Escalating challenges from recent wildfires and the implications for insurers and homeowners

As recovery and investigative crews continue to comb through the wreckage of California’s Camp Fire and homeowners set their sights on moving forward, public attention has turned to the insurance implications of such a destructive few years of wildfires in the state.

November’s Camp Fire, near Paradise in northern California, has already topped the Tubbs Fire of 2017 as the most destructive wildfire in California history, with at least 77 confirmed deaths and 15,850 structures destroyed as of this writing.1 This past July, the Mendocino Complex Fire burned through more land than any other wildfire in state history, at 459,123 acres, eclipsing the 281,283 acres burned from the Thomas Fire of 2017.2 California’s governor, Jerry Brown, has called this year’s wildfire activity “the new ‘abnormal,’” after the state’s largest, deadliest, and most destructive fires on record occurred in 2018.3

If the recent pattern of California’s escalated wildfire severity persists, there could be significant implications for insurers’ willingness to adequately cover wildfire losses in the state as well as for homeowners’ ability to find and afford coverage. This article examines some of the fundamentals of wildfire risk, including the effect on insurers, homeowners, and the overall implications for the property insurance market in California.

The new (ab)normal?

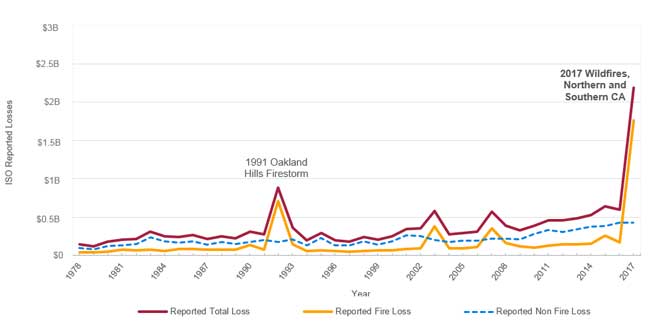

The calendar year 2017 was an unprecedented time for wildfires in California. According to Milliman’s estimates, losses incurred by insurance companies in the 2017 wildfire season could rival the combined losses of the entire 39-year period that preceded it (Figure 1).

Figure 1: Estimated California Wildfire Insurance Losses by Year

Source: Insurance Services Office (ISO), 2017 estimate from Milliman. ISO experience represents data from approximately 20% of the insurance industry

Despite the high level of wildfire destruction in the state over the past two years, it is not clear what Californians should expect in the future. Contributing factors to wildfire risk may include, at varying levels, environmental conditions such as drought and climate change, and human factors such as urban development and maintenance of the power grid. Some factors like drought may be cyclical, where risk to the state depends on climate conditions of the past several years. Other factors, such as anthropogenic climate change, could increase wildfire risk for decades (for a more detailed look at wildfire risk, see the sidebar, "How to Evaluate Wildfire Risk").

How to evaluate wildfire risk

A number of factors cause or mitigate wildfires and, accordingly, must be assessed in analyses of wildfire risk.

Climate is a major contributor to California wildfires in a variety of ways:

- The state’s Mediterranean climate is characterized by hot, dry summers and cool, moist winters, both of which enhance the accumulation of wildfire fuels such as decomposed vegetation.

- The lack of precipitation in recent years—the state experienced an extreme drought from 2010 through 2016—helped to dry out forests and other landscapes whose previous moisture levels would normally serve as barriers to flammability. Climate change, moreover, may exacerbate the severity of droughts.17

- The famed Santa Ana and Diablo winds, which originate inland and blow downslope toward the California coast, are notoriously warm, dry, and strong—and have fanned the flames of wildfires for decades.

Proximity to wildfire-prone areas known as the wildland-urban interface (WUI) is a growing concern throughout the United States, as about one-third of the national population lives in WUI locations.18 An increasing number of communities have been built in the WUI over the past few decades in the United States.19 In 1964, the Hanly Fire burned through a sparsely populated area in northern California, destroying only a few dozen homes.20 Fast-forward 53 years: the 2017 Tubbs Fire, following a similar footprint as the Hanly Fire, destroyed thousands of homes in the now densely populated Fountaingrove area of Santa Rosa.

Topography is a primary contributor to fire behavior. Natural features such as rivers and lakes, and man-made features such as roads and highways, serve as firebreaks that impede the spread of a wildfire. Other terrain features such as slope, aspect, and elevation can affect fuel moisture, the rate of fire spread, and the direction of fire spread.

