Most sponsors of public sector defined benefit pension plans have struggled to meet budgets and maintain a healthy funded status for their plans in recent years. One difficulty is that pension contribution requirements increase in ways that cannot be predicted in advance due to market downturns, just as revenues available to fund these contributions decline. Meanwhile, most systems automatically decrease contribution rates when the market begins to recover, and this can cause increased strain on budgets later. Is there another way for a pension plan to meet its funding needs?

The following is a case study for a large municipal defined benefit retirement system (the System) with a “fixed” funding contribution rate. Most defined benefit pension plans have variable contribution rates that change on a regular basis as a product of an annual actuarial valuation. The System takes a different approach, and when done properly, the System’s approach can provide added stability in the contribution rates, assist with budgeting, and result in a better funded status than typically seen for public sector plans.

The funded ratio is a measure of a plan’s funded status and is equal to the ratio of dedicated assets to the measured liabilities.1 It is an important metric used by the System. The latest report from the Center for Retirement Research (CRR) at Boston College estimates that the funded ratio of public pension plans rose from 72% in 2013 to 74% in 2014.2 By contrast, the System had a funded ratio over 95% using smoothed assets and 101% using market assets as of the most recent actuarial valuation.

Most defined benefit systems have variable contribution rates that automatically decrease (increase) after favorable (unfavorable) experience regardless of the municipality’s budget situation or the long-range outlook of the retirement system. Some fixed-rate plans have had difficulty maintaining contribution rates at the levels required to adequately secure the payment of future benefits. This particular System has used its “funding and benefits policy” as well as an emphasis on discipline, prudence, shared responsibility, and a long-range perspective to make the difficult choices required to put itself in a better actuarial position than most public sector pension plans.

There are lessons to be learned from the actions taken by this System and not just for other fixed-rate plans. Every public sector retirement system could give thought to the following steps:

- Seek a cushion above a 100% funding ratio before making permanent increases to benefit levels.

- Do not automatically reduce contribution rates after every year with favorable experience.

- Consider de-risking measures once funding targets are met.

- Take swift action when conditions change dramatically, but do not overreact to every minor change.

- Share responsibility between employers and employees.

A misnomer

A necessary ingredient for proper management of a fixed-rate plan is to acknowledge that the “fixed” rate is not truly fixed. Adjustments must be made periodically. A better name would be a “sticky” rate plan in that the rate does not automatically change every year, but rather remains stable until circumstances warrant a change. When the environment does change, this System’s actions in 2008 demonstrate that a fixed rate plan can react swiftly if well managed.

One fundamental equation applies for any retirement system no matter if it is maintained by an employer, an individual, or a government for all its citizens. It applies to defined contribution plans, defined benefit plans, and hybrids. The contributions (C) combined with investment income (I) into the System must equal the benefit payments (B) and expenses (E) paid out of the System. This results in the equation of C + I = B + E.

In a defined benefit program, “B” is typically defined.3 A retirement system should be designed to meet the obligations of the benefits that have been promised to employees. For large public defined benefit systems, the “E” portion of the equation is typically very small relative to benefits and cannot be easily altered in a meaningful way. The “I” for investment income is variable and unknown in advance, so with B and E difficult to change, the C portion of the equation, contributions, must be adjusted in order for the equation to balance when investment income fluctuates. For this reason, the plan’s contribution rate must not be truly fixed. The contribution rate must be able to adjust if the plan’s funding becomes inadequate.

Response to the 2008 global financial crisis

When the investment markets crashed in 2008, the System’s funded status plummeted as happened with nearly all pension plans. Most public sector defined benefit plans waited until after the next actuarial valuation in 2009 to make adjustments to contribution rates. There is often a lag of 12 to 24 months between the valuation date and the date when contribution rates change, meaning that the contribution rates did not adjust to reflect the market crash until 2010 or 2011.

By contrast, the System responded much more swiftly. Meetings were held in November and December 2008 to discuss various options, months before the stock market indices hit bottom in March 2009. In those meetings, policymakers made a quick but measured response to increase the rates gradually, starting in February 2009. At that time, the combined contribution rates for the employer and employees increased from 14% to 16% of payroll.

Eventually, the total contribution rate increased to 20% of payroll in January 2012 and has remained at that level since that time. The contributions are the shared responsibility of the employer and employees, with the employer paying just over half of the total. This shared responsibility means that both employees and the employer are aware that a fixed contribution rate can change.

Funding and benefits policy

As with most public sector defined benefit systems, the funded ratio for the System is measured on an annual basis. As seen in the 2008 example, assets are monitored more frequently and adjustments can be made when necessary. While the promised benefits are studied and analyzed every year, the contribution rate does not always change.

