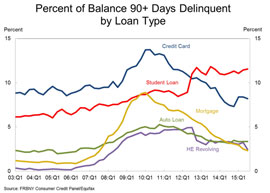

Figure 3 shows how the seriously delinquent rate for student loans has been trending and how this compares with other types of loans. Approximately 11.25% of aggregate student loan debt is either 90+ days delinquent or in default as of Q3 2015. Even though the recent trend in serious delinquencies has been flat since Q3 2013, student loan delinquencies remain elevated relative to all other kinds of consumer debt and have actually increased from Q1 2012, whereas delinquent loans for all other debt have declined, and, in some cases, have done so significantly.

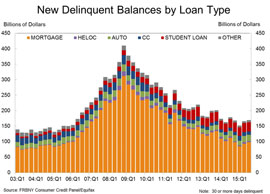

Figure 4 shows that new student loans entering delinquency have remained consistent over the last three years in terms of loan balance. Contrast this to credit card and mortgage delinquencies, which have shrunk in terms of balances over the same period. This demonstrates that student loan delinquencies have still not yet fully abated.

The cumulative impact of the weighing student loan debt continues to be felt in other important areas of the economy. As shown in Figure 5, in Q3 2015, only 35.8% of those under 35 were homeowners—a slight increase from the first quarter, which, at 34.6%, represented the lowest figure over the last 23 years.20 The overall annual homeownership rate continued to drop to 63.4% in Q2 2015, the lowest rate since 1995 (this rate was near 69% at the peak in 2004), before increasing slightly in the third quarter. While there are many contributing factors to this phenomenon, student loan debt has undoubtedly had an impact. Credit has been much tighter since the global financial crisis, and lenders cannot ignore student debt when calculating certain lending measures such as debt-to-income ratios when extending loans to consumers.

According to the Quarterly Report on Household Debt and Credit, Americans currently hold $1.19 trillion in student loan debt, and approximately 11% of these loans are currently three or more payments behind (90 or more days delinquent).1 As seen in Figure 1 of the inset, this trend of delinquency has been on the rise. As of 2012, the percentage of student loan debt 90 or more days delinquent has surpassed credit card debt to become the most frequent type of delinquent household debt. As can be seen in Figure 2 of the inset, as of Q3 2015, student loan debt makes up 10% of all household debt. This makes student loan debt the second-largest form of household debt, sandwiched between home mortgages (69%) and auto loans (9%).

According to the 2015 How America Pays for College study,2 38% of students attending college in the 2014-2015 academic year are borrowing money to do so (or having family borrow money on their behalf). The majority of this money comes from loans from the federal government, representing 60% of borrowing for the 2014-2015 academic school year.3 A mere 5% of the borrowing for the 2014-2015 academic year was from students taking out both federal and private loans, and an additional 2% of students had only private student loans.4

The current state of student loan debt is only the tip of the iceberg, however. Today, a four-year college degree is more valuable than it ever has been. In 2013, the pay gap between holders of college degrees and everyone else reached a record high. Workers with four-year degrees made 98% more an hour on average than people without a degree, up from 89% in 2008, and significantly higher than the 64% mark seen in the early 1980s.5 This pay gap is not only indicative of the benefit of obtaining a degree, it also represents an underlying issue: there are not enough college graduates.

The apparent high cost of a four-year college education is likely making some people shy away from attending college, even though the estimated cost of not attending college is $500,000 over a person’s lifetime.6 Because of the global financial crisis, states are spending 20% less per student on average than they did in 2008, and colleges have responded by raising tuition. In-state tuition and fees rose 42% between 2004 and 2014 after adjusting for inflation.7 Students have needed to fill this gap by taking out more and more student loans.

If prospective students had greater access to (or less need for) debt from the federal government or from private firms, it’s likely that we’d see an increase in the number of college graduates, which is nothing but positive for the country as a whole. However, as they say, “there’s no such thing as a free lunch.” Obviously any reforms to the postsecondary education financing system will need to be funded by something or someone. Are the potential benefits worth the cost, which will likely be borne by taxpayers?

