On February 9, 2018, Congress passed the Bipartisan Budget Act of 2018. The bill enacted key changes to the Medicare Part D program that will impact the “donut hole” starting in 2019. This paper discusses the implications for stakeholders.

Overview

The Bipartisan Budget Act of 20181 institutes three key changes to Medicare Part D’s “donut hole” (Coverage Gap) for applicable beneficiaries,2 effective January 1, 2019:

1. Closes the coverage gap one year early for applicable drugs,3 reducing standard beneficiary cost sharing in that phase from 30% to 25%

2. Increases pharmaceutical manufacturers’ discount in the Coverage Gap Discount Program (CGDP) from 50% to 70% of the negotiated price of applicable drugs,4 resulting in lower costs to Part D plan sponsors

3. Removes the exclusion of certain biosimilars5 from the CGDP, eliminating a significant impediment to biosimilar adoption by Part D plan sponsors

The bill provides standalone prescription drug plans (PDPs) with Parts A and B medical claims to promote appropriate medication use and better health outcomes. The bill also funds the study of the impact of obesity drug use on patient health and spending.

This white paper focuses on the implications of the coverage gap changes to Part D stakeholders, including beneficiaries, pharmaceutical manufacturers, the federal government, and plan sponsors.

Part D sources of funding

Part D benefits are funded by four stakeholders:

- Beneficiaries, through premiums and cost sharing (deductibles and copays/coinsurance)

- Employers, through their payment of premiums and non-Medicare supplemental drug (“wrap around”) coverage for retirees in Employer Group Waiver Plans (EGWPs)

- Pharmaceutical manufacturers, through the CGDP for applicable beneficiaries and drugs filled in the coverage gap6

- The federal government (taxpayers), through direct subsidies and risk sharing to plan sponsors, cost sharing and premium subsidies for low income beneficiaries, and reinsurance for catastrophic spending

Plan sponsors are also stakeholders that are affected by these coverage gap changes, with the plan liability being funded through government subsidies and beneficiary premiums.

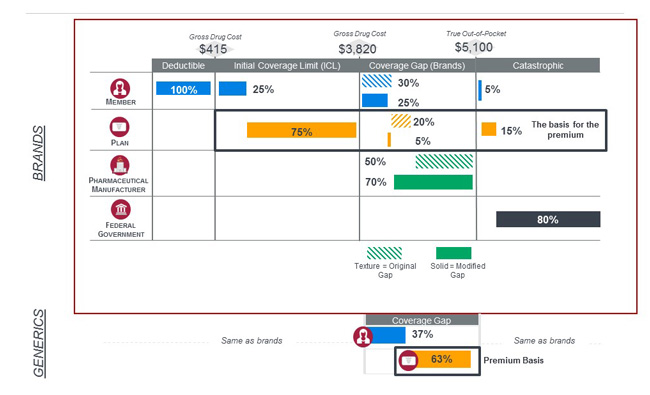

The Part D phases of coverage determine the share of spending for each of the stakeholders on every script. Figure 1 shows the original and proposed standard benefits for applicable beneficiaries and drugs.

Based on the Advance Notice released February 1, 2018, we expect that in 2019 beneficiaries will enter the coverage gap after accumulating $3,820 in total drug cost, and will move to the next phase, catastrophic, once their true out-of-pocket (TrOOP) expenses reach $5,100.7

Figure 1: Draft 2019 original and modified Medicare Part D standard benefits for non low income beneficiaries

What do these changes mean to stakeholders?

Figure 2 summarizes our estimate of the incremental CY 2019 impact of these changes for each of the major stakeholders:

Figure 2: Cost impact to Part D stakeholders for individual and EGWP markets in 2019 ($ billions)*

| Stakeholder | Individual | EGWP | Total |

| Beneficiaries1 | $ (0.6) | $ (0.7) | $ (1.3) |

| Fed government | $ (0.5) | $ (0.1) | $ (0.6) |

| Pharma | $ 1.1 | $ 0.8 | $ 1.9 |

| Total | $ 0.0 | $ 0.0 | $ 0.0 |

| * Estimates assume no changes in stakeholder behavior | |||

| 1Includes retirees in EGWPs and their employers, who pay a share of the premium. | |||

The following describe the impacts to each of the stakeholders.