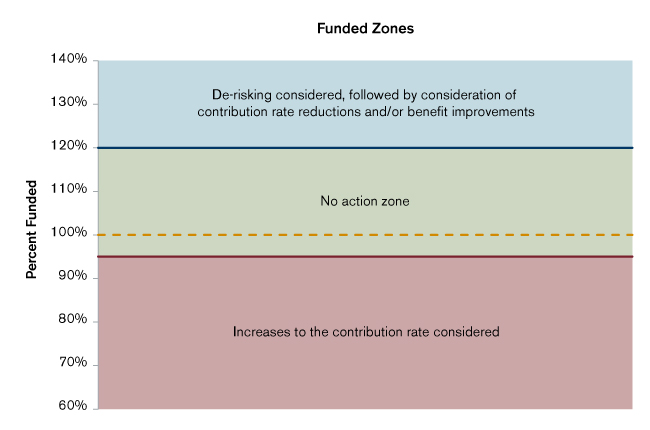

While policymakers have the discretion to recommend a change to contribution levels when deemed necessary, the funding and benefits policy has guidelines and metrics to assist those policymakers with the difficult decisions required. The policy has a relatively wide (but not too wide) zone for maintaining the status quo. When the funded ratio is between 95% and 120% and certain other parameters are met, the policy advises that no action should be taken.

Note that the “no action” zone is not symmetric around 100%. This is by design, which is due to the belief that actions required to increase the funded ratio when it dips below 100% are more urgent than taking actions that could decrease the funded ratio as it exceeds 100%. Reserves over 100% may be needed for future rate stabilization. The funded ratio is a useful measure, but it is based on the assumption that best estimates are met. A cushion above 100% is welcomed when assumptions are not met.

Often in the public sector, there are significant governance issues once there is a “surplus” as measured by a funded ratio above 100%. Permanent benefit improvements can be made based on temporary highs in asset values.

To illustrate just how common benefit improvements can be, consider the findings of a survey conducted by the Wisconsin Legislative Council.4 The report compared significant features of major state and local public employee retirement systems in the United States. According to the survey, 30 of the 85 plans increased their formula multipliers between 2000 and 2002. In addition, 32 of the 85 plans studied increased their formula multipliers between 1996 and 2000.

While the booming equities markets of the late 1990s made these benefit improvements look affordable when they were granted, the markets this century have not kept pace with actuarial assumptions and many funds are seriously depleted as a result. For plans that did not enhance benefits in those years, the plans that varied the contribution rates on an annual basis automatically reduced the contribution rates when asset values increased, typically without providing a cushion for future experience lagging expectations.

Note that in the System’s policy, the term “funding reserve” is used instead of surplus when the funded ratio is above 100%. While this is only terminology and does not directly influence anything, it reflects a mindset that having a funded ratio above 100% does not mean that you have extra money that must be spent; instead, there is a reserve for rate stabilization.

Funded ratios above the no action zone

When the funded ratio is above 120%, the policy states that de-risking will be considered followed by consideration of contribution reductions and/or benefit improvements, provided that the system’s funding status is expected to remain stable after the changes. The funding policy is integrated with considerations for benefit levels and investments. Rather than taking the approach that the benefit levels should be maximized based on what the latest measurements and current market expectations imply are affordable, consideration is given to investment risk and the long-term stability of the system.

De-risking could include the purchase of annuities for part of the future benefit payments or simply increasing the allocation to fixed income in the investment policy, away from more volatile categories such as public and private equities or real estate.

De-risking would not mean offering lump sum buyouts. For private sector defined benefit plans, “de-risking” often does mean offering lump sum buyouts, where the investment and longevity risk are pushed from the retirement system to retirees. The longevity risk should be easier for the system to shoulder than it would be for each individual participant, who typically cannot predict the end of life, while a mortality table can help a system predict the mortality of a large group.

Note that decreasing the risk taken by the plan would decrease the measured funded ratio. This is because the liabilities are measured based on discounting future benefit payments at the expected rate of return. A less risky portfolio will typically have a lower expected rate of return as the investor is no longer being compensated for the risk taken. The lower expectation will mean a lower discount rate, which will mean higher measured liabilities and a lower funded ratio. While the funded ratio is lower, the actual expected benefit payments do not change and those payments should be more secure with a more conservative asset allocation. The de-risking could push the funded ratio back into the no action zone.

Funded ratios below the no action zone

When the funded ratio falls below 95%, increases to the contribution rates are considered. There are additional guidelines to assist with setting a schedule for increased contributions. Those guidelines include considerations of long-term funding projections and consideration of both actuarial and market value funded ratios. There is a goal to have a contribution rate sufficient to return to a 100% funded status in less than 30 years if all assumptions are met. Practical considerations, such as making incremental changes and providing lead time so that both employers and employees can adjust budgets, are also part of the guidelines.

Conclusion

The comparative success of the System was not attained easily and certainly there will continue to be challenges. Adverse experience, particularly regarding investment performance, can significantly weaken funded status. While the current funded ratio does signify better funding than most systems, continued diligence will be required for future success. The funding and benefits policy has served this system well and appears to give it the right foundation to assist with future challenges.

1Here the measured liabilities are known as the actuarial accrued liability (AAL). The AAL is essentially a funding target based on the discounted value of projected benefit payments. The AAL is the portion of that value allocated to service prior to the valuation date.

2Alicia H. Munnell and Jean-Pierre Aubry in “The Funding of State and Local Pensions: 2014 – 2018”, June 2015, p. 2 from the Center for Retirement Research at Boston College.

3While the strength of the laws protecting benefits varies by state and the laws are being challenged in the courts in some locations, it is usually difficult to alter benefits that have been accrued, and, in many cases, it is even difficult to change the benefit formula for future service once a public employee has been hired. This is commonly referred to as “vested rights.”

42002 Comparative Study of Major Public Employee Retirement Systems, dated December 2003, page 25