Clearly, any form of government lending naturally becomes a political hot button, and it is not our intent to opine on whether or not the government should or should not get more involved in the student loan area. Nor is it our intent to opine on whether or not a student loan modification or even a forgiveness program is warranted. However, with so many households under the burden of student loan debt and many more considering their children’s future college expenses, it is important to look at the roles of the government and the private market. We will discuss these parties’ current roles and examine how they might change under the presidential candidates' student loan proposals.

We will be focusing on the proposals currently laid out by the leading Democratic candidates, Hillary Clinton and Bernie Sanders. As of the date of publishing, the leading Republican candidate, Donald Trump, has not released a proposal outlining his reforms for the student loan world; however, he has been quoted as saying: “That’s probably one of the only things the government shouldn’t make money off. I think it’s terrible that one of the only profit centers we have is student loans."8

Government’s current role

The government plays a significant role in student loan lending. Currently, the major forms of federal financial aid for college students are grants and loans. Federal Pell Grants are currently the largest federal grant program available to undergraduate students. Pell Grant availability is limited to students with a financial need and represents the foundation of a student’s financial aid package. As of June 2015, the annual Pell Grant appropriations totaled over $28.9 billion, up from $2.2 billion in 1980.9 Many state and local governments also have grants available for college students.10

Pell Grants require students to have a financial need and do not need to be repaid. On the other hand, federal loans, which must be repaid, are available to all students (except those who have previously defaulted on a student loan or have been convicted of drug offenses and have not completed a rehabilitation program). These loans can be subsidized (where the loan does not accrue interest while the student is in school) or unsubsidized (where interest is accrued and added to the principal).

Federal student loans generate billions of dollars in profit for the government each year11 because the interest payments far exceed borrowing costs, loan losses, and administration of the loans. Despite the significant number of student loans in default by three or more payments, losses on student loans remain very low. This is partially due to the fact that student loans cannot be discharged in bankruptcy (unless repaying the loan would create an “undue hardship” for the borrower).

However, this “profit” may never actually be realized. Student loan risk is very long-tailed, while the revenue is heavily front-loaded. It is difficult to quantify the propensity of student loans to default over their long lives, even assuming a relatively stable economy. In addition, for federal student loans, the interest rates are fixed. As the interest rate environment fluctuates, it’s difficult to project what the “profit” from a portfolio of student loans will ultimately be. Therefore, the assumptions that make up future profits are subject to substantial volatility and can lead to a wide array of very reasonable potential outcomes.

Private market’s current role

Private student loans are significantly more expensive than government-provided loans and typically are only used when borrowers exhaust the maximums available under the federal loans. These loans differ in that they are underwritten (to an extent). Lenders use credit scores and the incomes of the students and their parents to determine available amounts and interest rates. Another difference is that these loans accrue interest immediately (though payment is still delayed until after graduation). As the interest rates on these loans are not set by Congress, they are higher than those available from the federal government. Private loans offer higher limits than federal loans, which can help ensure that the student is not left with a budget gap.

Proposals

Both of the top Democratic candidates have released proposals on how they would deal with the student loan problem if elected. Clearly, it’s important to note that these are proposals and would require significant debate (as well as bill authoring and passage) to become the law of the land. We will not comment on the likelihood of either of these plans coming to fruition, but rather will focus on the key points of the plans to determine if either one leaves room for the private student loan market.

Clinton plan

The current Democratic front-runner, Hillary Clinton, has titled her plan for education reform “The New College Compact.”12 Her plan “ensures that students can attend a 4-year public college without taking loans for tuition, attend community college tuition-free, pushes states to re-invest and schools to reduce costs and raise graduation rates, and rewards innovation that makes a real difference in student outcomes.”13

Clinton plans to provide states with grants to ensure no student should borrow for tuition and to improve affordability for expenses not related to tuition. The plan is to require individual states to work with their colleges and distribute funds to meet these requirements by lowering the overall cost of college. The amount of the grant will depend on the number of students enrolled with higher benefits for lower-income students. Clinton specifically states that “families will be expected to make a realistic and simplified family contribution,” and students will be required to contribute based on wages from 10 hours per week of work (it’s unclear whether or not this implies a work requirement to receive benefits).

