Self-managed super fund (SMSF) investors are an anomaly in the Australian market.

On average, investors are older and wealthier and exhibit far more control over their decisions than others in the $2.1 trillion super industry.

This also makes them prime candidates for sequencing risk: the devastating impact of poor investment performance that strikes at just the wrong time.

But do SMSF investors’ real-world portfolios actually exhibit sequencing risk or do they, on average, strike the right balance between risk and return?

We have conducted a high-level analysis running thousands of simulated scenarios using a simple portfolio to replicate the average SMSF based on clients of administrator Multiport.

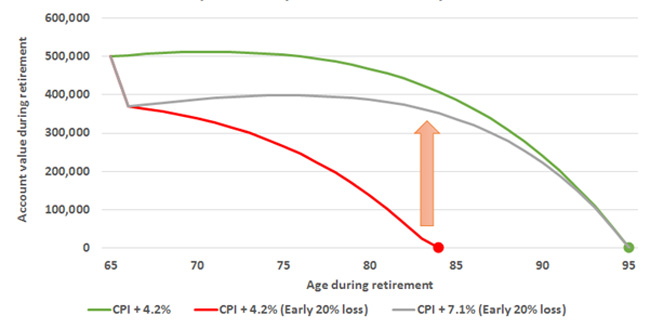

This analysis shows that a typical SMSF portfolio has a one in 12 chance of experiencing a double-digit drop in the first year (at least 10% compared with the expected CPI + 4.2%), which would strip eight years from a pension. The following diagram shows the impact of an even larger 20% loss, which causes the nest egg to deplete 12 years sooner.

Figure 1: Impact of early loss on retirement plan

Source: Milliman analysis of a hypothetical 65-year-old retiree with a $500,000 portfolio withdrawing at an initial rate of 6% and then adjusted for 2.5% inflation thereafter over a 30-year retirement. The 20% drop is assumed to occur over the first year with the following 29 years yielding a return of CPI+4.2%. The CPI+4.2% value is formulated to be the minimum rate of return in order for the retiree’s assets to be not depleted by the end of 30 years.

This is sequencing risk in action–the heightened risk that an investor with a large balance approaching retirement, or in retirement and drawing down a pension, faces.

Younger investors have time on their side. They are often making contributions (rather than withdrawals) and can benefit from an eventual market rebound. Older investors don’t.

If our investor lost 10% in the first year of retirement, he would need to outperform inflation by 5.9% a year for the subsequent 29 years (as opposed to the original target of inflation plus 4.2%) to make up for the impact of the downturn.

Alternatively, he would need to reduce his lifestyle by cutting withdrawals or face running out of money.

| First year | Required return in subsequent years | ||

| Fall in year 1 | Likelihood | 6% withdrawal for 30 years | 8% withdrawal for 20 years |

| 2.5% | 1 in 2 chance | CPI + 5.1% | CPI + 6.1% |

| 5.0% | 1 in 3 chance | CPI + 5.3% | CPI + 6.5% |

| 10.0% | 1 in 12 chance | CPI + 5.9% | CPI + 7.3% |

| 15.0% | 1 in 25 chance | CPI + 6.5% | CPI + 8.2% |

| 20.0% | 1 in 30 chance | CPI + 7.1% | CPI + 9.1% |

There are some important caveats with this analysis because it uses a portfolio split between growth (62.5%) and defensive (37.5%) assets. A typical Multiport portfolio can be viewed as roughly 50% equities, 30% defensive assets and 20% property (the actual figures were 54.1% equities, 30.3% cash and fixed interest, 20.8% property and 0.6% other at December 31, 2015).

However, tracking the true performance of property is problematic: monthly data of residential property prices dampens volatility while listed real estate investment trusts (REITs) adds equity-like volatility. This property data also doesn’t stretch back as far as other asset classes.

While actual SMSF property investments are highly concentrated, leading to highly individual performance, including property index data would likely dampen volatility and risk.

However, this expected benefit is also offset by one of the strongest fixed income bull markets in history during the same period–can investors expect to continue reaping these benefits in the future? Diversification within asset classes with high duration risks, including real estate, infrastructure and credit, will face headwinds in a rising rate environment.

There are some early signs that the bond rally propelled by central banks’ quantitative easing (QE) policies may finally be ending. Markets had already been factoring in a slowdown in central bank QE programs before the surprise November 8 election of Donald Trump, which again boosted inflation expectations.

The Bloomberg Barclays Global Aggregate Total Return Index (Unhedged USD) lost approximately 6.6% between September 26 and November 18, 2016, while other yield-producing assets, such as REITs, have also been sold off.

There are two other factors to consider.

First, the diversification benefits of bonds have been greatly reduced thanks to central bank quantitative easing policies, which have driven yields down to extreme low levels and into negative territory in some cases.

Second, bonds have had extended periods where they have not provided diversification and instead moved in tandem with equities, particularly during times of stress. Prior to 1990, there were long periods where bonds and equities were positively correlated.

The challenge faced by older investors and retirees remains the same: they need growth to fund their increasing lifespan but can't tolerate substantial volatility or losses. While many SMSF investors hold significant cash rather than bonds, interest rates remain at historic lows.

Constructing sound portfolios which can manage heightened risk while delivering returns is a key challenge. Explicit risk management strategies that include capital protection utilising simple exchange traded instruments are a new but effective part of retail investors’ toolkits.

Relying on historical asset class diversification, which may not hold up in the future, remains a strategy fraught with risk.