In developing the investment menu for a pension plan, a sponsor has a number of considerations: target return, asset allocation, cash flows, manager selection, and cost. This article explores some aspects of each, with a main focus on developing a menu of investments that has a mix of index and actively managed options.

The target return for a pension plan is generally the annual required return for the plan to maintain a level contribution pattern. Along with utilizing the target return, an advisor often focuses on the cash flows of the plan, running them through an asset liability model. For the limited scope of this article, we do not delve into matching the duration of liabilities to the duration of assets, an approach known as liability-driven investing (LDI). This article focuses on the asset side of managing the investments in a pension portfolio.

Developing the base: “A rising tide lifts all ships”

Starting with the primary asset categories—U.S. equity (small, mid, and large), bonds (short-, intermediate-, and long-term), and international investments—a sponsor can develop a fairly well diversified portfolio. Running these basic asset categories through an optimizer tool will yield an efficient portfolio on a risk/return basis. Now you have developed an allocation that should, in theory, maximize returns and minimize risk.

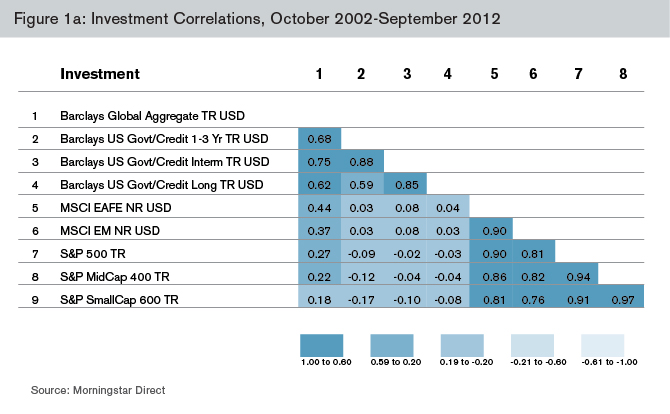

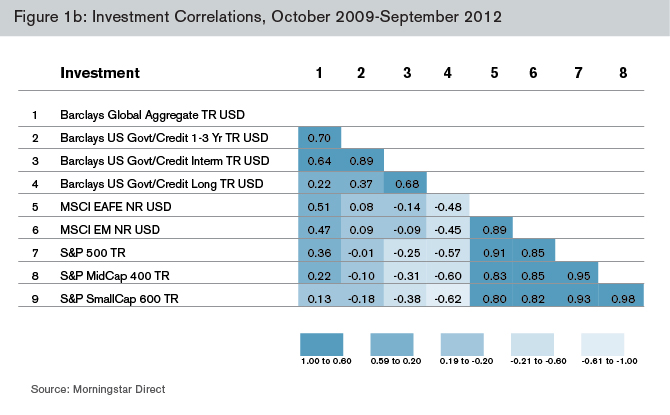

However, an important aspect to consider is the correlation of the asset categories. The correlation charts Figure 1a and 1b show that, over the last decade, many of the investments have become more highly correlated. On the bond side, there is often a fairly high degree of correlation among the maturity terms, except for longer durations (10+ years) and on the equity side there is a high degree of correlation among various domestic market caps, foreign and emerging markets. In rising markets, correlation of investments in a portfolio may not be much of a concern as all the asset classes are moving up. However, in a bear market, as well as a volatile one, a high degree of correlation could keep a plan sponsor up at night.

At a very high level, one method of managing correlation is diversification across fixed-income and equity investments. As shown below, these investments often have a low or negative correlation with other asset categories and therefore offer some opportunities to manage the correlation of underlying investments.

Finding downside defensive managers

So how does a sponsor work with beta, alpha, and investment management to offset the beta or market risk exposure? Simple. Look for managers to offset some of the downside risk. Well, not so simple: the search should consist of both a qualitative and a quantitative review. Screen on the quantitative side for managers who have good downside measures (when the market goes down, these managers tend to fall at a slower rate) and confirm they have a policy of moderating exposure to risk as their model indicates a pullback in the market. Some methods of protecting capital that an investment manager can employ include holding more cash in the portfolio or holding stocks that move contrary to market movements.

Some of the statistical measures to review in looking at managers who do well in declining markets (who may not have a specific policy for downside protection) include: beta/tracking error, downside capture ratio, downside or semi-standard deviation, and various other measures of downside risk. Beta and tracking error are not specifically measures of downside risk, but they give a sense of whether the manager has a tendency to track or follow the market. Looking at the downside measures will show the manager’s tendency of following the market when it is in a declining trend, thereby lowering average or expected returns.

Another aspect to look at is whether the active manager can generate a return in excess of the level of market risk associated with the investment, known as alpha. The focus here is on whether the active manager can consistently generate a return in excess of the market, or beta, with a reasonable level of risk.

This will often lend itself to pairing an index and an active manager in each equity category. The index functions as the beta; as the market rises, upside is captured (and as the market declines, so will the index). The active manager with a low level of downside capture will often offset market losses, thus managing downside investment risks.

In addition, applying some type of hedging strategy to the equity side of the investment portfolio could moderate downside losses. Attempting to cut off the downside tail-risk could possibly allow for more equity upside exposure while limiting downside risk and overall portfolio volatility.

Cost considerations

Overall cost should be a consideration too. As of late, much of the focus of expenses has been on defined contribution (DC) plans. Has anyone looked at pension plan management and administration expenses? Because expected average returns are much lower now than in previous times, investment management and administration expenses have more impact on the overall return of the portfolio. With an approach that combines index and actively managed assets, it's possible to moderate the level of investment management expense by starting with a base of indexes with low investment management expenses, such as institutional mutual funds or exchange-traded funds (ETFs). Adding managers as needed to reduce some of the downside capture, generate alpha, and reduce correlation often results in paying more for these strategies. If applying a hedge to the portfolio, consider where to apply it (to the full portfolio, or to the equity side only) and at what levels. Once all the components are in place, the total cost as a percentage of the portfolio value can be determined.

Summary

In developing a pension portfolio, it is important to focus on the overall goals of the plan, which should be defined in the investment policy; target return, volatility management, overall asset allocation and the management of investment expenses. In starting with basic market indexes (there are thousands to select from) diversification across an array of stock and bond investment categories can be achieved, by strategically adding in active managers, a sponsor can further fine tune the allocation and potentially moderate risk and maximize return.