Technology has radically reshaped the business world in the last decade. The pace of change is staggering with hundreds of firms, from start-ups to mature businesses, attacking traditional ways of doing business.

But while this disruption is exciting, the effect many of these companies are having on the broader business ecosystem is even more intriguing.

Consumers– emboldened by a mix of smartphones, internet connectivity, open information and new technology– are no longer blindly accepting packages that include some unwanted products and services. Instead, they are demanding greater choice and flexibility.

The result has been dubbed “the great unbundling” and it has reshaped industries as widespread as entertainment, utilities and travel– and increasingly, financial services.

Unbundling everywhere

At its worst, bundling raises prices by forcing consumers to buy products or services they don’t really want with those that they do.

For example, pay TV or cable packages often include programs and channels that consumers don’t want. The rise of the Internet-powered Netflix (which started out as a DVD-by-mail service when I was in college in the U.S.) and other services such as Hulu, HBO Go, Apple’s iTunes and Amazon has changed that.

This content has been carved out from cable providers’ higher cost content delivery mechanisms and allows consumers to make bespoke choices.

Similarly, travel agencies no longer have exclusive access to pricing data and booking platforms that allows them to package dream holidays. Now consumers can book holidays themselves with online websites such as Expedia. Travel agents now focus on planning and recommending the perfect holiday for consumers too busy to do it on their own.

While financial services may be a more complex area, consumers are also beginning to take advantage of the unbundling trend.

Investment platforms act as a portal to invest in managed funds with the benefit of performance/tax reporting. But several new offerings can now be combined to potentially deliver similar results at lower cost for investors.

For example, software-as-a-service providers, such as local firm Sharesight, deliver performance and tax reporting of shares, managed funds and other investments for a fixed monthly fee. The ASX mFund platform allows investors to buy managed funds via their broker while a wide range of low-cost exchange-traded funds (including strategic beta products) offer another investment alternative.

These products and services weren’t launched specifically to disrupt investment platforms– they were instead built to do one thing well. But used together, this broader ecosystem offers an effective alternative.

Can longevity solutions be unbundled?

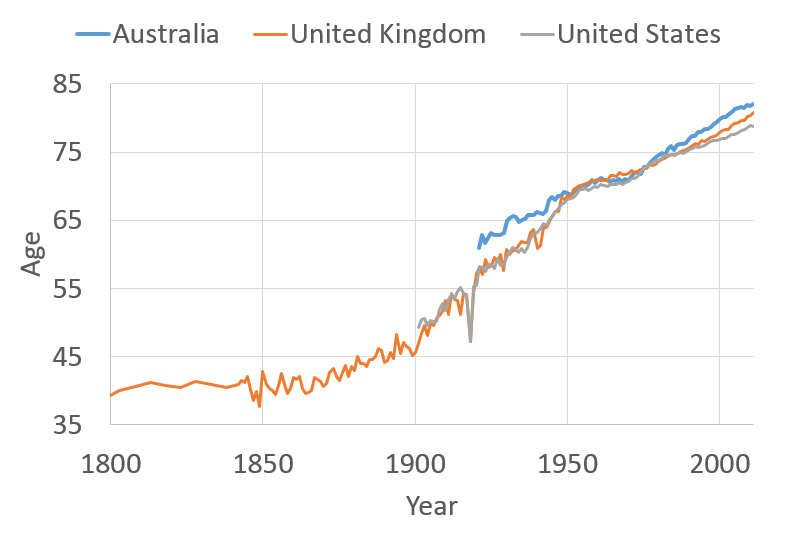

Longevity risk– the chance that an investor will outlive their retirement savings– poses a growing challenge as improvements in healthcare, living standards and agriculture continue to boost lifespans.

Figure 1: Life expectancy from birth

Source: Clio Infra

However, longevity risk is not just a factor of rising life spans. Other factors include the investment returns generated by a retiree’s portfolio, the level of inflation (and whether returns outpace the areas where retirees are spending their money, such as healthcare), and retirees changing expenditures as they age.

The industry’s current longevity risk solution– lifetime annuities and similar products– lack flexibility and effectively bundle longevity risk with assets not typically associated with extremely long-dated liabilities.

These government bonds and similar assets don’t last the 20 to 30 years that investors are now expected to spend in retirement. In fact, there is a more than a 70% chance that at least one of a male/female couple who retire today at age 65 survives to age 90.

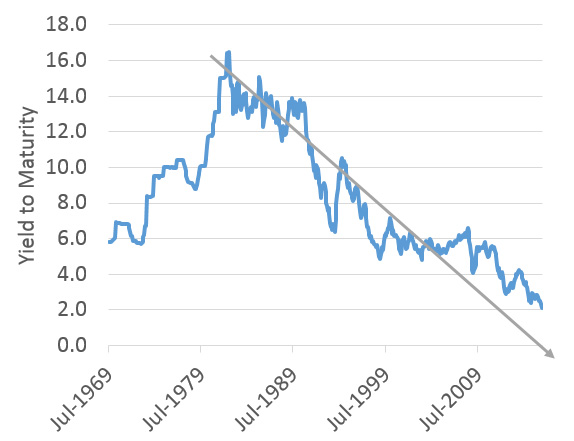

This added risk is built into the pricing structure of lifetime annuities. In addition, fixed income assets which typically underpin lifetime annuities are currently locking investors in at historically low rates.

Figure 2: 10 year Australian government bond yield

Source: Reserve Bank of Australia

But there is a way to unbundle these components and build a better solution with a mix of best-of-breed strategies.

Milliman’s alternative approach to longevity risk is built on our work with funds, asset managers and life insurers, where we regularly unbundle risk management strategies from balance sheets and structured products.

We believe that longevity risk management can be unbundled from the underlying asset allocation found in many current products. Funds can instead give investors a greater choice of higher-returning portfolios and manage greater volatility and potential capital losses with managed risk strategies.

Meanwhile, a separate pooling mechanism, where benefits are transferred to members who live longer than average, directly manages many people’s fear that they will outlive their savings and stops them from overly limiting withdrawals.

This unbundled approach, part of our Retirement Enhancement Trust solution, can reduce costs, boost income through longevity pooling and lead to higher returns with greater investment flexibility.

The benefits of unbundling are being seen far and wide and the retirement industry is no longer immune from its effects. But just as importantly, an unbundled approach is particularly well suited to solve complex challenges such as longevity risk.

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.

An investment in an underlying portfolio, whether with or without Milliman Managed Risk Strategy (MMRS) is subject to market and other risks and no guarantee or assurance is given by Milliman AU or any company in the Milliman group that the use of MMRS in conection with an underlying portfolio will not give rise to losses or that the performance of the MMRS in relation to the underlying portfolio will remove volatility completely or to the extent depicted in an illustration or fully replace losses in the underlying portfolio or to the extent depicted. While generally assets used in connection with the MMRS are liquid, this may not be the case in all circumstances. Further, during periods of sustained market growth, the return to clients from the combination of an underlying portfolio and MMRS should be less than if a client had no MMRS.

Any source material included in this document has been sourced from providers that Milliman AU believe to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by any company in the Milliman group as to the accuracy or completeness of the source material or any other information in this document. Logos or names of companies that Milliman AU has partnered with for the development of products using MMRS have been reproduced with the consent of those companies but must not be taken to be a recommendation by those companies with respect to MMRS.

Past performance information provided in this document is not indicative of future results and the illustrations are not intended to project or predict future investment returns.