In addition to following up on President Obama’s plan for tuition-free community college, Clinton would cut the interest rates on student loans, so that the government doesn’t profit from the loans. She would cut current interest rates as well as those on loans issued in the future. Clinton would further expand income-based repayment options to simplify them and make them universally available as well as extend certain tax credits.

Her plan, she says, will increase college enrollment and push colleges to increase their graduation rates. Her plan incorporates the principles of the “Student Protection and Success Act,” which, among other things, includes provisions to penalize colleges when their graduates are unable to repay their loans, essentially giving the college some “skin in the game.”

Clinton’s plan would be paid for by an increase in taxes via the closing of some “loopholes and expenditures for the most fortunate.” Her campaign estimates the cost at $35 billion a year for the next 10 years. More than half of this is slated to go toward the aforementioned grants to states and colleges. A third will go to relief on interest from student loan debt, including allowing students to refinance their loans at the current low rates.

Sanders plan

Bernie Sanders’s proposal is posted under the bold heading “It’s Time to Make College Tuition Free and Debt Free.”14

Sanders proposes to make tuition free at public colleges and universities. He notes that this is already happening in developed countries around the world (Germany, Chile, Finland, Norway, and Sweden, to name a few). Second, he proposes to stop the federal government from making a profit on student loans, which is something that even the Republican front-runner agrees with as we noted earlier. He proposes to eliminate the profit on federal student loans through lowering the interest rates, which is his third step. To achieve this goal, Sanders proposes changing the formula for student loan interest rate calculations back to the formula used prior to 2006, which would drop student loan interest rates to 2.4% (from 4.3%).

Along with lowering the interest rates on new undergraduate loans, his plan will allow graduates currently repaying their student loans to refinance them at the current low interest rates. His final step is to make college debt-free for the lowest-income students. While he doesn’t define who meets this criteria, he proposes that colleges and universities would be required to meet 100% of the needs of these students, including board, books, and living expenses.

Obviously a dramatic overhaul with a dramatic increase in benefits needs to be paid for with tax dollars, and Sanders proposes a new tax on “Wall Street Speculators” to pay for the increased student loan benefits, citing similar taxes already in place in 40 countries around the world.

Comparison of proposals

Both proposed plans contain similar aspirations. While Clinton’s is more detailed and provides some insight on other enhancements to the secondary education system, there’s not much differentiating it from the Sanders plan. The plan’s primary deviation is in the funding of the changes, which is beyond the scope of this article. The remainder of this article will not differentiate between the two plans as the core aspects of them are largely identical.

Private market under the proposals

The proposed changes to the federal student loan programs would represent a complete paradigm shift if they were to be implemented as proposed (which is our assumption for the remainder of the article). Providing essentially “free” postsecondary education is far from a radical idea, but also far from one many would consider realistic. The impact it would have would be felt immediately and for the long term. The changes would give the country a more educated employee base, which is a definite positive, and they could likely lead to decreased reliance on consumer debt. These benefits, of course, ignore the implications of the proposed changes in the tax code that would fund the change. Analysis of these changes is beyond the scope of this article.

But does the plan allow any room for the private market? If tuition is to be free at public colleges and universities, then expenses that are not tuition-based will be increasingly covered by federal loans and grants originally earmarked for tuition costs. This dramatically decreases the total amount of borrowing that will be required by students at public universities.

That leaves the industry with largely nonpublic universities. Neither proposed plan included details on raising the limits of borrowing currently in place. While the proposal will significantly lower interest rates on loans issued by the federal government, there will still be a gap between costs and federal borrowing, to the extent that the limits are not raised, which will need to be accommodated by the private market. To the extent that a funding gap exists for public universities, there will be an opportunity for the private market as well, but that funding gap is likely to be less material.

