The challenge:

Our public sector client had developed its funding policy based on reference to the Governmental Accounting Standards Board (GASB) annual required contribution (ARC). As GASB Statements No. 67 and 68 (which eliminate the concept of the ARC) are scheduled to be phased in beginning in 2014, this client looked to Milliman to help design a new funding policy that would stand on its own without reference to the GASB standards, while accomplishing the goals of prudent funding of the system and balancing the intergenerational equity of the payments. Additionally, stability of the long-term contribution rate was a priority for this client.

The solution:

Although the GASB ARC allowed for an amortization of the unfunded actuarial accrued liability (UAAL) over a new 30-year period each year (a method often referred to as a “rolling” 30-year amortization), the recommended approaches today1 typically involve amortizing the UAAL over a closed period of 20 years or less. One potential downside of funding over a strictly closed amortization period is increased contribution rate volatility toward the end of the closed period; if UAAL gains or losses occur during the final years of the amortization, the contribution rate may need significant adjustment in order to continue to pay off the UAAL on schedule.

Our client was concerned about this potential future contribution rate volatility, and wanted to find a balance between prudent acceptable funding and a stable contribution rate over time. We therefore recommended a modification to a strictly closed amortization method, often referred to as a “layered” closed amortization method. Under a layered closed method, the initial UAAL is amortized over a closed period of a specified number of years; in each future year, any gain or loss on the UAAL is amortized over its own closed period of the same number of years. This eventually results in a series of UAAL layers, each of which is being paid off over a fiscally responsible closed period. This helps mitigate volatility in the required amortization payment as the end of the initial closed period approaches, but maintains a true payoff of the UAAL over time.

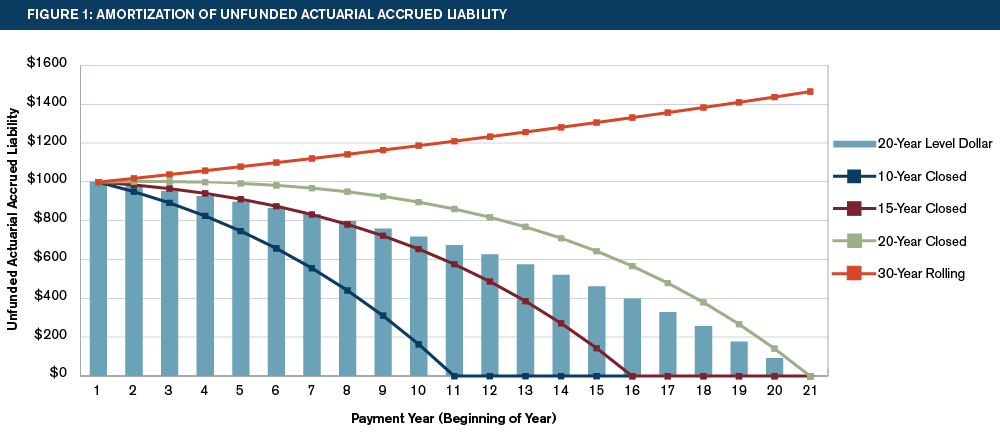

Milliman prepared a projection of contribution rates as a level percentage of payroll for our client to illustrate the effect of a layered 20-year, layered 15-year, and layered 10-year amortization approach. For illustrative purposes, we also showed how the payoff pattern under these methods compared to the payoff pattern under the previous funding policy, which used a rolling 30-year amortization period consistent with the client’s current method of determining the GASB ARC.

Through graphical illustration of the client’s current funding method and the potential alternatives, it became apparent that the GASB ARC would not meet the client’s newly stated objectives of prudent funding and intergenerational equity in the revised funding policy. Under a rolling 30-year amortization method, negative amortization of the UAAL occurred in each year, so that over time the UAAL was actually projected to grow, rather than eventually being paid off as the client intended.

The graphs in Figures 1 and 2 illustrate the amortization of an initial UAAL over time under various amortization methods, as well as the related UAAL contribution dollars.

The outcome:

Milliman consultants held multiple meetings with the client to discuss current model funding guidance, as well as to discuss the subtleties of the various proposed funding methods. Based on Milliman’s analysis, the client decided on a twofold approach to improve its funding method.

As a first step, the client closed its current amortization period effective immediately through the passage of a resolution. This helped the client take prompt action to fund the plan in what it viewed as a more prudent manner.

The client remained concerned about potential future contribution rate volatility resulting from the closed amortization period, and additionally remained concerned that even a closed 30-year period was longer than they would ultimately like.

To address these ongoing concerns, the client took the further step of writing into legislation a mandatory future deadline to revisit the funding policy, at which time a shorter layered amortization method would automatically trigger if no additional funding policy changes had been implemented. Additionally, the client scheduled a second set of educational and numerical analysis for the year following Milliman’s initial analysis, to keep the topic current and its Board of Retirement well-informed regarding funding options. The client intends to make further changes to the funding policy over the next several years, but formalizing a commitment to do so in the legislation guaranteed that a change would eventually be made if short-term efforts were to fail.

Ultimately, the client achieved an immediate improvement in its funding structure by closing the amortization period, which was due to an improved understanding of its current funding method, and how that compared to more generally accepted methods. The client also gained detailed knowledge about the mitigation of potential future contribution rate volatility for its plan, and a set of tools to address that down the road.

1Guidance published by the Conference of Consulting Actuaries (CCA), the California Actuarial Advisory Panel (CAAP), and the Government Finance Officers’ Association (GFOA). Milliman consultants were involved in several of these national committee efforts.