Beneficiaries and employers

We expect these coverage gap changes will reduce premium for all beneficiaries in 2019 relative to previous expectations for 2019 premiums. We expect employers sponsoring EGWPs to see a reduction in premiums for both standard and wraparound benefits in 2019. Applicable beneficiaries will also benefit from lower cost sharing in the coverage gap for both brands that are currently eligible for the CGDP as well as biosimilars newly eligible for the program.

In addition, we expect applicable beneficiaries to reach catastrophic faster in 2019 as the manufacturer discounts accumulate towards TrOOP. For applicable scripts filled in the coverage gap, the portion of spending that counts towards TrOOP increases from 80% to 95%.

The inclusion of biosimilars in the CGDP may cause some beneficiaries to see their reference products removed from the formulary in favor of the biosimilar. However, we expect this to have little financial impact in the short-term due to the lack of biosimilars available for popular biologic reference products geared toward the Part D population.

Pharmaceutical Manufacturers

The bill will result in lower revenues to the pharmaceutical industry, specifically to manufacturers of CGDP-eligible drugs. Some manufacturers with biosimilar competition may see their products removed from formularies sooner as the plan sponsor liability in the coverage gap will be the same for both products. On the other hand, manufacturers of biosimilars may see improved formulary access.

Federal government

We estimate that the bill will reduce federal spending. We expect some of the lower plan costs to translate into lower direct subsidies to plan sponsors as well as lower beneficiary premiums, which, for low income beneficiaries, are subsidized by the government through a low income premium subsidy (LIPS). However, the higher CGDP payments by pharmaceutical manufacturers, by causing applicable beneficiaries to hit catastrophic sooner, are expected to increase federal reinsurance spending.

Plan sponsors

The changes to the coverage gap will reduce the portion of claims covered by the plans as the 2019 plan liability drops from 20% (as established by the Patient Protection and Affordable Care Act) to 5%. We expect this reduction in plan costs to result in lower bids, likely translating into lower government subsidies to plan sponsors and lower beneficiary premiums.

Plan sponsors will also have an increased incentive to include biosimilars on their formularies, although in the short-term we expect this will have little financial impact due to the lack of biosimilars available for popular biologic reference products geared toward the Part D population.

What is next?

While the near term implications of the Part D provisions in the funding bill are fairly clear, it is less certain what behavior changes may occur or what avenues for program reform may open as a result of the legislation. Some possibilities include:

1. Exacerbation of the high price/high rebate incentives in Part D. The reduction of plan liability in the coverage gap reduces the plan liability associated with higher cost drugs. This, combined with current manufacturer rebate levels, creates an environment where plan sponsors can achieve a lower net plan liability by favoring use of higher priced brand drugs compared to lower priced brands or generics. This dynamic, addressed by MedPAC and the Centers for Medicare and Medicaid Services (CMS) in their 2017 proposals8,9 is intensified with the lower plan liability in the coverage gap.

2. Direct and indirect remuneration (DIR) shifts toward government reinsurance and away from plan liability. The revised Part D benefits are likely to cause an increase in the share of spending in Catastrophic. This can lead to a smaller share of DIR amounts reflected in plan liability.

3. End to enhanced gap coverage for brands. While few Part D plans offer meaningful enhanced gap coverage for brand drugs today, the coverage gap changes may further reduce the benefit of providing enhanced gap coverage for brand drugs. When plans offer reduced or alternative cost sharing in the coverage gap, the percent of spend paid for by manufacturers is applied only to the beneficiary’s cost sharing with plans responsible for the remainder. Plans will be less likely to give up 70% of the cost of the drug. The law also disincentivizes plans from charging a fixed dollar copay instead of the standard coinsurance in the gap.

4. Manufacturers’ re-evaluation of rebates. The 70% discount may be particularly challenging to manufacturers of brand drugs in therapeutic classes where rebates above 30% are common (such as certain medications that treat chronic conditions). For these brand drugs, each fill in the coverage gap will result in losses to the manufacturer, which in turn may try to offset the reduced margins though higher prices or lower rebates. Either of these actions would result in increased Part D program costs.

