Big market timing calls can make or break reputations–and businesses. Few get it right, but that doesn’t stop many from trying.

Whenever market valuations seem to be getting stretched, various active managers will make market timing calls. More recently, Altair Asset Management returned all its Australian equity funds to investors and RBS warned investors to “sell everything” in early 2016, while prominent investors including Stan Druckenmiller, Carl Icahn, George Soros and Bill Gross have built their reputations with significant market calls.

It’s a commendable decision whenever active investors, particularly those with skin in the game, put integrity ahead of short-term fee income.

If their predictions prove right and the market suffers a major correction, they’ve potentially made a significant name for themselves and will enjoy fund inflows. However, if the market continues to march higher over the coming years, their reputations may suffer.

While markets have certainly run hard to date, many investors are still predicting that the valuation of global asset prices can remain at current levels or travel higher.

Does this mean they lack integrity? Hardly. No, that’s what makes a market.

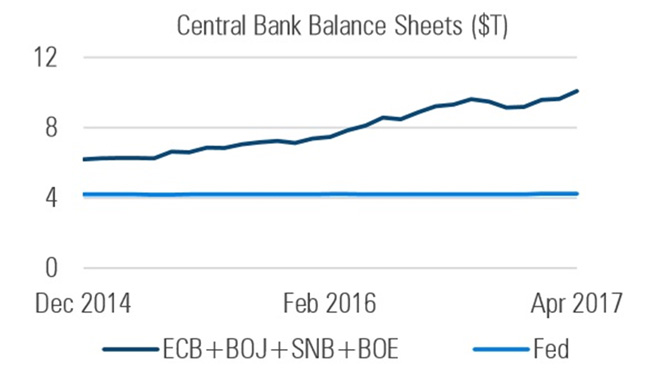

Almost a decade on from the global financial crisis, many developed economies remain at an unusual juncture. Despite an uneven pickup in global growth, markets are still being underpinned by a wall of central bank money.

The US Federal Reserve’s quantitative easing program ended in December 2014 but, since then, the central banks of Europe, Japan, Switzerland and England have grown their balance sheets by 65% in aggregate.

In 2017, they have added a further US$1 trillion in assets bringing their total debt to US$10.3 trillion–it shows just how far the world has to go to revert to “normal”.

Figure 1

Source: Milliman FRM Insight April 2017 Market Commentary

The impact that the end of central bank support will have on markets is impossible to predict as is the impact of rising geopolitical risks around the world. Markets have ups and downs, but history shows timing those changes isn’t consistently possible-however much sense they make in hindsight.

Investors who acknowledge the difficulty of timing markets or super funds that are constrained from making such sweeping market calls and de-allocating from equity markets need to consider other options to manage risk.

A dynamic exposure management strategy utilising exchange-traded equity index futures is one low-cost risk management strategy that has proven to be effective.

Hedge assets can act independently of an underlying portfolio, allowing investors to retain exposure to the bulk of the market’s upside while softening the impact of volatility and market corrections when necessary.

These types of strategies allow investors to continue to reap returns while markets remain strong–unlike those who get their market timing calls wrong.

Recently, most developed equity markets have continued to perform strongly, reaching new “all-time highs” while volatility has been particularly subdued. The three-month volatility of the S&P Global 1200 Index touched a new 10-year low in April 2017.

In this environment, managed risk strategies have generally employed their maximum equity allocations and enjoyed strong returns. But at the same time, these “always on” rules-based approaches have been monitoring and analysing volatility and capital preservation positions standing ready to adjust exposure to risk as markets dynamics determine.

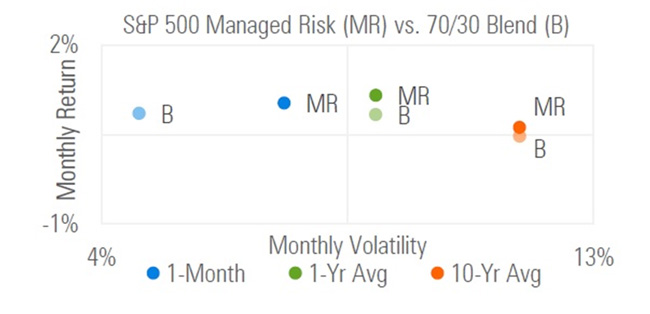

Over the long term, managed risk strategies have shown their worth.

The S&P 500 Managed Risk Index has delivered an average annualised return 1.09% above a 70:30 blend over the 10 years ended April 2017. During that time, its volatility was 200 basis points lower than the 70:30 blend with half the maximum drawdown.

Figure 2

Source: Milliman FRM Insight April 2017 Market Commentary

However, after so many years of market gains, many investors have become complacent about risk while others have started making big calls about the end of the market cycle.

Only time will tell who is correct in both the near term and long term. A managed risk strategy is a prudent middle-ground approach that can manage the potential downside while still allowing investors to participate in the bulk of the market’s upside.

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.