Recent trends in investment markets are signalling heightened financial risk, posing new challenges for investors. In this brief note, we talk about key market features contributing to this environment. We also talk about a potential strategy for managing financial risk—especially valuable for individuals approaching retirement who seek to convert their hard-earned savings into a reliable, long-term income stream.

Long-term bond markets

A key theme emerging this year has been the notable increase in long-term interest rates across numerous economies worldwide. In both the UK and Europe, 30-year interest rates have recently reached their highest levels in five years—in the case of the UK, the highest level since 1998. Although the US 30-year rate has not risen as sharply, it remains elevated compared to its average over the past five years.

Figure 1: Yields on 30-year government bonds

Source: Bloomberg

This trend has been particularly pronounced for long-term rates, while short-term rates have not experienced the same degree of upward movement. The divergence between short-term and long-term rates is becoming increasingly significant, highlighting shifting market expectations regarding inflation and fiscal policy.

Figure 2: Spread—30-year less 2-year government bond yield

Source: Bloomberg

In the UK, the rise in long-term rates is especially topical due to the increasing pressure on government finances. The cost of servicing debt now exceeds spending on key areas such as defence and education.1 Additionally, the UK market is feeling the effects of pension funds unwinding their gilt-heavy LDI hedges, while insurers are seeking higher-yielding assets to match their buyout liabilities, provided such assets are available.

This is not merely a local phenomenon, but part of a broader global trend. Heightened and more uncertain long-term inflation expectations mean investors are demanding greater compensation for holding government debt. Some economies, such as those in Europe, are experiencing increased spending, particularly in response to the need for stronger defence budgets. Political resistance to public spending cuts, as seen recently in France, adds further complexity. Overall, record levels of debt issuance are fuelling increased concerns about long-term debt sustainability. The following summary of analysis from Insight Investment classifies the fiscal outlook for all G7 economies, except Germany, as either risky or unsustainable.

Figure 3: Debt burden of economies by country

| Economy | Government debt/GDP |

Fiscal deficits | Interest costs as % of GDP |

Overall outlook |

|---|---|---|---|---|

| Canada | 111% | Good | 3.2% | Risky |

| France | 116% | Bad | 1.8% | Unsustainable |

| Germany | 65% | Worsening | 0.7% | Stable |

| Italy | 134% | Improving | 3.8% | Risky |

| Japan | 236% | Worsening | 1.5% | Risky |

| UK | 101% | Improving | 3.3% | Risky |

| US | 123% | Bad | 3.6% | Unsustainable |

Source: Colesmith, G., & Down, S. (September 2025). Fiscal fault lines: A global review of sovereign fiscal health. Insight Investment. Retrieved 9 October 2025 from https://www.insightinvestment.com/globalassets/documents/recent-thinking/q3-2025-global-macro-research/uk-eu-gmr-fiscal-sustainability.pdf.

The prevailing fear is that major economies could inch closer to a “debt doom loop,” where rising debt and servicing costs reinforce each other, undermining fiscal stability.

Figure 4: Debt doom loop

Equity markets

Despite the heightened risks facing bond markets, unresolved inflationary pressures and ongoing geopolitical uncertainties, global equity markets have recently been performing strongly. Since the volatility seen around April’s Liberation Day, many of the major equity indices have rebounded, with some reaching record highs.

Most national equity benchmarks across developed markets have shown positive returns for the year. Some sectors, such as information technology (driven by the hype around artificial intelligence) are showing stronger performance than others. However, growth is also seen in more traditional sectors such as financials and industrials.

Option markets also appear relatively calm; for instance, the VIX, a key benchmark for market volatility, remains below its historical average. This suggests that investors are not currently pricing in these longer-term risk factors. The VIX however is a measure focusing on 30-day options, so it may just indicate that the market does not view this as an immediate risk.