5. Impact of TrOOP cliff. In 2020, the TrOOP is expected to jump by approximately $1,200.10 The impact to beneficiaries will be mitigated because they will move through the coverage gap faster (due to applicability of additional CGDP dollars toward each applicable beneficiary’s TrOOP). However, manufacturers will have to pay up to an additional $840 for each applicable beneficiary that makes it to Catastrophic.

6. Manufacturers may increase focus on development and patent litigation of biosimilars, given the removal of the market disadvantage biosimilars previously had in the Part D market.

7. Increased adherence, which may improve health outcomes for patients taking high cost medications–both due to immediately reduced cost sharing in the coverage gap and the faster journey to Catastrophic where applicable beneficiaries pay 5% coinsurance instead of 25%. This may lead to increased sales for some manufacturers but is unlikely to materially offset the additional costs of the CGDP.

In summary, the Bipartisan Budget Act of 2018 reduces beneficiary and government funding for Part D while increasing costs to manufacturers. However, these changes may be just the beginning. Several proposals by MedPAC and CMS (such as the phasing in of a reduction of Part D reinsurance, from 80% to 20%, or the application of rebates at the point-of-sale)11 aim to adjust the incentives in Part D. This bill may act as a catalyst to further reform in the Part D program.

Methodology and data sources

We developed the financial impact of the Bipartisan Budget Act of 2018 to Part D stakeholders using Milliman pricing models. The models were calibrated to the 2018 national average bid and premium amounts and trended to 2019. We assumed the draft defined standard benefits for 2019 as the starting point, and modified the benefits to reflect the changes introduced by the bill. The total dollar impact was then applied to the 2019 membership projections from the 2017 Medicare Trustees report.12 We have not modeled the impact of biosimilars becoming eligible for the CGDP; we estimate its impact to be negligible in 2019 due to the small spending on biosimilars in the Part D market. While our estimates include the impact of induced utilization due to lower beneficiary cost sharing, we have assumed no formulary changes or other behavior changes.

Caveats

The figures presented here represent national averages. Results for any particular stakeholder may vary substantially from those presented here due to demographics and other factors. Certain types of benefit programs, in particular EGWPs, may see different dynamics due to the interplay of Part D benefits and wraparound coverage.

Contact

If you have any questions or comments on this paper, please contact:

Adam Barnhart

[email protected]

+1 262 796 3428

Gabriela Dieguez

[email protected]

+1 646 473 3219

David Mike

[email protected]

+1 262 796 3414

The American Academy of Actuaries requires that its members identify their credentials in communications. The authors meet the Academy’s qualification requirements to issue this report.

1 https://www.ssa.gov/OP_Home/ssact/title18/1860D-14A.htm, section 1860D–14A(g)(1)

2Applicable beneficiaries are those not qualifying for low income subsidies, permitting them access to the coverage gap discount program.

3Applicable drugs are Part D covered brand products, with some generic exceptions, as specified in Chapter 5 of the Medicare Prescription Drug Benefit Manual.

4 https://www.ssa.gov/OP_Home/ssact/title18/1860D-14A.htm, section 1860D–14A(g)(2)

5For biologics approved under subsection (k) of section 351 of the Public Health Service Act.

6 https://www.ssa.gov/OP_Home/ssact/title18/1860D-14A.htm, section 1860D–14A(g)(1)

7 https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/Advance2019Part2.pdf, page 52

8 http://medpac.gov/docs/default-source/reports/mar17_entirereport.pdf, page 404

9 https://www.federalregister.gov/documents/2017/11/28/2017-25068/medicare-program-contract-year-2019-policy-and-technical-changes-to-the-medicare-advantage-medicare

10 http://www.ajmc.com/journals/supplement/2017/beyond-charitable-assistance-sustainable-strategies-for-providing-access-to-critical-medications/reducing-out-of-pocket-cost-barriers-to-specialty-drug-use-under-medicare-part-d?p=2

11 http://www.medpac.gov/docs/default-source/comment-letters/01032018_partc_d_comment_v2_sec.pdf?sfvrsn=0

12 https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2017.pdf