In addition, it seems reasonable to assume that there may be a shift in enrollment from nonpublic to public universities to take advantage of the additional available federal funding. As of 2013, over 25% of college students (5.63 million) attended a private university. A recent survey15 indicates that public school graduates earn (on average) 80% of what private school graduates do. If private schools can successfully promote their degrees as “more valuable” than public school degrees (whether through a perceived “better” education, higher after-graduation salaries, or stricter admissions standards), there may still be strong incentive to choose a private school over a public school, especially for higher-income borrowers.

Can the private market fix the problem?

While the proposed plans have garnered a lot of attention from college students and from the media, let’s take a step back and see if there’s another solution to the problem. Even if, as Sanders states, the student loan interest rates are lowered to 2.37%, that still leaves significant flexibility for private lenders. A lender with a powerful predictive model might theoretically be able selectively underwrite student loans and offer them to students at rates even lower than the 2.37% number. This is far from a new concept, of course.

Students with high earning potential will likely have low default rates, which makes them attractive borrowers, especially in the student loan area, where the federal student loan rate is fixed (at the same rate) for all borrowers, irrespective of whether they’re studying medicine or massage therapy. Companies such as CommonBond, a venture capital-backed student loan lender, are already taking advantage of this. Currently, they’re focusing on refinancing student loans for those they deem as creditworthy. As of December 2014, CommonBond has made over $100 million in loans to current students and graduates of master of business administration (MBA), doctor of jurisprudence (JD), doctor of medicine (MD), and engineering programs. SoFi (another venture capital-backed lender) has refinanced more than $1 billion of student loan debt held by over 13,500 graduates.

It’s a common sense business concept: pick the borrowers who are the least likely to default, and offer them a rate lower than they can get from the federal government. The flat federal rate essentially assumes a uniform risk margin among all borrowers (or, more accurately, is set high enough so that the non-risky borrowers subsidize the higher-risk ones). A lender that can underwrite and lend to those non-risky borrowers can stand to profit. The low default rates of the borrowers who would qualify for these rates make this a good opportunity for investment.

This year (for 2015-2016 students), the interest rate for federal loans to postgraduate medical students is 5.84% for the first $40,500 (the limit on a graduate Stafford loan). The remainder of the student’s expenses can be covered with a Direct Plus loan at 6.84%.16 For comparison's sake, a moderately qualified borrower (660-679 FICO, 5% down) can get a 30-year fixed mortgage at 4.09%17 in the city of Chicago.

SoFi and CommonBond take advantage of the lack of differentiation in the federal borrowing rate and offer refinancing between 3.625% and 6.00% for a five-year refinance, significantly below the federal rates. The difference, of course, is the underwriting. Lenders backed by venture capital are focusing on the cream of the crop, the doctors and engineers from prestigious universities. It is not unrealistic to assume that this business model can be expanded and that a powerful predictive underwriting model would allow a lender to significantly limit its default risk and offer a rate far below the federal rate. It’s starting with refinancing of existing debt, but the next logical step is to begin to offer it to the elite students currently enrolled or yet to enroll. Currently, private investors believe that $200 billion of the $1.2 trillion of student loan debt is in a creditworthy tranche.18

This doesn’t come without a potential downside. If the “best” loans are removed from the government programs and charged a lower rate, then that leaves the government with the rest-- the “worse” loans, the ones most likely to default, a classic case of adverse selection. As in the insurance industry, adverse selection could potentially cause serious problems as more and more loans left with the government have a higher propensity to default (relative to those loans borrowing from private companies). The risk of adverse selection highlights just one of the many difficulties in quantifying the ultimate costs (and resulting profits) of long-tailed risks.

Could this enhanced private market work hand in hand with the government plans as outlined by Clinton and Sanders? Probably, although there would be less room for error. A decrease in the federal interest rates would clearly necessitate a similar decrease in the rate offered by the private market. At some point, that rate would likely become too low to generate a reasonable return. Further work would be required to determine this tipping point.

Conclusion

The 2016 Democratic presidential front-runners have proposed bold plans for reshaping the nation’s postsecondary education system and for correcting some problems in the student loan marketplace. These increased opportunities for students may decrease the opportunity for private lenders to make a profit without dramatic changes to their operations and may drive a number of them out of the market.

