The challenge

The implementation of GASB 45 resulted in a significant increase to the payroll/benefits budget for a public authority that included its annual required contribution (ARC) in the budget. Grant funding received by the authority often requires payroll and benefits to be less than a specified percentage of the total cost of the grant. The large increase in the budget due to GASB 45 could result in the loss of some grant funding.

The goals and constraints of the authority are:

- Maintain the same postretirement benefits

- Reduce short- and long-term costs of the postretirement medical benefits

The solution

The discount rate used to determine the ARC under GASB 45 is based on the funded status of the plan. When determining an appropriate discount rate for valuing GASB 45 liabilities, it is important to note:

- An unfunded plan utilizes a discount rate that is based on the expected rate of return on the general assets of the plan sponsor. General assets of a plan sponsor are often held in cash and other short-term investment vehicles.

- A funded plan where the plan sponsor contributes at least the ARC each year (via a combination of pay-as-you-go benefit payments plus a contribution of the remaining amount to a dedicated trust) can utilize a discount rate that is based on the long-term expected return of the plan assets.

Therefore, funded plans typically use a higher discount rate than unfunded plans because funded plans hold assets that have a higher expected long-term rate of return than a sponsor’s general assets. Higher discount rates produce lower liabilities; conversely, lower discount rates produce higher liabilities.

Milliman worked with the authority to analyze the impact of funding an OPEB trust to meet both their funding goals and subsequent investment targets.

Milliman prepared a study showing the potential decrease in the ARC for funding the ARC using an OPEB trust. The decrease is due to the use of a higher discount rate based on the long-term expected return on the plan (trust) assets instead of the general assets of the sponsor. In addition, the investment returns, along with the authority contributions, will ultimately fund the postretirement benefits.

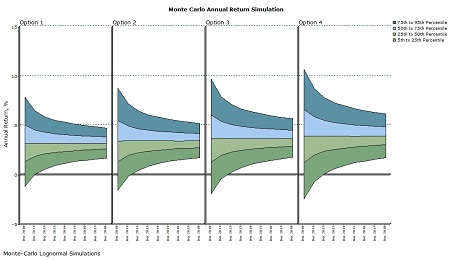

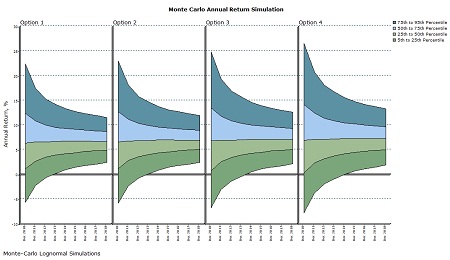

Milliman’s investment consultants developed a series of Monte Carlo simulations to help the authority evaluate different asset allocations for the trust. Monte Carlo simulations run 10,000 “trials” on the proposed asset allocations to find the probability distribution of the expected rate of return. Multiple analyses were prepared, as the authority’s board requested allocations that included and excluded specific types of investments. Following are several charts illustrating the results of the modeling showing the probabilities and ranges of expected returns. These charts show that including domestic equities in the portfolio significantly increases the expected return compared to the portfolio with fixed income only. Additional allocations were illustrated as well for comparison.

Simulation Excluding Equities (Fixed Income Only)

Simulation Including Domestic Equities

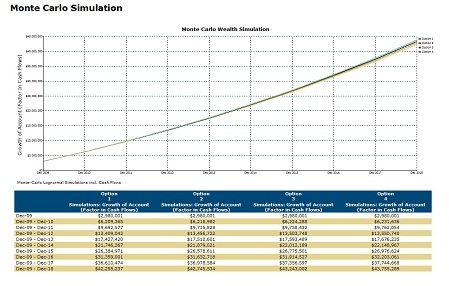

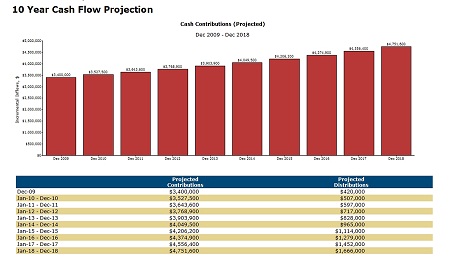

Milliman’s actuaries and investment consultants worked together to review the impact on the ARC of each allocation’s long-term expected return. The actuaries projected the future payouts and contributions which were used by the investment consultant to determine an appropriate cash allocation for liquidity purposes. The following chart illustrates the expected contributions and benefit payouts from the actuarial study.

Milliman’s consultants also worked with the authority’s legal staff to design and review a plan document, trust agreement, and Investment Policy Statement (IPS) for the post-retirement plan.

The outcome

As a result of the study, the authority:

- Entered into a trust agreement with a bank to establish a funded OPEB trust

- Reduced the current net OPEB obligation (NOO) on its financials to $0 by making an initial contribution to the OPEB trust equal to the NOO

- Adopted a funding policy to contribute the ARC each year

- Adopted an investment allocation with a long-term expected rate of return of 6.5%

- Reduced the annual required contribution by over 20% using the higher discount rate supported by the plan’s asset allocation