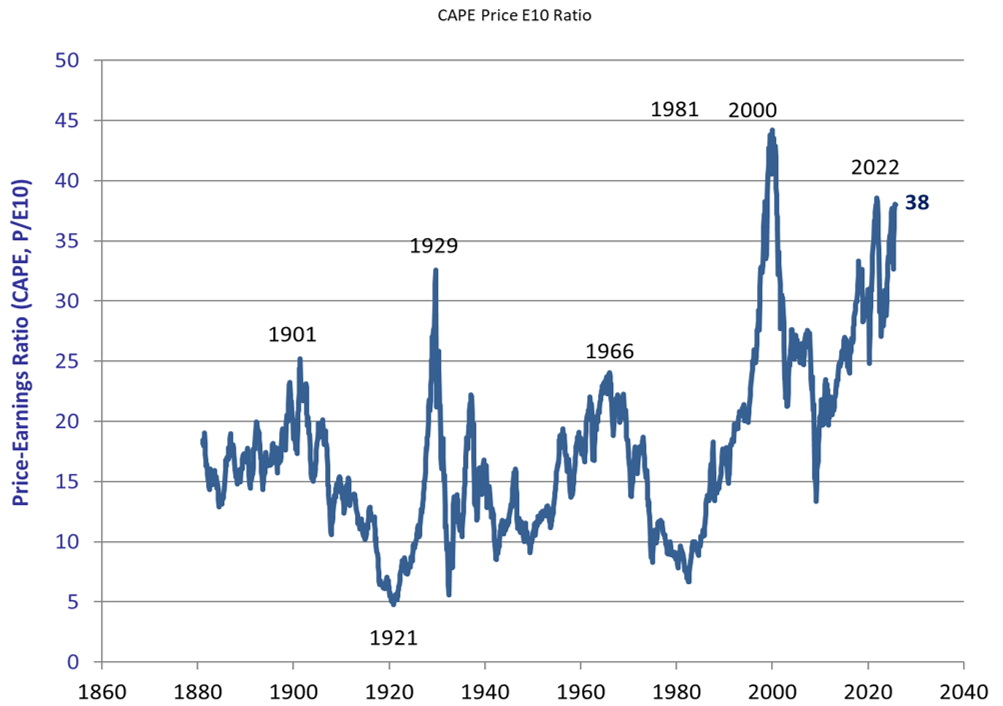

Gold, a traditional safe-haven asset, has increased in price massively this year, by over 40%. This sharp increase may reflect rising concerns about risk in the financial system, particularly as market perception of the US Treasury and US dollar as safe-haven assets has weakened. There are certainly signs that equities may be overvalued. This is shown by both the conventional price-earnings (P/E) ratio, as well as the Shiller P/E ratio (or CAPE). The latter ratio smooths earnings over 10 years and adjusts for inflation, providing a longer-term perspective.

As of the end of August 2025, the Shiller P/E on the S&P 500 index stood at approximately 38x. This level is not only far above its historical mean of around 17x but also places current valuations among the most elevated on record. In fact, the index has only been higher on two prior occasions: at the peak of the dot-com bubble in 1999–2000 and briefly at year-end 2021 during the post-pandemic surge. Such elevated readings have historically preceded periods of muted equity returns, underscoring the extent to which today’s market is priced for perfection.

Figure 5: The Shiller price earnings ratio (CAPE) on the S&P 500 since 1871

The calculation includes a cyclical adjustment.

Source: Chart from Shiller Data, based on updated numbers included in Irrational Exuberance, published by Princeton University Press. Accessed October 8, 2025, from https://shillerdata.com/.

Financial risk implications: The case for dynamic management

For retirees, portfolios typically rely on equities and bonds as their core investment engines. As discussed, both asset classes remain exposed to some significant financial risk that could potentially lead to market falls. Furthermore, the negative correlation experienced between equities and bonds since the late 1990s has broken down in recent years, increasing the risk that both could decline simultaneously—as witnessed in 2022.

