1. Use an auto-enrollment design with a default of no less than 6%.

2. If you provide a match, stretch the match to at least 7% or 8% of pay.

3. Consider adding a nonelective (i.e., profit-sharing) contribution.

4. Reenroll all non-savers every six years at the default rate.

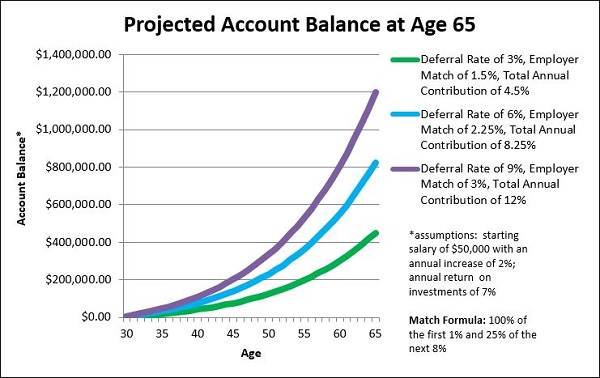

Some experts suggest that automatic plan features are the best way to change behavior. This is most likely true, but a New York University (NYU) study suggests that while auto-enrollment gets people into the plan, it is not ensuring that they build secure retirements. All too often employers select the default rate of 3%, which, according to researchers, reduces long-term retirement savings for those who would have enrolled at a higher rate. As consultants, we see this example frequently a young employee enters the plan automatically and three years later is still at 3%, even though the plan is matching deferral rates up to 6%. Out of sight and out of mind can be dangerous for young employees. The NYU study states that 80% of retirement plans include an employer match contribution, and of those plans, almost half of employees are not maximizing the match. That means that at least half of workers do get it; at the right deferral rate, there is free money on the table. With this in mind, consider an example to illustrate the savings impact of a new match contribution formula: currently, the match is 50% of the first 6% (or maximum of 3% of pay). Why not match 100% of the first 1%, then 25% of the next 8%? In this scenario, we could argue that half of the employee population would defer 9% of pay to get the 3% match. This would produce a total annual contribution of 12% of pay per year, without the employer matching anymore compensation than it did in the current formula.

Figure 1: Match Formulas

To emphasize the impact of different deferral rates on an employee's account balance at retirement, using the proposed new match formula, see the chart below:

Figure 2: Potential Savings

A recent Employee Benefits Research Institute Retirement Confidence Survey asked workers what action they would take if they were automatically enrolled into their retirement plans, deferring 6%. Nearly three-quarters, 74%, responded that they would stay at that rate or increase their contribution rates. This survey addressing employee behavior offers strong incentive for a 6% auto-enrollment rate. In my opinion, plan sponsors should incorporate this type of employee behavioral analysis into the plan design process. A current client has maintained participation rates near 90%, with a 6% auto-enrollment rate. And of those deferring, 84% defer at a rate greater than or equal to 6%.

While matching contributions are an important feature, the researchers argue a more beneficial tool for a plan is a general (i.e., nonelective) contribution. And if the employer can afford to, and the plan is designed for the population correctly, the nonelective contribution can provide a more substantial retirement benefit. There are, of course, trade-offs, and with nonelective contributions comes stricter annual testing.

Something else to think about reenrolling all current employees when the plan adds the auto-enrollment design. I have witnessed firsthand the success of such an endeavor with another Milliman client who did this 18 months ago. The plan went from 63% participation to 97% and has maintained that level.

As an administrator of defined contribution plans, I know automatic arrangements can be difficult to administer, but the recent relaxation by the Internal Revenue Service (IRS) of correction rules (Revenue Procedure 2015-28), and the evidence provided by the surveys mentioned above, simplify the decision. If employers enroll new employees in plans automatically, they are clearly likely to stay, and the automatic arrangement often becomes the obvious choice. But the rate needs to be high enough to be worthwhile. Plan sponsors must evaluate the goals of their plans. Is the objective to simply have higher participation, satisfy tax incentive rules, and ensure that workers save something toward retirement? Or is it to truly build a serious retirement benefit for employees? In that likely case, additional studies of the employee population and their saving behavior must be incorporated into plan designs.