However, there’s potential for the private equity market to fix this problem by allowing students to refinance at lower rates based on their earnings potential and other underwriting considerations. A logical extension of this type of program could lead to a completely underwritten, “qualified borrowers only” private market, offering premium interest rates to borrowers perceived as less risky. This could help reduce the financial burden on graduates as well as current and future students, but care must be taken to prevent a grab for market share.

Regardless of the outcome of the election, the student loan area continues to evolve as private investors look at the $1.2 trillion of student loan debt to decide if a gamble on “elite” students is prudent. Whether or not this private market is needed after the election remains to be seen.

1Federal Reserve Bank of New York (May 2015). Quarterly Report on Household Debt and Credit.

2Sallie Mae (2015). How America Pays for College, p. 16. Retrieved January 14, 2016, from http://news.salliemae.com/files/doc_library/file/HowAmericaPaysforCollege2015FNL.pdf.

3The College Board. Total Undergraduate Student Aid by Source and Type, 2014-15. Trends in Higher Education. Retrieved January 14, 2016, from http://trends.collegeboard.org/student-aid/figures-tables/total-undergraduate-student-aid-source-and-type-2014-15.

5Leonhardt, D. (May 27, 2014). Is college worth it? Clearly, new data say. New York Times. Retrieved January 14, 2016, from http://www.nytimes.com/2014/05/27/upshot/is-college-worth-it-clearly-new-data-say.html?_r=0.

7The Briefing. College compact: Costs won't be a barrier. Factsheets. Retrieved January 14, 2016, from https://www.hillaryclinton.com/briefing/factsheets/2015/08/10/college-compact-costs/.

8 Cirilli, K. & Cusack, B. (July 23, 2015). Video: Exclusive: Trump threatens third-party run. The Hill. Retrieved January 14, 2016, from http://thehill.com/homenews/campaign/248910-exclusive-trump-threatens-third-party-run.

9 U.S. Department of Education (September 25, 2015). Education Department Budget History Table: FY 1980–FY 2016 President's Budget. Budget History Tables. Retrieved January 14, 2016, from http://www2.ed.gov/about/overview/budget/history/index.html.

10Institute of Education Sciences (May 2015). Grants and Loan Aid to Undergraduate Students. National Center for Education Statistics. Retrieved January 14, 2016, from https://nces.ed.gov/programs/coe/indicator_cuc.asp.

11Nasiripour, S. (April 14, 2014). Student loan borrowers' costs to jump as Education Department reaps huge profit. Huffington Post. Retrieved January 14, 2016, from http://www.huffingtonpost.com/2014/04/14/student-loan-profits_n_5149653.html.

12Hillary (August 10, 2015). The new college compact: Costs won't be a barrier, debt won't hold you back. Retrieved January 14, 2016, from https://www.hillaryclinton.com/issues/college/.

14Bernie 2016. Issues: It's Time to Make College Tuition Free and Debt Free. Retrieved January 14, 2016, from https://berniesanders.com/issues/its-time-to-make-college-tuition-free-and-debt-free/.

15Wei, S. How your college choice affects your career. NerdWallet. Retrieved January 14, 2016, from http://www.nerdwallet.com/blog/nerdscholar/college-and-career-study/.

16 McGrath, M. (December 10, 2014). Student debt as an asset class: A $1 trillion opportunity? Forbes. Retrieved January 14, 2016, from http://www.forbes.com/sites/maggiemcgrath/2014/12/10/student-debt-as-an-asset-class-a-1-trillion-opportunity/#2715e4857a0b34cc995f7ced.

17Bankrate.com. Retrieved December 23, 2015.

19Hunley, L.A. (February 3, 2015). The Student Loan Debt Crisis Revisited: For-Profits Come to the Forefront. Retrieved February 11, 2016, from http://us.milliman.com/insight/2015/The-student-loan-debt-crisis-revisited-For-profits-come-to-the-forefront/.

20U.S. Census Bureau (January 28, 2016). Residential vacancies and homeownership in the fourth quarter 2015. Press release. Retrieved February 11, 2016, from http://www.census.gov/housing/hvs/files/currenthvspress.pdf.