A gap event is a rare but disturbing phenomenon.

The Brexit vote was a classic example–when Britons unexpectedly voted to leave the European Union in June 2016, some major equity markets fell between trading periods. Investors woke to find sharply lower prices the next morning.

While most quickly recovered in the following days, other historical gap events have been less predictable, introducing periods of volatility which flowed into extended downturns.

The S&P 500 has posted 34 gap events (defined as a greater than 5% difference between the intraday low with the prior day’s market close) over the 50 years ended July 2017. That represents just 0.27% of trading days, but some were unforgettable such as the near 25% single-day fall on 20 October 1987.

While most exchanges now implement circuit breakers to prevent falls of that size, the chance of sudden intraday falls of more than 5% still exceeds some investors’ risk tolerance.

The challenge: High costs and poor timing

Investors using put options to protect against gap risk face significant challenges. It’s expensive to maintain ongoing protection, difficult to time and often doesn’t pay off.

Meanwhile, put spreads and deep out of money option purchases still leave many portfolios significantly exposed to gap events.

For example, consider a gap event of 10%. A hypothetical investor has bought a three-month 97%/90% put spread at the top of the market with a cost of 1.5% (6% to run annually). This strategy would still leave the portfolio participating in 45% of the market fall at expiry.1

However, if the gap event were 20%, this strategy would leave the portfolio exposed to 72.5% of the fall (both assuming the strike was from the top of the market) at expiry.2

The level of instantaneous gap protection is highly variable and heavily dependent on where the option was struck and the remaining tenor.

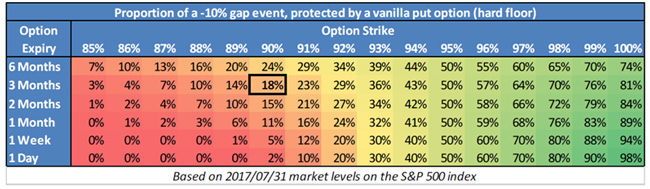

‘Hard floor’ style option structures can be useful but are also expensive. The following table shows a simplistic vanilla put option (marked-to-market representing the ‘hard floor’) and the level of protection against a -10% gap event. Highlighting, the level of protection is determined by several factors, including strike level and time remaining to expiry.

For example, holding a three-month 90% put option will generate 1.8% return on the notional–or provide just 18% protection against the gap event (assuming the option notional amount was equal to the underlying holding). If markets trend lower as the option matures, then the hard floor will pay off. However, markets have historically recovered quickly after large drawdowns.

Within a risk management strategy utilising physical options, option strike levels are usually determined arbitrarily by time. The arbitrary nature of the strike level (in spreads and out right purchases) adds uncertainty about the level of protection.

We have previously shown the high cost and difficulty in timing protection with put options by analysing three hypothetical investors in the US, UK and Eurozone looking to protect their end-of-May portfolio values against a Brexit-related selloff.

Managed risk: Assessing an alternative strategy

While options, swaps and swaptions offer benefits, they also bring challenges. Ongoing option protection strategies are less efficient and do not necessarily protect portfolios more than dynamic hedging strategies.

The Milliman Managed Risk Strategy™ (MMRS) has a cash buffer and uses hedge assets (typically exchange-traded futures contracts) to preserve capital and manage volatility during periods of market turbulence.

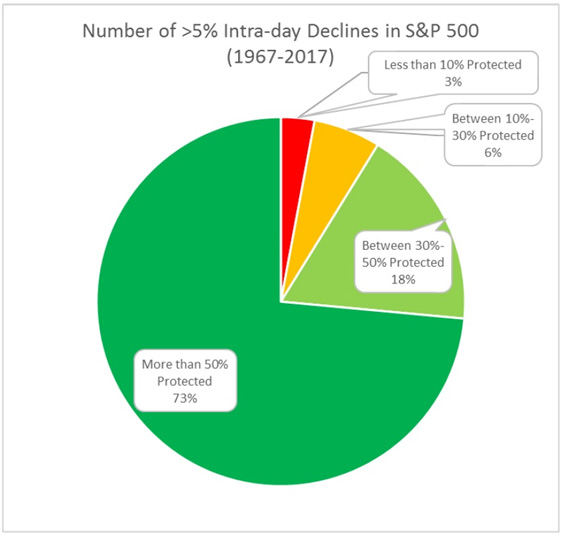

This means the strategy aims to consistently offer some protection against gap events. The following chart shows the level of protection offered by the managed risk strategy applied to an S&P 500 portfolio over the same 50-year period. It provided protection against more than 50% of the portfolio more than 73% of the time.

This relatively high level of protection occurs because gap events typically strike during periods of high volatility or sustained market drawdowns–this is when managed volatility and managed risk strategies offer the highest level of protection.

This is not a discretionary decision based on a qualitative assessment of market conditions, which can leave some option-based strategies exposed, but a pre-determined rules-based response to quantitative market data.

Milliman also minimises the period in which a gap event can occur by relying on three trading desks covering all major markets, including (where appropriate) night sessions offered by most major future exchanges and ongoing contact with most major brokers. This allows our traders to respond quickly and appropriately as market events happen rather than waking up to a gap event.

There are no simple answers to protecting portfolios against gap risk, but a careful assessment of the strategies at hand will ensure the most efficient and cost-effective approach.

For more information about derivate strategies, please contact Milliman head of fund advisory services Michael Armitage at [email protected].

1In a 97%/90% put spread, the long strike at 97% leaves 3% of the portfolio out of the money. With a cost of 1.5%, this would mean that the portfolio would participate in 4.5% of the 10% market fall, which is equivalent to 45% participation of the fall.

2In a 97%/90% put spread, the long strike at 97% leaves 3% of the portfolio out of the money and limits protection to the level of the short strike of 90%. With a cost of 1.5%, the investor would participate in 4.5% of the first 10% fall and would fully participate in the additional 10% fall. This would mean the portfolio would participate in 14.5% of the 20% market fall, equivalent to 72.5% participation of the fall.

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

These results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown. Milliman does not manage the underlying fund.

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.