When previous acute market crisis events occurred, such as in 2008 and 2020, global governments and central banks were able to respond effectively to bring the crisis under control and help confidence return to the markets. Response measures included bailing out banks, cutting interest rates and issuing stimulus packages.

In the current environment, and given the risk of a debt doom loop, global governments are more restricted, limiting their ability to respond in a similar manner to any repeat acute crisis event. With inflation far from being under control, central banks are also less able to cut interest rates. If an acute crisis event were to occur, especially one that included high inflation risk, market confidence may not be restored for a long time.

This could be especially painful for retirees. As discussed in our recent paper on sequencing risk,2 market crash events that occur for a prolonged period of time are more damaging to the sustainability of retirement income. If the next crisis were to depress markets for a similar period to the Global Financial Crisis (2008–2009), that could be highly damaging.

The shifting landscape highlights the need for alternative risk management strategies. One approach is to purchase options, which can provide downside protection, but these typically come with an embedded premium. Even when absolute volatility is low, this embedded premium cost of options can remain relatively high.

Another strategy is that of dynamic hedging or dynamic risk management. This approach involves synthetically creating option-like exposure and providing a cushion against market downturns. The main advantage of dynamic hedging is its lower cost, as it avoids paying the embedded option premium. However, the level of protection is variable and not guaranteed, offering “soft protection” rather than “hard protection.” Despite this consideration, dynamic hedging can offer meaningful protection in severe market downturns, giving retirees greater confidence to remain invested.

Figure 6 shows the progression of a retirement fund invested in a 60/40 portfolio and taking income at a 5% initial rate increasing with inflation. It compares two starting points in history—year-end-2001 and year-end-2011—and a 60/40 portfolio with and without dynamic risk management applies. The effect of dynamic risk management is to narrow the range of outcomes and reduce the uncertainty of timing risk of income commencement relative to the market cycle.

Figure 6: Progression of a 60/40 fund with income taken, comparing different historic scenarios and with/without risk management

Results based on simulated or hypothetical performance results have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown. Milliman does not manage the underlying fund.

As with any risk management approach, there is a trade-off. There is an insurance cost of protection in the form of a reduction in expected portfolio return compared to an unprotected strategy. However, the value of maintaining confidence to stay invested should also be considered. If risk protection enables investors to maintain a higher allocation to equities rather than reducing exposure out of caution, this is a source of value that can offset the expected cost.

Dynamic risk management represents an additional tool that can complement more traditional approaches, such as asset class diversification, bucketing strategies or dynamic withdrawal strategies. The result is the ability to strike a better balance for retirees between protection from significant market falls and participation in future growth.

Disclaimer

The information, products, or services described or referenced herein are intended to be for informational purposes only. This material is not intended to be a recommendation, offer, solicitation or advertisement to buy or sell any securities, securities-related product or service, or investment strategy, nor is it intended to be to be relied upon as a forecast, research or investment advice.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient. Investment involves risks. Any discussion of risks contained herein with respect to any product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved. Investing in foreign securities is subject to greater risks including currency fluctuation, economic conditions, and different governmental and accounting standards.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors. Information herein has been obtained from sources we believe to be reliable, but neither Milliman Financial Risk Management LLC (Milliman FRM) nor its parents, subsidiaries or affiliates warrant its completeness or accuracy. No responsibility can be accepted for errors of facts obtained from third parties.

The materials in this document represent the opinion of the authors at the time of authorship; they may change and are not representative of the views of Milliman FRM or its parents, subsidiaries or affiliates. Milliman FRM does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary, and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman FRM. Milliman Financial Risk Management LLC is an SEC-registered investment advisor and subsidiary of Milliman, Inc.

1 See analysis shown in House of Lords - National debt: it’s time for tough decisions - Economic Affairs Committee and https://ifs.org.uk/microsite/education-spending.

2 Dissanayake, N., & Ward, R. (20 June 2025). Retirement income: The impact of market risk. Milliman. Retrieved 9 October 2025 from https://www.milliman.com/en/insight/retirement-income-impact-market-risk.