Active prevention strategies can help property owners to mitigate wildfire risk and, potentially, reduce their insurance premiums.21 Commonly suggested strategies include:

- Creation of defensible spaces around dwellings by clearing brush and vegetation

- Use of fire-retardant materials and more robust home construction methods

- Use and placement of firebreaks to slow the spread of wildfires

- Assessing whether exit and entry routes provide ready access for firefighters

Without question, the recent wildfire destruction has had a devastating effect on individuals and businesses across the state, and has had a major impact on property insurers as well. Due to an extraordinary outbreak of major wildfires in the fourth quarter of 2017, insurers suffered wildfire losses of $12 billion in calendar year 2017—the largest amount of such losses on record since the 1991 Oakland Hills Firestorm, which would have cost $2.8 billion in 2017 dollars.4 In 2018, the California Department of Insurance (CDI) estimates that commercial and residential property losses from both the Carr and Mendocino Fires will top $845 million,5 while losses from the Camp Fire (expected to be California’s costliest in state history) and Woolsey Fire are currently estimated between $9 billion and $13 billion.6

The insurance implications of these losses are still developing. Anecdotal news reports indicate that some insurers' homeowner policies have not been renewed in areas identified as having the highest fire risk.7

Comprehensive data on nonrenewals isn’t available yet, but recent metrics make it clear that the practice may have been growing leading up to the 2017 wildfires, and that it is having an impact on consumers. According to a California Department of Insurance report:8

- Nonrenewals in the 24 highest-risk counties rose 15% in 2016 from 2015.

- The number of annual homeowner complaints about nonrenewals in the highest-risk ZIP Codes rose 249% between 2010 and 2016.

In response, California signed into law a number of proposals related to wildfire safety, prevention, and recovery, including the following measures intended to address insurance issues:

- SB 824, sponsored by California insurance commissioner-elect Senator Ricardo Lara (D), prohibits insurance companies from canceling or non-renewing homeowners policies for a year in counties that have faced a declared state of emergency.

- SB 894 permits those impacted by a disaster to combine limits for dwelling, and other structures on their insurance policies in the event that the dwelling policy limits alone are insufficient. In addition, the bill requires insurers to provide up to three years of living expenses as policyholders rebuild their homes, and requires the insurer to offer to renew affected policy for at least the next two renewal periods under certain circumstances.

- AB 1772, AB 1800, AB 1875, and AB 2594 have also been passed in California to address issues faced by survivors of wildfires.9

Given what we’ve seen recently, California legislators will likely face continued pressure from both consumer and industry groups to put forth solutions that will help combat the risk resulting from increased wildfire severity in the state.

Wildfires vs. hurricanes: An instructive comparison

It may be that wildfires are to California what hurricanes are to Florida. Both perils are the subject of continuous concern not only for insurers and policyholders, but also for their respective state governments as well. In addition, both California and Florida have “insurance of last resort” programs to keep disaster coverage available and reasonably affordable to residents who otherwise wouldn’t be covered.

But the similarities end with a fundamental difference: 84% of wildfires are caused by human activity.10 In other words, many wildfires are preventable, while hurricanes are not. The economic losses from California’s two major wildfires in October 2017 are estimated to comprise two-thirds of the economic costs for wildfires globally in all of 2017.11 In light of that fact, Benjamin Franklin’s axiom, “An ounce of prevention is worth a pound of cure,” may have increased resonance for wildfires.

Another stark contrast between California wildfires and Florida hurricanes is that Florida has developed a far more robust scientific and legal framework to deal with hurricane risk. Grounded in science and engineering, catastrophe models have been developed during the past few decades to assist insurers in pricing and managing risk for hurricane coverage. In 1995, Florida created the Florida Commission on Hurricane Loss Projection Methodology (FCHLPM), comprised of a panel of experts in the fields of insurance, statistics, engineering, and meteorology. Under state statutes, insurance companies are only permitted to use catastrophe models that have passed the muster of the FCHLPM.

By contrast, California insurance law for property insurance as dictated by Proposition 103 remains primitive. Insurance companies are prohibited from using wildfire catastrophe models to set overall prices, and must use historical averages instead. This has the potential to lead to pricing that is not fully reflective of actual risk, and insurance companies may be reluctant to insure policies in wildfire-prone locations within the state. On the other hand, wildfire risk models have been permitted by the CDI for risk differentiation and underwriting purposes, but there are no laws or panel of experts in place to ensure model accuracy or reliability for risk differentiation. On the underwriting front, there are no laws permitting the CDI to regulate underwriting rules of insurance companies.12 The CDI unfortunately simply doesn’t have the statutory authority to do more.

Third-party catastrophe models, when properly regulated, are a more sophisticated and granular method for pricing insurance than what is currently in use in the state. If California were to permit the use of (and regulate) these wildfire catastrophe models similar to what Florida has done for hurricanes, it would be a positive step toward establishing more risk-based, accurate prices for homeowners and would likely help stabilize what is becoming a volatile property insurance market in the state.

The California wildfire conundrum

At the heart of the issue is the reality that insurers’ hands are tied in the face of potentially rising losses. After past catastrophic wildfires, the California Insurance Commissioner has been known to request that insurance companies expedite claims handling, which can potentially lead to inaccurate payments of claims.13 As wildfire activity escalates, insurance companies are also at higher risk of being involved in litigation over a variety of issues, including claims handling, policy contract language, and subrogation against other parties. In addition, reinsurance prices may rise for insurance companies post-catastrophe, and California regulation prohibits insurance companies from including the cost of reinsurance in premiums—a practice fully permitted in Florida.

Faced with such threats to profitability, insurers have few options. They could limit their exposure to new policies in certain areas, stop writing new business entirely, or as the most extreme scenario, exit the state. The latter possibility could be hugely disruptive, as California’s top 10 property insurers control three-quarters of the market.14 The departure of big players would leave mostly smaller players with less experience and capacity, potentially exacerbating the existing availability problem. However, a major exit from the California market is not likely to be imminent. If such an extreme situation were to occur, we expect that it would develop over the course of many years.

One answer to the availability problem is the California Fair Access to Insurance Requirements Plan (FAIR Plan), which was created in 1968 in response to wildfires and riots during the '60s. Through the FAIR Plan, consumers can obtain bare-bones dwelling insurance coverage that they would otherwise be unable to find in the voluntary market. It is important to note that a FAIR Plan policy only includes coverage for a limited number of perils such as fire and lightning; other common homeowners insurance perils such as wind and water are excluded from coverage. Many major carriers now offer Difference in Conditions (DIC) policies, which are full homeowners policies that exclude coverages offered by the FAIR Plan.15 Insurers are more likely to be willing to write DIC policies in wildfire-prone areas, especially as fires are not covered.

In reality, the FAIR Plan is not a single insurer. As a condition of their participation in the California property insurance market, all voluntary insurers must share in the losses, profits, and expenses of the FAIR Plan, proportional to their respective market shares. This is a key feature of the FAIR Plan: no taxpayer money is involved, and it is financially backed by the strength of the entire California property insurance industry.16 Even with increasing policy cancellations, the industry still has to foot the bill to cover high wildfire risk, albeit indirectly. Interestingly, FAIR Plan prices are not dictated by Proposition 103, and therefore the incorporation of wildfire catastrophe models and reinsurance prices in setting overall rates is not disallowed by the CDI. This inconsistent treatment results in a dynamic in which a state residual market program can potentially price for wildfire risk more accurately than voluntary private insurers are permitted.

Ultimately, California regulators, insurers, and policyholders are all “stuck” until insurance laws change. Insurance companies facing mounting profitability issues may have no recourse but to attempt to raise rates in high-risk areas, or to tighten their belts around underwriting of high-risk policies. Consequently, policy cancellations and nonrenewals may persist in higher numbers. In addition to solving a wide variety of issues related to wildfire prevention and mitigation measures, legislators may consider regulating third-party wildfire models and permitting their use in insurance pricing, and permitting the inclusion of reinsurance costs in premiums, similar to Florida’s regulations around hurricane risk. While this could help shore up the property insurance market in California, it’s worth noting that such a proposal may be unpopular with some policyholders and consumer advocate groups as pricing that is more reflective of actual wildfire risk would result in higher rates for some homeowners.

Looking ahead, whether the recent increased wildfire activity is the “new normal” or not, it’s important for consumers, insurers, and legislators to be educated on the issues surrounding wildfire risk. Understanding the escalating challenges and implications for all stakeholders enables decision-makers in the state to legislate effectively if and when the severity of this wildfire season provides the fuel for government to act.

1California Department of Forestry and Fire Protection (November 25, 2018). Top 20 Most Destructive California Wildfires. Cal Fire Statistics and Events, Incidence Information. Retrieved November 27, 2018, from http://www.fire.ca.gov/communications/downloads/fact_sheets/Top20_Destruction.pdf.

2California Department of Forestry and Fire Protection (November 25, 2018). Top 20 Largest California Wildfires. Retrieved November 27, 2018, from http://www.fire.ca.gov/communications/downloads/fact_sheets/Top20_Acres.pdf.

3Birnbaum, Emily (November 11, 2018). California governor on wildfires: 'This is the new abnormal.' The Hill. Retrieved November 27, 2018, from from https://thehill.com/homenews/state-watch/416167-california-governor-on-wildfires-this-is-the-new-abnormal.

4Insurance Information Institute. Facts + Statistics: Wildfires, Retrieved November 27, 2018, from https://www.iii.org/fact-statistic/facts-statistics-wildfires.

5CDI (September 6, 2018). Carr and Mendocino Complex fire insurance claims top $845 million. Press release, Retrieved November 27, 2018, from http://www.insurance.ca.gov/0400-news/0100-press-releases/2018/release106-18.cfm.

6Insurance Journal (November 19, 2018). Latest estimates of insured losses from California wildfires at $9B to $13B. Retrieved November 27, 2018, from https://www.insurancejournal.com/news/west/2018/11/19/509677.htm.

7Adriano, Lyle (July 23, 2018). Liberty Mutual, other insurers start dropping risky clients. Insurance Business America. Retrieved November 27, 2018, from https://www.insurancebusinessmag.com/us/news/catastrophe/liberty-mutual-other-insurers-start-dropping-risky-clients-106678.aspx.

8CDI (December 2017). The Availability and Affordability of Coverage for Wildfire Loss in Residential Property Insurance in the Wildland-Urban Interface and Other High-Risk Areas of California: CDI Summary and Proposed Solutions. Retrieved November 27, 2018, from http://www.insurance.ca.gov/0400-news/0100-press-releases/2018/upload/nr002-2018AvailabilityandAffordabilityofWildfireCoverage.pdf.

9 http://www.insurance.ca.gov/0400-news/0100-press-releases/2018/release117-18.cfm

10Balch, Jennifer et al. (January 6, 2017). Human-started wildfires expand the fire niche across the United States. Proceedings of the National Academy of Sciences of the United States of America. Retrieved November 27, 2018, from http://www.pnas.org/content/114/11/2946.

11Aon Benfield. Weather, Climate & Catastrophe Insight: 2017 Annual Report. Retrieved November 27, 2018, from http://www.aon.com/spain/temas-destacados/Annual-report-weather-climate-2017.pdf.

12CDI, Availability and Affordability, op. cit.

13CDI (August 1, 2018). Expedited Claim Handling Billing Grace Period Procedures for California Wildfires. Retrieved November 27, 2018, from http://www.insurance.ca.gov/0400-news/0100-press-releases/2018/upload/nr086NoticeExpeditedClaimsProcedures.pdf

15CDI. List of Insurers That Sell Difference in Conditions (DIC) Policies. Retrieved November 27, 2018, from http://www.insurance.ca.gov/01-consumers/105-type/5-residential/carriersDICpolicies.cfm. Note that the list is not comprehensive.

16California FAIR Plan Property Insurance. General Information. Retrieved November 27, 2018, from https://www.cfpnet.com/index.php/general-info/.

18U.S. Department of Agriculture. The 2010 Wildland-Urban Interface of the Conterminous United States. Retrieved November 27, 2018, from https://www.fs.fed.us/nrs/pubs/rmap/rmap_nrs8.pdf. Data based on most recent (2010) U.S. census.

19 U.S. Department of Agriculture (March 12, 2018). Areas where homes, forests mix increased rapidly over two decades. News release. Retrieved November 27, 2018, from https://www.nrs.fs.fed.us/news/release/wui-increase.

20Hansen, J. (July 21, 2014). Park agencies, landowners gird for fire season (w/video). Santa Rosa Press Democrat. Retrieved November 27, 2018, from https://www.pressdemocrat.com/news/state/2393494-181/park-agencies-landowners-gird-for.

21California FAIR Plan Property Insurance. Brush/Wildfire Rating. Retrieved November 27, 2018, from https://www.cfpnet.com/index.php/consumers/brushwildfirerating/.